TL;DR:

- UK employers must enroll all eligible workers in a qualifying pension scheme from their first day at work. Setting up and maintaining this process is essential to avoid fines and ensure proper retirement savings.

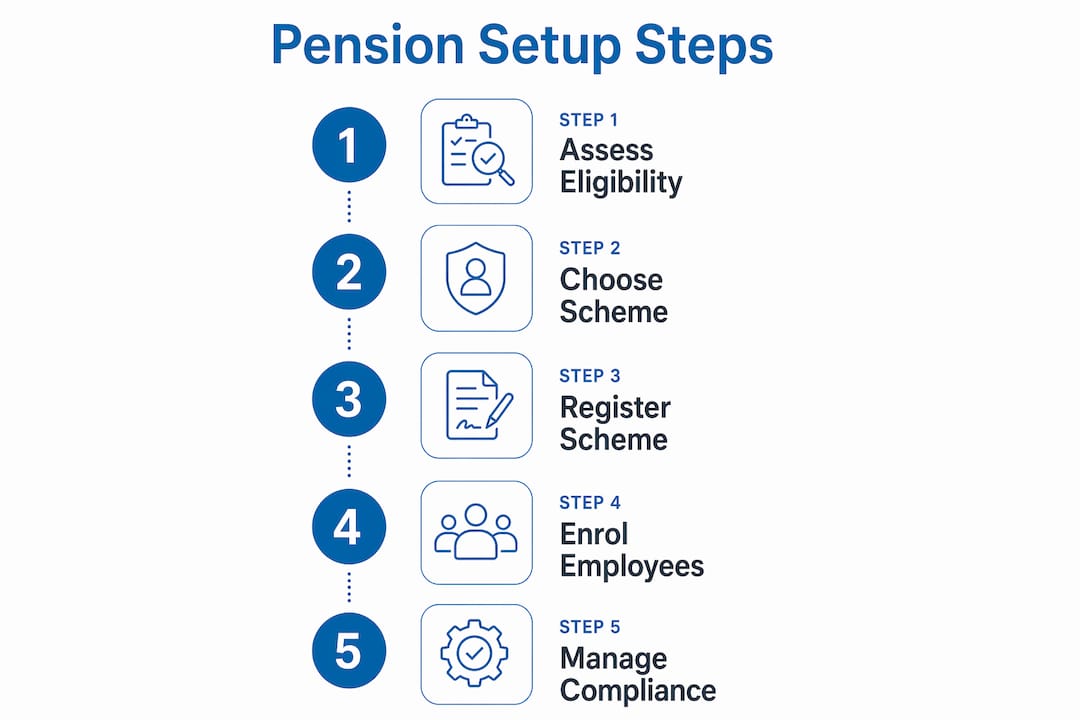

Automatic enrolment is the legal duty requiring every UK employer to enrol eligible workers into a qualifying workplace pension scheme from the first day they begin work. The Pensions Act 2008 established this obligation, and The Pensions Regulator enforces it across all business sizes. For the step by step pension setup for UK SMEs, the process covers five core stages: preparing your payroll, selecting a compliant scheme, assessing employees, communicating enrolment, and managing ongoing compliance. Getting each stage right from the start protects you from fines and keeps your team’s retirement savings on track.

Your duties start on the day your first employee begins work. That date is called your duties start date, and everything flows from it. Setting up your pension scheme before that date is the only way to avoid backdating contributions and the penalties that come with it. Assessing employees from day one is a legal requirement, not a best practice.

Before you register a scheme, you need three things in place:

Eligibility under the auto-enrolment rules applies to workers aged 22 to State Pension age who earn over £10,000 per year and work in the UK. Workers outside those parameters are not eligible for automatic enrolment, though they may have the right to opt in.

Pro Tip: Set a calendar reminder for your duties start date the moment you hire your first employee. Missing it by even one pay period can trigger a backdating obligation that is time-consuming and costly to correct.

Good recordkeeping is non-negotiable. The Pensions Regulator can request evidence of your assessment process, your communications to employees, and your contribution records at any time. Keep digital copies of all correspondence and payroll outputs.

A qualifying pension scheme must meet the standards set out in the Pensions Act 2008. The scheme must accept all eligible workers, meet minimum contribution thresholds, and be registered with HMRC. Not every pension product on the market meets these criteria, so you cannot simply pick any provider.

For most SMEs, the practical options fall into two broad categories:

| Feature | Government-backed (e.g. NEST) | Commercial master trust |

|---|---|---|

| Setup fee | None | Varies by provider |

| Must accept all employers | Yes | Not always |

| Payroll integration | Standard | Varies |

| Investment flexibility | Limited | Higher |

| Best suited for | SMEs needing simplicity | Businesses with specific investment needs |

Once you select a scheme, register it with The Pensions Regulator through your online account. You will need your PAYE reference number and your duties start date. Registration is separate from your Declaration of Compliance, which comes later.

Pro Tip: NEST is the default choice for most SMEs starting out. Its zero setup cost and universal acceptance remove two of the biggest barriers to getting a scheme in place quickly.

Check that your chosen scheme’s contribution structure aligns with the legal minimums before you finalise registration. The minimum total contribution is 8%, split as at least 3% from the employer and 5% from the employee.

Employee assessment is the process of categorising every worker by age and earnings to determine what pension rights they hold. You must run this assessment on the first day of employment and repeat it every pay period, because a worker’s status can change as their earnings fluctuate.

The three categories are:

Once you identify eligible jobholders, enrolment must happen promptly. The legal process runs as follows:

Pro Tip: Do not rely on employees to tell you when their earnings cross the £10,000 threshold. Your payroll software should flag eligibility changes automatically each pay period. If it does not, that is a gap in your compliance process.

Workers who opt out must be re-enrolled at the three-year cycle regardless of their wishes. They can opt out again, but you cannot simply leave them out permanently.

Contribution management is where many SMEs slip up. The minimum total contribution is 8% of qualifying earnings, with at least 3% coming from the employer. Qualifying earnings currently sit between £6,240 and £50,270 per year. Contributions above those thresholds are at the employer’s discretion.

The ongoing compliance cycle works as follows:

| Compliance task | Deadline |

|---|---|

| Employee assessment | First day of employment and every pay period |

| Enrolment notification to worker | Within 6 weeks of eligibility |

| Opt-out window closes | 1 month from enrolment or letter date |

| Declaration of Compliance | Within 5 months of duties start date |

| Re-enrolment cycle | Every 3 years from duties start date |

The Pensions Regulator issues fixed penalty notices starting at £400 for missed declarations. Persistent non-compliance escalates to daily fines. The declaration of compliance is a recurring duty, not a one-off task. It repeats at every three-year re-enrolment cycle for the lifetime of your business.

For a broader view of your payroll obligations alongside pension duties, the payroll compliance checklist from Priceandaccountants covers both areas in detail.

Setting up a compliant workplace pension for a UK SME requires acting from day one, selecting a qualifying scheme, and maintaining a structured three-year compliance cycle.

| Point | Details |

|---|---|

| Act from day one | Your pension duties begin the moment your first employee starts work. |

| Choose a qualifying scheme | NEST is free, universal, and integrates with payroll software, making it the practical default for most SMEs. |

| Assess every pay period | Employee eligibility can change as earnings fluctuate, so assessment must run with every payroll cycle. |

| File the Declaration of Compliance | Submit to The Pensions Regulator within 5 months of your duties start date, even with no eligible workers. |

| Re-enrol every three years | Opted-out workers must be re-enrolled at the three-year cycle, followed by a new Declaration of Compliance. |

The most common mistake I see is treating pension setup as a task to complete after the first payroll has already run. By that point, you are already behind. The legal duty starts on day one, and backdating contributions is a genuinely painful process that eats into time and cash you cannot afford to lose.

The second mistake is the “set and forget” attitude. Proactive management of pension duties is what separates compliant businesses from those receiving penalty notices. A worker’s earnings can cross the £10,000 threshold mid-year. A new hire can join at 22 and immediately trigger enrolment. These events happen quietly, and if your payroll software is not flagging them, you will miss them.

My honest advice: integrate your pension platform with your payroll software before your first employee starts. Manual contribution calculations are error-prone and unnecessary when automation handles it reliably. Diary your Declaration of Compliance deadline and your three-year re-enrolment date the moment you know your duties start date. Treat those dates with the same seriousness as a tax filing deadline, because the penalties are just as real.

Pension compliance is not complex once the system is in place. The difficulty is getting the system in place before the clock starts. That is where most small business owners lose ground.

— Rahamut

Pension setup sits inside a wider set of payroll and compliance obligations that grow quickly as your team grows. Priceandaccountants handles auto-enrolment duties, contribution management, and Declaration of Compliance filings as part of its payroll and pension services for UK SMEs.

With over 40 years of expertise and a track record supporting businesses from pre-seed to Series A, Priceandaccountants acts as your finance partner rather than just a filing service. If you want pension compliance handled correctly from day one, the accounting services team is ready to take it off your plate. Reach out today to discuss your specific situation.

Automatic enrolment is the legal duty to enrol eligible workers into a qualifying workplace pension scheme without waiting for them to ask. It applies from the first day an employee begins work.

Workers aged 22 to State Pension age who earn over £10,000 per year and work in the UK must be automatically enrolled. Workers outside those parameters have opt-in rights but are not enrolled automatically.

The minimum total contribution is 8% of qualifying earnings, with at least 3% paid by the employer and 5% by the employee. Qualifying earnings are currently banded between £6,240 and £50,270 per year.

The Declaration of Compliance must be submitted to The Pensions Regulator within 5 calendar months of your duties start date. You must file even if you have no eligible workers at that time.

Employers must re-enrol eligible workers who have opted out every three years from the original duties start date. A new Declaration of Compliance must be submitted within five months of each re-enrolment date.