TL;DR:

- Proper management of VAT is crucial for tech and fintech SMEs to avoid cashflow issues, penalties, and audit risks. Understanding VAT classification, registration thresholds, and compliance requirements ensures VAT becomes a strategic part of financial operations rather than a compliance burden. Leveraging digital tools and expert support can optimize VAT processes, recover costs, and future-proof your business as it scales.

VAT is often dismissed as just another compliance box to tick, but that framing costs tech and fintech SMEs real money. Handled poorly, it creates cashflow gaps, audit exposure, and late-registration penalties. Handled well, it becomes a predictable, even strategic part of how you run your finances. UK VAT is a tax on most goods and services administered by HMRC, and understanding it properly is one of the highest-return financial habits you can build. This guide walks you through everything: what VAT actually is, when you must register, how to charge and reclaim it, and what Making Tax Digital means for your business in 2026.

| Point | Details |

|---|---|

| VAT impacts every SME | Understanding VAT helps you manage both compliance and cashflow in your daily operations. |

| Know registration thresholds | Check your turnover regularly and register for VAT promptly to avoid penalties. |

| Digital records now required | Almost all VAT returns must be submitted digitally under Making Tax Digital. |

| Monitor input vs output VAT | Track VAT on sales and purchases to ensure accurate returns and reclaim opportunities. |

| Get strategic support | Professional advice can help you avoid costly errors and optimise your VAT processes. |

VAT stands for value added tax. It is charged at each stage of a supply chain, from manufacturer to wholesaler to end customer, with each business collecting VAT on sales and reclaiming VAT paid on purchases. The net result is that only the final consumer bears the full cost.

For tech and fintech businesses, this mechanic matters enormously. Your SaaS subscription, digital API product, or payment-processing service almost certainly carries VAT. Getting the rate wrong, or misclassifying a supply as exempt when it is taxable, can trigger HMRC corrections and penalties. The UK VAT landscape is more nuanced than many founders realise, particularly when digital products and cross-border services are involved.

VAT rates break down into three main categories, plus exempt supplies. Here is how they apply to typical tech SME products and services:

| VAT rate | Percentage | Common tech/fintech examples |

|---|---|---|

| Standard rate | 20% | SaaS subscriptions, software licences, digital consultancy, app downloads |

| Reduced rate | 5% | Some energy-saving products (rarely applies to tech SMEs directly) |

| Zero rate | 0% | Some printed publications (physical books); most tech services do not qualify |

| Exempt | N/A | Certain financial services, insurance; some fintech products may qualify |

The distinction between zero-rated and exempt is critical and often misunderstood. A zero-rated supply still allows you to reclaim input VAT on related costs. An exempt supply does not. If your fintech product blends financial intermediation with software, the VAT treatment of each component matters individually.

“VAT is charged at the standard rate of 20% on most goods and services, with other rates (reduced/zero) and exempt supplies depending on what is supplied.” Tax Confident guidance

HMRC publishes detailed small business VAT advice covering specific product types, and checking it regularly is worth the effort. The rules for digital services, in particular, have evolved significantly since 2015.

Key points to absorb here:

Getting these classifications right from the start saves significant corrective work later.

The legal position is clear: if you sell taxable goods or services in the UK above the VAT registration threshold, you must register. The obligation is not about whether registration is convenient. It is about your rolling 12-month taxable turnover and whether it has crossed the threshold set by HMRC.

The rolling check is the part that trips up fast-growing tech startups. You are not looking at your financial year. You are looking at the last 12 calendar months at any point in time. A strong six months of SaaS growth can push you over the threshold before you realise.

| Threshold type | Amount (2025/26) | Registration deadline |

|---|---|---|

| Mandatory registration | £90,000 taxable turnover | Within 30 days of the month end in which threshold was exceeded |

| Voluntary registration | Below threshold | Any time, if beneficial |

| Distance selling / EU digital services | Varies by destination country | At point of supply to consumers |

Your legal VAT registration obligations begin the moment you exceed the threshold, not when you notice it. Missing the deadline exposes you to backdated VAT liability and potentially a late-registration penalty.

Here is what to do as you approach the threshold:

For businesses selling B2B, place-of-supply rules mean your UK VAT registration may not be the only obligation. Selling digital services to business customers in the EU? The reverse charge mechanism usually applies, shifting the VAT accounting to your customer. Selling to EU consumers? You may need to register under the EU’s One Stop Shop (OSS) scheme. These are not hypothetical edge cases for fintech and SaaS businesses with European user bases. They are live obligations.

Check key VAT deadlines alongside your registration planning, because missing dates anywhere in the compliance calendar creates compounding problems.

Pro Tip: Always check the latest HMRC guidance before filing or making registration decisions. VAT thresholds and digital service rules have changed multiple times in recent years and can change again.

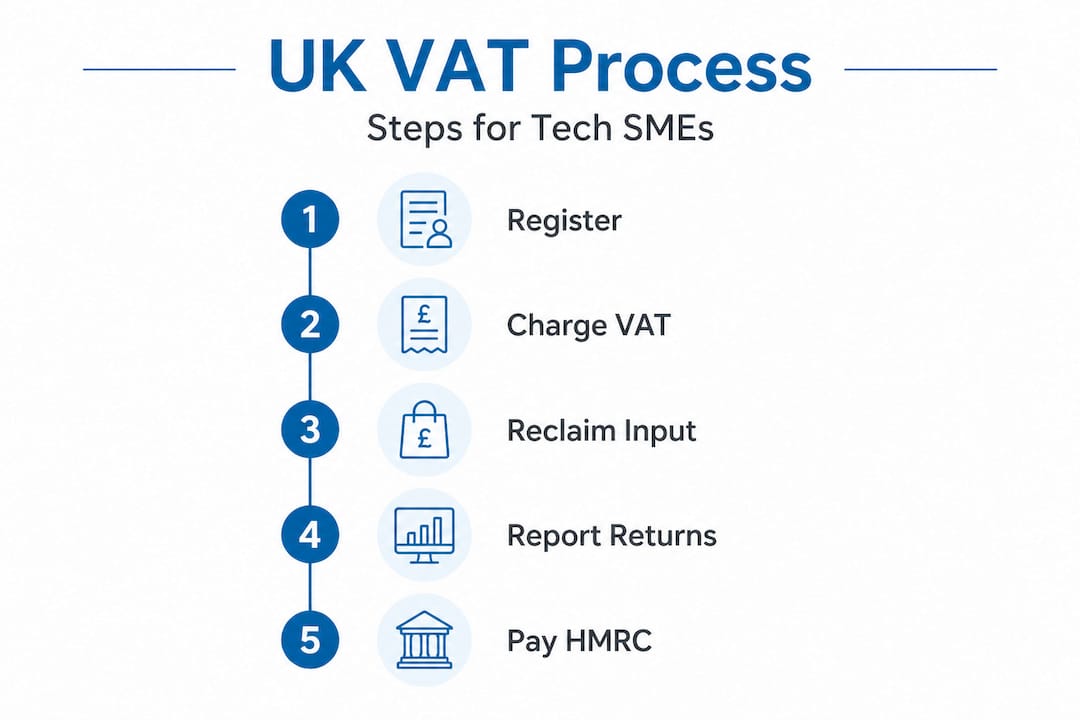

Once you are VAT-registered, you enter the VAT lifecycle. Every transaction touches it. Output VAT is what you charge your customers on taxable sales. Input VAT is what you pay on your own business costs. The difference between the two is what you pay to, or reclaim from, HMRC each quarter.

The VAT compliance management process, done correctly, looks like this:

Charging output VAT. Every VAT-registered business must issue a valid VAT invoice for taxable supplies made to other VAT-registered businesses. A valid invoice must include your VAT number, invoice date, a description of the supply, the VAT rate applied, and the VAT amount. Missing any of these details can mean your customer cannot reclaim the VAT you charged them, which damages your commercial relationships.

Reclaiming input VAT. You can reclaim VAT paid on goods and services used for your taxable business activities. This includes software subscriptions, hardware, office costs, and professional services. You cannot reclaim VAT on entertainment expenses or on costs attributable exclusively to exempt supplies. Keep every supplier invoice. HMRC expects to see supporting documentation on inspection.

Submitting VAT returns. Most businesses submit quarterly. The return shows total output VAT, total input VAT, and the net amount due to or from HMRC. You must submit within one calendar month and seven days of the end of your VAT period.

A compliance workflow for startups built around these three steps prevents the most common errors. Speaking of which, here are the mistakes we see most often:

Pro Tip: Maintain digital records and clear supplier documentation for every VAT claim you make. If HMRC opens an enquiry, the burden of proof sits with you. A missing invoice means a disallowed claim.

“A common VAT compliance benchmark for SMEs is whether you are VAT-registered and, if so, you must manage output VAT (charged to customers) versus input VAT (VAT paid on business costs), including via VAT returns.” Tax Confident guidance

The cashflow point here is worth emphasising. VAT you collect from customers is not your money. It belongs to HMRC. Setting it aside in a separate account, or at minimum tracking it separately in your accounting software, prevents the painful scenario of having spent the VAT before the return is due. Review the official HMRC VAT rules for full details on return periods, payment deadlines, and how to handle errors on previous returns.

Making Tax Digital (MTD) for VAT is not optional. Since April 2022, virtually all VAT-registered businesses must keep digital VAT records and submit returns through MTD-compatible software. There are narrow exemptions, for example for businesses with religious objections to using computers or those who are digitally excluded, but these are genuinely narrow.

“Most VAT-registered businesses must submit VAT returns digitally under Making Tax Digital (MTD) for VAT, subject to limited exceptions and exemptions.” HMRC MTD evaluation

For tech SMEs, MTD should feel natural. Your business runs on software. But many early-stage companies still submit VAT through a spreadsheet and the legacy HMRC portal, which ceased to be MTD-compliant in 2022. If that is you, you are already non-compliant.

Here is what you need to do:

The Making Tax Digital guide for tech startups covers the practical setup in detail. If you are also navigating self-assessment or corporation tax alongside VAT, the tax filing steps for consultants and freelancers may also apply to your situation.

Pro Tip: Choose your MTD-compatible software before you hit the registration threshold. Setting it up under pressure after registration causes data gaps and reconciliation headaches that take months to fix.

Here is something most generic VAT guides will not tell you: the businesses that struggle most with VAT are not those who ignore it entirely. They are the ones who copy a generic approach and assume it fits. It does not, not for tech and fintech businesses.

The core problem is misclassification at scale. A SaaS business with 10,000 B2C users and a handful of B2B enterprise clients cannot treat all of those transactions identically for VAT purposes. The place-of-supply rules, the VAT rates, and the invoicing requirements differ by customer type, by geography, and sometimes by the specific feature set being sold. When you are billing at volume, one misclassified product line compounds across thousands of transactions.

A practical methodology for VAT compliance that actually works for tech SMEs involves three disciplines: first, maintaining a clear record of which supplies are taxable and at what rate; second, knowing whether each customer is B2B or B2C for place-of-supply purposes; and third, having digitised accounting that supports MTD and survives an HMRC audit.

Future-proofing your VAT processes also means thinking about scale. The VAT workflow that works at £100,000 in revenue often breaks at £1m. Automation helps, but automating the wrong classification just scales the error. Review your VAT supply types every six months, not just when something goes wrong.

Our insider checklist for minimising risk:

Pro Tip: Do not just automate your VAT filings. Use your technology to improve VAT classification at point of entry and to retain evidence automatically. Fixing classification errors after the fact is far more expensive than getting them right the first time.

Managing VAT well is not simply about avoiding penalties. For tech and fintech SMEs, the right approach can recover meaningful sums through input VAT reclaims, protect cashflow, and demonstrate financial maturity to investors. Professional support frequently pays for itself in the first quarter alone.

At Price & Accountants, our VAT compliance support is built specifically for UK tech and fintech businesses, not retrofitted from a generic small business template. We understand the nuances of digital service VAT, partial exemption, and MTD compliance in environments that move fast. Our strategic tax advice service goes further, combining VAT planning with broader tax efficiency so your growth decisions are always financially sound. We also help innovative businesses access R&D tax credits alongside their VAT strategy, maximising every relief available. Get in touch to build a VAT action plan tailored to your business.

You must register for VAT when your taxable turnover exceeds the threshold set by HMRC for the relevant tax year. VAT Notice 700/1 explains the registration rules and how the rolling 12-month check works.

Yes. Most digital products including SaaS subscriptions, app downloads, and software licences are taxable at the standard 20% rate, unless they fall within a specific exemption.

Almost certainly yes. Most VAT-registered businesses must use MTD-compatible software to file VAT returns, and the exemptions are very narrow.

Yes, provided you are VAT-registered and the costs relate to taxable business activities. Input VAT on eligible costs can generally be reclaimed, subject to proper record-keeping and applicable rules.

Late registration results in backdated VAT liability from the date you should have registered, plus potential penalties and interest. VAT Notice 700/1 sets out the statutory deadlines and what HMRC expects when you miss them.