TL;DR:

- UK businesses must register for VAT when their taxable turnover exceeds £90,000 within a rolling 12-month period or if they reasonably expect to do so within the next 30 days. Proper preparation, including having necessary documents and choosing the appropriate VAT scheme, ensures a smooth registration process and ongoing compliance. Failure to register on time can result in severe penalties, including up to 100% of lost revenue, and complicates subsequent VAT obligations.

Getting VAT registration wrong costs UK businesses real money. Whether you’ve just crossed the £90,000 taxable turnover threshold or you’re planning ahead, the VAT registration process UK businesses must follow has specific rules, tight deadlines, and digital requirements that catch many founders off guard. This guide covers everything you need: when to register, what you need to apply, how to complete the HMRC online process step by step, and how to stay compliant once your VAT number arrives. If you’ve been searching for practical VAT registration help UK, this is where to start.

| Point | Details |

|---|---|

| Know both registration triggers | The £90,000 rolling 12-month test and the 30-day future expectation test are separate obligations requiring immediate action. |

| Gather documents before you start | Having your UTR, company number, bank details, and turnover figures ready cuts registration time to under 30 minutes. |

| Choose the right VAT scheme early | Flat Rate, Cash Accounting, and Standard schemes carry different cash flow impacts. Choosing wrong costs money. |

| Set up MTD-compatible software first | Making Tax Digital requires digital records and linked software before your first VAT return is due. |

| Late registration carries serious penalties | HMRC can charge up to 100% of potential lost revenue for failing to register on time. |

The official term for this process is VAT registration, and in the UK it is governed by the Value Added Tax Act 1994. Most people searching for UK VAT advice are actually trying to answer one question: do I need to register, and when?

There are two independent triggers, and missing either one is where businesses get into trouble.

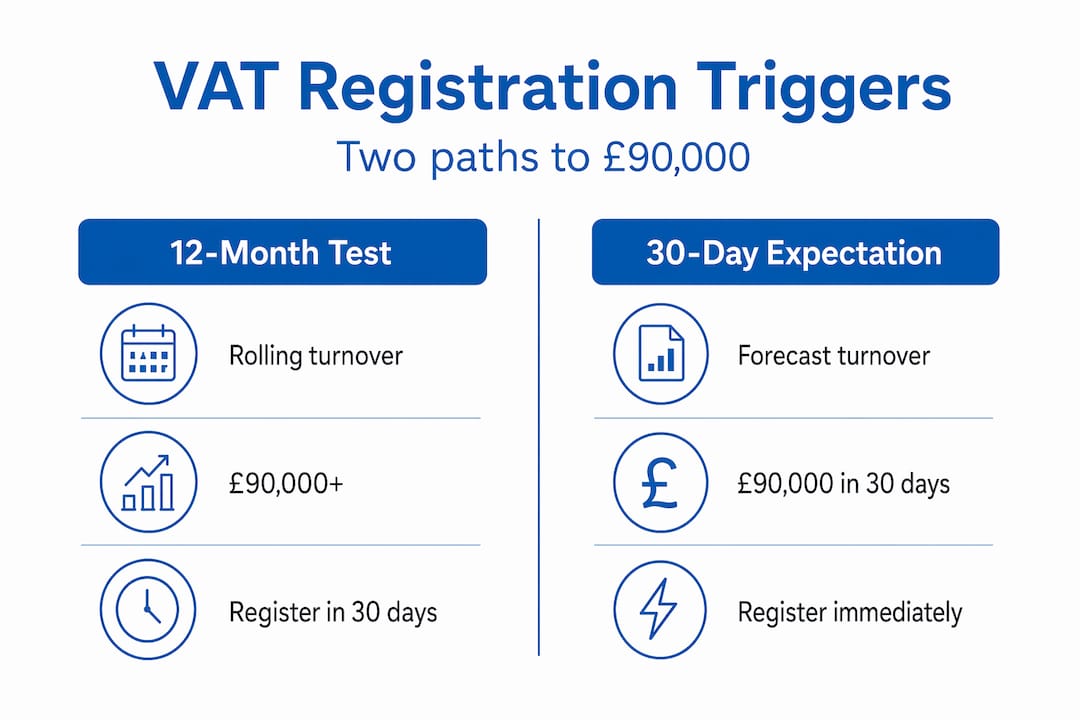

The rolling 12-month test requires you to add up your taxable turnover for any 12-month period ending on the last day of any month. The moment that figure exceeds £90,000, you must register. This is not a tax year figure. It rolls month by month.

The 30-day expectation test is the one that surprises people most. If you have reasonable grounds to believe your taxable turnover will exceed £90,000 within the next 30 days alone, you must register immediately. Winning a single large contract can trigger this even if your previous turnover was modest. Your effective registration date links back to the day that expectation arose, not the day you actually applied.

A critical distinction here: taxable turnover is not the same as total revenue. It excludes exempt supplies (such as certain financial services or insurance) and out-of-scope supplies. Many businesses receive HMRC letters recommending registration based on figures that may include exempt income or cover periods longer than 12 months. Before acting on a letter, verify your actual taxable turnover using HMRC’s definitions.

| Trigger | What counts | Registration deadline |

|---|---|---|

| Rolling 12-month test | Taxable supplies only, any 12-month period | 30 days after the month end in which threshold exceeded |

| 30-day future expectation | Expected taxable turnover in next 30 days alone | Immediately, with effective date at start of 30-day period |

| Voluntary registration | Below threshold but want to reclaim input VAT | Any time, with HMRC approval |

Pro Tip: If you sell a mix of taxable and exempt supplies, calculate your taxable turnover separately before deciding whether you need to register. Many service-based businesses overestimate their obligation.

The HMRC online registration process typically takes 20 to 30 minutes, but only if you have everything ready. Missing even one piece of information can stall the application mid-way, which causes avoidable delays.

Here is what you need to gather before you start:

Beyond documents, you also need to make a scheme decision before you submit. The four main VAT accounting schemes are:

| Scheme | Best suited to | Key benefit |

|---|---|---|

| Standard rate | Most businesses | Straightforward, claim all input VAT |

| Flat Rate Scheme | Small businesses under £150k turnover | Simplified calculation, potential savings |

| Cash Accounting | Businesses with slow-paying customers | Pay VAT only when customer pays you |

| Annual Accounting | Businesses wanting predictability | One return per year, monthly payments |

Choosing the wrong scheme at the outset is harder to undo than people expect. The Flat Rate Scheme, for example, works well for service businesses with low costs but can cost more than the Standard Scheme if your input VAT is high.

Pro Tip: Set up your MTD-compatible accounting software before you register. Digital record-keeping requirements under Making Tax Digital mean you need linked software from day one. Installing it after you receive your VAT number leaves you scrambling before your first return.

For a broader view of how VAT fits into your overall compliance picture, the UK VAT guide from Priceandaccountants covers the full regulatory framework in detail.

The entire process takes place through HMRC’s online VAT registration service, accessed via GOV.UK. Here is how to complete it:

After submission, you can expect confirmation within 5 to 10 working days. Your VAT registration certificate, containing your VAT number and effective registration date, arrives via your Government Gateway account.

The effective registration date is the date from which you are obligated to charge VAT. You must not charge VAT to customers before this date. You can, however, reclaim input VAT on goods and services purchased before registration, subject to time limits: four years for goods still on hand, and six months for services.

Pro Tip: If your effective registration date is backdated because of the 30-day expectation rule, you will owe VAT on invoices issued from that date even if you did not charge it. Factor this into your cash flow immediately. If necessary, issue revised invoices to customers.

For consultants and professionals who need to understand how VAT registration integrates with their broader tax obligations, the tax filing guide for UK consultants is worth reading alongside this.

Registration is step one. The compliance obligations that follow are where many businesses stumble.

The most frequent mistakes Priceandaccountants sees after clients receive their VAT numbers include the following:

On the penalty side, the consequences of late registration are severe. HMRC can charge up to 100% of the VAT that should have been collected as a penalty for non-registration. That sits on top of the VAT itself, which you owe from the date registration was required.

If you sell to EU customers and use the Import One Stop Shop (IOSS) scheme, missing three consecutive monthly returns can lead to exclusion from the scheme for two years. For any business with EU exposure, this is a rule worth knowing before it becomes a problem.

Pro Tip: Set calendar reminders for every VAT return deadline the moment you receive your registration certificate. Your first deadline will arrive faster than expected, especially if your effective date is backdated.

The businesses that manage VAT without stress are not the ones with the most time. They are the ones with the right processes in place from the beginning.

Effective VAT threshold monitoring involves two distinct habits: a monthly review of rolling 12-month turnover, and an immediate review whenever you win a large contract. These are separate checks that serve different purposes. Monthly checks catch the gradual creep towards the threshold. Contract checks catch the sudden leap over it.

Once registered, your routine should include:

The digital bookkeeping habits required for MTD are not as burdensome as they sound if you set them up correctly from the start. Xero, QuickBooks, and FreeAgent all meet HMRC’s MTD requirements and integrate with most banking platforms.

Pro Tip: Do not wait until your first VAT return to test your MTD software. Run a practice submission or reconcile a test period before your actual deadline. This reveals any data link gaps early, when there is still time to fix them without penalty.

I’ve helped dozens of UK founders through the VAT registration process, and the single biggest mistake I see is treating registration as a one-off admin task rather than the start of an ongoing compliance obligation. People rush the application, pick a scheme without thinking it through, and then spend the next 12 months wishing they had chosen differently.

What I’ve found is that the 30-day expectation rule is the most dangerous blindspot of all. Founders who win a transformative contract often celebrate before considering whether that single win just triggered an immediate VAT registration obligation. I’ve seen businesses that had to backdate their registration by several months because of one contract, resulting in significant VAT liabilities on invoices they hadn’t collected it on.

The other thing I always tell clients: get comfortable with your MTD software before you need it. HMRC’s digital record requirements are not negotiable, and I’ve seen otherwise well-run businesses face penalties simply because their data links were broken. Sort this early, and your first VAT return becomes a formality rather than a crisis.

Proactive VAT management also has an upside that people underestimate. Once you understand your VAT position monthly, you get a much clearer view of your actual trading cash flow. For growth-stage businesses, that visibility is genuinely useful beyond compliance alone.

Do not let the perceived complexity of VAT registration push you into delay. A missed registration deadline costs far more than taking a few hours to sort it properly.

— Rahamut

VAT registration and ongoing compliance do not need to be something you work through alone. At Priceandaccountants, we support UK business owners and tech founders with everything from initial VAT compliance management to MTD-compatible bookkeeping and VAT return filing. We help you choose the right VAT scheme for your business model, handle your HMRC registration, and set up professional bookkeeping that keeps your records clean and your returns accurate. Whether you’re approaching the £90,000 threshold for the first time or cleaning up a late registration situation, our team has seen it before and knows how to fix it. Get in touch with Priceandaccountants today for tailored VAT guidance built around your business, not a generic checklist.

You must register when your taxable turnover exceeds £90,000 over any rolling 12-month period, or when you have reasonable grounds to believe it will exceed that figure within the next 30 days alone.

The online application takes 20 to 30 minutes if you have all your information ready. HMRC typically confirms registration within 5 to 10 working days and sends your VAT certificate via Government Gateway.

Late registration means you owe VAT on all taxable sales from the date you should have registered, plus interest. HMRC can also charge a penalty of up to 100% of lost VAT revenue, depending on how long registration was delayed.

Yes. All VAT-registered businesses in the UK must keep digital records and submit returns using MTD-compatible software. Manual entry or spreadsheet-only approaches do not meet HMRC’s requirements.

Yes. Voluntary registration is available to any UK business below the £90,000 threshold and allows you to reclaim input VAT on business purchases, which can be valuable during a period of high startup expenditure.