Navigating UK tax filing presents unique challenges for consultants and tech entrepreneurs. With over 60% of self-employed individuals reporting confusion about compliance requirements, getting your tax procedure right matters more than ever. Timely and accurate filing ensures you avoid penalties whilst optimising tax efficiency. This guide breaks down the complete tax filing procedure for 2026 step by step, covering registration deadlines, profit calculations, Making Tax Digital requirements, and practical strategies to streamline your compliance journey.

| Point | Details |

|---|---|

| Registration deadline | Register for Self Assessment by 5 October following your first tax year to avoid automatic penalties |

| Profit calculation | Calculate taxable profits using accruals or cash basis accounting, deducting allowable business expenses from turnover |

| MTD compliance | Making Tax Digital mandates digital records and quarterly updates from April 2026 for gross income above £50,000 |

| Common pitfalls | Late filing triggers £100 minimum penalties, whilst IR35 misclassification creates unexpected tax liabilities |

| Record retention | Maintain detailed business records for five years minimum to satisfy HMRC audit requirements |

Your tax filing obligations depend entirely on your business structure and income level. Consultants operating as sole traders must register for Self Assessment by 5 October following the end of their first tax year if earnings exceed £1,000. The UK tax year runs from 6 April to 5 April, creating a filing cycle that differs from the calendar year many international founders expect.

Registration triggers a cascade of compliance requirements. You must file your online return by 31 January following the tax year end, with payment due on the same date. Missing this deadline incurs an immediate £100 penalty, escalating rapidly if you delay further. For consultants earning above certain thresholds, payments on account become mandatory, requiring you to pay half your estimated tax bill by 31 January and the remainder by 31 July.

The distinction between sole trader and limited company structures creates dramatically different obligations. Sole traders complete Self Assessment returns reporting business profits directly. Limited company directors file corporation tax returns for the company whilst completing personal Self Assessment for salary and dividends. Each structure offers distinct tax planning opportunities, particularly for consultants scaling beyond £50,000 annual revenue.

Pro Tip: Register immediately when you start consulting, even if your first year income falls below £1,000. Early registration establishes your tax record cleanly and avoids rushed compliance later.

Key registration and filing milestones include:

Penalties escalate quickly for late compliance. Beyond the initial £100 fine, HMRC adds daily penalties of £10 after three months, additional percentage-based charges after six months, and potential investigation costs if patterns of late filing emerge. The financial impact compounds when you factor in interest charges on late tax payments, currently running above 7% annually.

Taxable profits are calculated using accruals or cash basis accounting, deducting allowable business expenses from turnover. Cash basis suits most small consultancies, recognising income when received and expenses when paid. Accruals accounting matches income and costs to the period they relate to, regardless of payment timing. You can switch between methods, but consistency matters for accurate year-on-year comparisons.

Allowable expenses reduce your tax bill significantly when claimed correctly. HMRC permits deductions for costs incurred wholly and exclusively for business purposes. Office equipment, professional subscriptions, travel between client sites, and software licences all qualify. Personal costs, commuting from home to a permanent workplace, and entertaining clients remain non-deductible despite their business connection.

Record keeping requirements extend five years from the 31 January submission deadline. You need invoices, receipts, bank statements, and mileage logs supporting every expense claim. Digital records satisfy HMRC provided they capture the same detail as paper equivalents. Cloud accounting platforms like Xero automate much of this burden, categorising transactions and generating reports that feed directly into tax calculations.

Simplified expenses offer an alternative for small businesses, replacing actual costs with flat rate allowances. Vehicle expenses become a per-mile rate rather than tracking fuel, insurance, and depreciation separately. Working from home allows a monthly flat rate based on hours worked instead of apportioning utility bills and mortgage interest. The trade-off favours simplicity over potentially higher actual expense claims.

| Expense Category | Allowable Examples | Simplified Rate Option |

|---|---|---|

| Vehicle costs | Fuel, insurance, repairs, depreciation | 45p per mile (first 10,000 miles), 25p thereafter |

| Home office | Proportion of rent, utilities, council tax | £10-£26 monthly based on hours |

| Professional fees | Accountancy, legal advice, industry subscriptions | Actual costs only |

| Equipment | Laptops, software, office furniture | Annual investment allowance up to £1 million |

| Travel | Client site visits, accommodation, subsistence | Actual costs with receipts |

Pro Tip: Run dual calculations comparing simplified expenses against actual costs before choosing your method. Many consultants discover simplified vehicle rates save tax in early years, whilst actual home office costs prove more beneficial as businesses mature.

Capital allowances provide additional relief for equipment purchases. The annual investment allowance lets you deduct the full cost of qualifying assets up to £1 million in the year of purchase. Computers, office furniture, and business vehicles all qualify, creating immediate tax savings rather than spreading relief over the asset’s useful life. This becomes particularly valuable when investing in technology infrastructure to support client delivery.

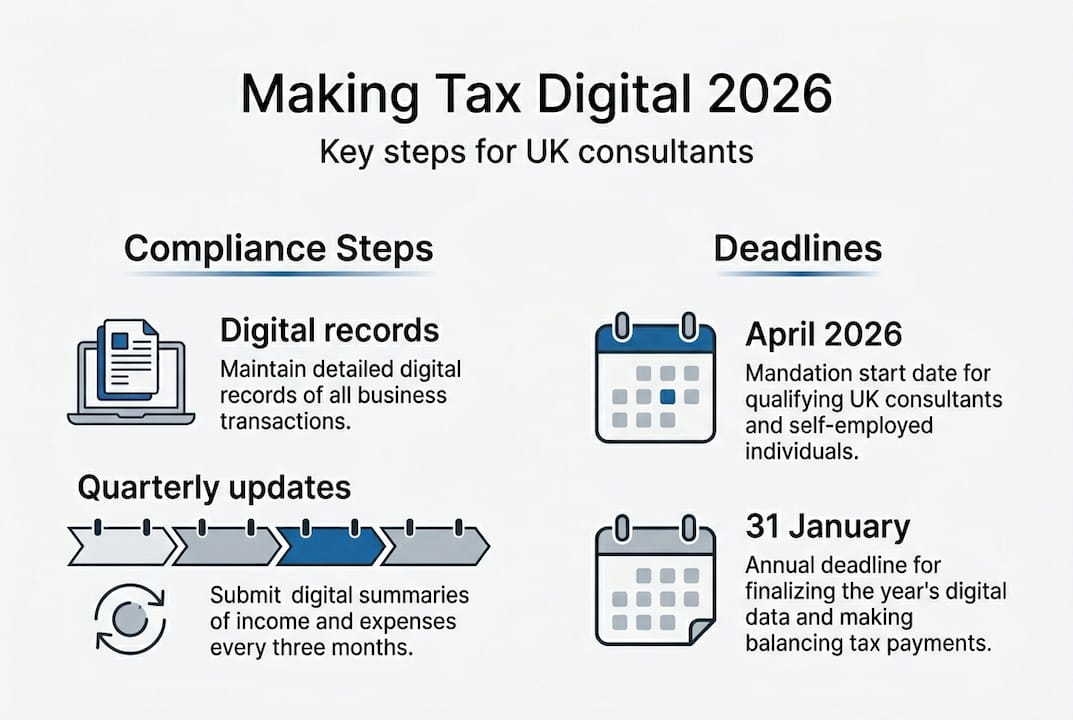

From 6 April 2026, Making Tax Digital mandates digital records and quarterly updates for self-employed consultants with gross income exceeding £50,000 from trade or property. This threshold drops to £30,000 from April 2027, bringing most established consultancies into scope. MTD fundamentally changes how you interact with HMRC, replacing annual Self Assessment with quarterly digital submissions throughout the tax year.

Digital record keeping becomes mandatory under MTD. You must maintain income and expenditure records in compatible software that links directly to HMRC systems. Spreadsheets no longer satisfy compliance unless they connect via MTD-approved bridging software. Cloud accounting platforms dominate the approved software list, offering real-time visibility of your tax position alongside automated quarterly submissions.

Quarterly update deadlines create a new compliance rhythm. You submit four updates covering:

Each update summarises income and expenses for the quarter without calculating tax due. The final declaration, submitted by 31 January following the tax year, replaces the traditional Self Assessment return. This declaration confirms your annual position, claims reliefs, and triggers any balancing payment.

“MTD transforms tax compliance from an annual scramble into a manageable quarterly routine, reducing year-end surprises and improving cash flow planning for growing consultancies.”

Voluntary adoption before April 2026 offers significant advantages. Testing MTD software now identifies workflow issues whilst stakes remain low. You gain familiarity with quarterly rhythms and discover how real-time reporting improves business decisions. Early adopters report smoother transitions and fewer technical problems when mandatory compliance arrives.

Pro Tip: Schedule a startup tax compliance guide review three months before your MTD start date. This buffer allows time to migrate historical data, train on new software, and resolve integration issues without deadline pressure.

Penalties under MTD mirror traditional Self Assessment initially, but HMRC plans points-based systems penalising patterns of late submission rather than isolated delays. Understanding these evolving rules becomes critical as digital compliance matures beyond its 2026 launch.

Missing registration or filing deadlines triggers escalating penalties that damage profitability. The initial £100 fine for late Self Assessment seems modest, but daily penalties of £10 begin after three months. Six months late adds penalties of 5% of tax due or £300, whichever proves greater. Twelve months late doubles these percentage penalties whilst HMRC gains powers to estimate your tax bill, typically erring conservatively high.

IR35 legislation creates particular complexity for consultants working through limited companies. The off-payroll working rules determine whether your consultancy constitutes genuine self-employment or disguised employment. HMRC’s Check Employment Status for Tax tool provides initial guidance, though its limitations mean professional review remains essential for borderline cases. Misclassification triggers unexpected tax liabilities, National Insurance contributions, and potential penalties extending back four years.

Multiple income streams complicate tax calculations when consultants combine employment, self-employment, and investment income. Each requires different reporting sections within Self Assessment. Losses from one business can offset profits from another, but only when claimed correctly. Trading losses can carry forward indefinitely against future profits or carry back one year against previous profits, creating valuable tax planning opportunities often overlooked in DIY returns.

Pro Tip: Review your business structure and client contracts before April 2026. Converting from sole trader to limited company or vice versa takes months to execute properly, so early planning prevents rushed decisions driven by compliance deadlines.

| Structure | Tax Efficiency | Administrative Burden | IR35 Risk |

|---|---|---|---|

| Sole trader | Lower at <£50k profit | Minimal compliance | Not applicable |

| Limited company | Higher at >£50k profit | Corporation tax, accounts, confirmation statement | Significant for single-client consultants |

| Partnership | Flexible profit allocation | Partner tax returns plus partnership return | Moderate depending on client relationships |

Overseas contractors present unique considerations. Working entirely outside the UK for non-UK clients may avoid IR35 altogether, whilst maintaining UK tax residence still triggers Self Assessment obligations. Double taxation treaties prevent paying tax twice on the same income, but claiming relief requires meticulous documentation and often professional support.

Common expense claim errors include mixing personal and business costs, claiming capital items as revenue expenses, and overlooking legitimate deductions. Professional subscriptions, industry conference attendance, and continuing professional development all qualify when directly relevant to your consultancy. Home office claims fail most often through inadequate evidence of exclusive business use or incorrect calculations of allowable proportions.

The reasonable care defence protects against penalties when genuine mistakes occur despite diligent effort. Maintaining contemporaneous records, seeking professional advice on uncertain matters, and promptly correcting discovered errors all demonstrate reasonable care. HMRC distinguishes sharply between careless mistakes and deliberate errors, with penalty rates varying from zero to 100% of tax lost depending on behaviour and disclosure timing.

Specialist tax consultant benefits become apparent when navigating these complexities. Professional support costs less than most consultants expect whilst delivering returns through optimised structures, maximised reliefs, and avoided penalties. The value compounds for high-growth consultancies where tax planning shapes business decisions around hiring, investment, and international expansion.

Navigating MTD compliance and quarterly updates demands expertise that diverts focus from client delivery. Price & Accountants specialises in supporting UK consultants and tech entrepreneurs through every compliance requirement whilst identifying tax planning opportunities that generic accountants miss.

Our strategic advisory and tax planning services optimise your business structure for current operations and future growth. We analyse whether sole trader, limited company, or partnership structures serve your specific situation best, factoring in IR35 implications, profit levels, and expansion plans. Our accurate bookkeeping solutions maintain MTD-compliant digital records automatically, generating quarterly updates without manual intervention. This frees you to focus on consulting whilst we ensure compliance deadlines never slip.

Beyond basic compliance, we provide specialist guidance on corporation tax planning for consultants operating through limited companies. Our team identifies reliefs, allowances, and structural opportunities that reduce tax liabilities legally whilst maintaining full HMRC compliance. Whether you’re scaling from solo consultant to multi-person consultancy or expanding internationally, our 40 years of experience supporting high-growth businesses ensures you make informed financial decisions at every stage.

HMRC issues an automatic £100 penalty immediately, regardless of whether you owe tax. Additional daily penalties of £10 begin after three months late, capped at £900. Six months overdue triggers further penalties of 5% of tax due or £300 minimum, doubling again at twelve months.

Yes, provided your home serves as your business base rather than simply convenient workspace. You can claim a proportion of mortgage interest, rent, utilities, and council tax based on business use. Simplified flat rates of £10 to £26 monthly offer an easier alternative for smaller claims.

IR35 determines whether you pay tax as self-employed or deemed employee. If caught by IR35, you must deduct income tax and National Insurance as though employed, significantly reducing take-home pay. Medium and large clients now assess IR35 status themselves, but small business clients leave responsibility with you.

Not immediately, but consider adopting voluntarily. The threshold drops to £30,000 in April 2027, and early adoption smooths the transition. Cloud accounting software offers benefits beyond MTD compliance, including real-time financial visibility and automated expense tracking that improve business decisions.

Yes, trading losses can offset other income in the same tax year or carry back to the previous year for immediate tax refunds. Alternatively, carry losses forward indefinitely against future trading profits. The optimal strategy depends on your income profile and tax rates across different years.

Maintain all invoices, receipts, bank statements, and mileage logs for five years from the 31 January submission deadline. Digital records satisfy requirements provided they capture transaction dates, amounts, suppliers, and business purposes. Cloud accounting platforms automatically store this detail whilst generating audit trails HMRC accepts.