TL;DR:

- Business valuation estimates a company’s worth using income, market comparisons, and asset values. It results in a range reflecting investor perceptions of risk and future earnings. Founders should normalize financials and consider multiple methods to improve credibility and negotiating power.

Business valuation is the structured process of estimating a company’s monetary worth using earnings, market comparisons, and asset values to reach a defensible figure. For UK founders, understanding what is business valuation means understanding how investors, acquirers, and lenders will judge your company before they commit capital. The three core approaches are the Income approach, the Market approach, and the Asset-based approach, each reflecting a different view of where value sits. Getting this right matters whether you are raising a Series A, preparing for a merger, or simply benchmarking your progress. A valuation is not a fixed number. It is a strategic baseline reflecting a buyer’s view of risk and future cash flow.

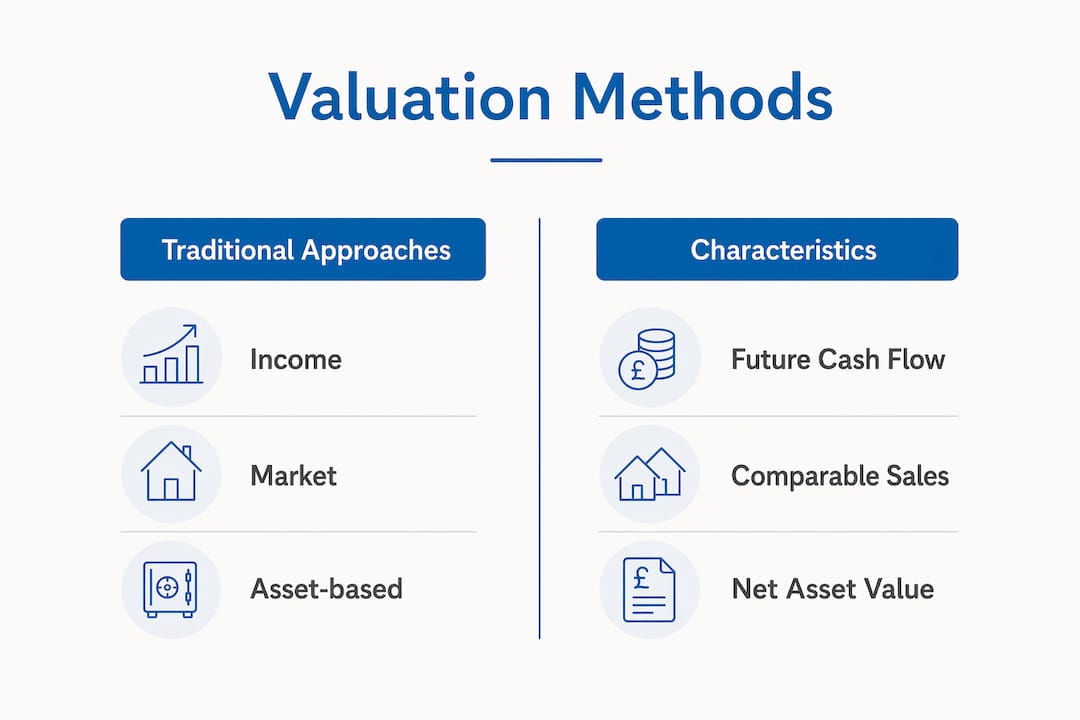

Three primary approaches form the foundation of every business appraisal process: Income, Market, and Asset-based. Most practitioners use at least two of these to triangulate a credible range of value rather than relying on a single figure.

The Income approach values a business by the future cash it is expected to generate. The two main techniques are Discounted Cash Flow (DCF) and capitalisation of earnings.

DCF projects cash flows over a 5–10 year period and discounts them back to today using the Weighted Average Cost of Capital (WACC). Capitalisation of earnings takes a single normalised earnings figure and divides it by a capitalisation rate. DCF suits high-growth businesses with variable cash flows. Capitalisation of earnings suits stable, mature businesses with predictable profits.

The Market approach values a business by comparing it to similar companies or transactions. Comparable company multiples apply revenue or EBITDA multiples drawn from publicly traded peers. Precedent transactions use multiples paid in recent private acquisitions. Guideline transactions carry a 33% method-weight on average in multi-method valuations. This approach works best when good comparable data exists, which is easier for established sectors than for early-stage tech.

The Asset-based approach calculates value from the net worth of a company’s assets after liabilities. Adjusted net assets restate balance sheet items to fair market value. Liquidation value estimates what assets would fetch in a forced sale. This approach suits asset-heavy businesses, holding companies, or distressed situations. It rarely captures the full value of a profitable trading business because it ignores future earnings.

| Approach | Key method | Best suited for |

|---|---|---|

| Income | DCF, capitalisation of earnings | Growth businesses, stable profitable firms |

| Market | Comparable multiples, precedent transactions | Businesses with good sector comparables |

| Asset-based | Adjusted net assets, liquidation value | Asset-heavy, holding, or distressed companies |

Pro Tip: Never present a valuation based on a single method to an investor or acquirer. Using two or three approaches and showing where they converge gives your figure far more credibility in negotiations.

Choosing the wrong earnings base is one of the most common errors in the business appraisal process. The two main options are Seller’s Discretionary Earnings (SDE) and EBITDA, and the choice depends on your business size and management structure.

SDE adds back the owner’s salary, personal benefits, and non-recurring expenses to net profit. It reflects the total financial benefit a single working owner extracts from the business. SDE is typically used for owner-operated businesses with revenue under £4 million, where the owner’s involvement directly shapes cash flow.

EBITDA strips out interest, tax, depreciation, and amortisation to show operating profit before financing and accounting decisions. It is the standard earnings base for professionally managed businesses above the £4 million revenue threshold. Buyers use EBITDA because it allows comparison across companies with different capital structures and tax positions.

The practical difference matters enormously:

Pro Tip: Before any valuation exercise, have your accountant prepare a clean normalised earnings schedule. Every legitimate add-back, from personal vehicle costs to one-off legal fees, can multiply your enterprise value by 3 to 10 times depending on your sector.

Enterprise value is the headline figure most founders focus on. It represents the total value of the business, including debt, before any adjustments. The amount a seller actually receives is almost always lower, sometimes significantly so.

The bridge from enterprise value to equity value works like this. Net debt is deducted first: any bank loans, overdrafts, or finance leases reduce the proceeds. Working capital adjustments follow. If the business delivers less working capital than the agreed target at completion, the buyer deducts the shortfall. Transaction costs, including legal fees, advisory fees, and stamp duty, come off the seller’s proceeds too.

Beyond these standard adjustments, deal structure creates further complexity:

Trade debtors and accounts receivable form part of the working capital calculation, so their quality and ageing profile directly affect how much cash you walk away with. A business with £2 million enterprise value and £400,000 in net debt, £100,000 in working capital shortfall, and £150,000 in transaction costs nets the seller approximately £1.35 million at close. Understanding that gap before you enter a sale process is not optional.

Pro Tip: Ask your adviser to model a full proceeds bridge before you agree heads of terms. Founders who negotiate on enterprise value alone often receive a surprise at completion.

Every business valuation is anchored to a specific date. The figure reflects only the information that was known, or reasonably knowable, on that date. Post-valuation events cannot be used to adjust the value retroactively, even if a major contract was signed the day after.

This matters for founders who believe a recent win should lift their valuation. If the contract was not signed before the valuation date, it does not count. Valuers use 5–10 year cash flow projections discounted by WACC to estimate present value, and those projections must be grounded in evidence available at the valuation date.

Key implications for UK founders:

The concept of fair value in accounting requires that assets and liabilities reflect conditions at a specific measurement date. Business valuation follows the same discipline. Assumptions must be defensible, not aspirational.

Business valuation is always a range of values, not a single number, and the method, earnings base, and valuation date each shape where that range sits.

| Point | Details |

|---|---|

| Three core approaches | Income, Market, and Asset-based methods should be combined to triangulate a credible value range. |

| Earnings base matters | Use SDE for owner-operated businesses under £4 million revenue; use EBITDA for larger, professionally managed firms. |

| Enterprise value is not proceeds | Net debt, working capital adjustments, earnouts, and transaction costs reduce what a seller actually receives at close. |

| Valuation date is fixed | Only information known at the valuation date counts; post-date contracts cannot lift the figure retroactively. |

| Normalise your financials | Every legitimate add-back can multiply enterprise value by 3 to 10 times, making financial normalisation one of the highest-value steps before any sale. |

Founders come to me expecting a single number. They want to know their business is worth £3 million, full stop. That expectation sets them up for frustration, because a credible valuation is always a range reflecting low, base, and high scenarios. Single point estimates undermine credibility in buyer negotiations because any experienced acquirer will immediately challenge the assumptions behind a precise figure.

The second mistake is presenting raw management accounts without normalisation. Financial normalisation means adjusting your statements to remove owner benefits, one-off costs, and non-recurring items so the buyer sees true sustainable earnings. Failure to normalise causes many owners to leave significant value on the table, not because the business is weak, but because the numbers do not tell its real story.

My honest view is that no single valuation method fits every business. Method choice depends on industry, size, stage, and purpose. A pre-revenue SaaS startup needs a different framework than a profitable manufacturing firm. Applying the wrong method does not just produce a wrong number. It signals to buyers that you do not understand your own business.

The founders I have seen achieve the best outcomes treat valuation as a planning tool, not a one-time event before a sale. They track their normalised earnings quarterly, understand their EBITDA multiple relative to sector benchmarks, and engage advisers well before they need a formal figure. That preparation is what separates a confident negotiation from a reactive one.

— Rahamut

Getting your financials in order before a valuation is not a last-minute task. Priceandaccountants works with UK tech founders and growing businesses to prepare the clean, normalised accounts that underpin a credible business appraisal process.

Our advisory and tax planning service acts as an outsourced Finance Director, helping you understand your accounting policies, manage corporation tax exposure, and structure your financials for investor or acquirer scrutiny. We also help founders understand how accounting period selection affects the earnings figures used in valuation. With over 40 years of expertise and a track record of supporting businesses now valued at over £50 million, Priceandaccountants gives you the financial foundation to enter any valuation process with confidence.

Business valuation is the process of estimating what a company is worth in monetary terms using earnings, market data, or asset values. The result is typically expressed as a range, not a single figure.

Business value is determined by applying one or more of the Income, Market, or Asset-based approaches to normalised financial data. The choice of method depends on the company’s size, industry, and the purpose of the valuation.

Normalised earnings, growth prospects, sector multiples, and the quality of recurring revenue have the greatest impact on valuation outcomes. Deal structure elements such as earnouts and working capital targets also affect the final proceeds a seller receives.

A full Valuation Engagement producing a Conclusion of Value is required for formal proceedings such as tax disputes, legal matters, or ESOP schemes. For fundraising or early-stage planning, a less formal Calculation Engagement is often sufficient and less costly.

Enterprise value is the total value of the business before adjusting for debt and cash. Equity value is what shareholders actually receive after deducting net debt, working capital shortfalls, and transaction costs.