TL;DR:

- Management accounts are internal reports that provide current insights into a business’s performance for decision-making. They include key components like profit and loss, balance sheet, cash flow, variance analysis, and tailored KPIs, helping owners track progress and identify risks. Unlike statutory accounts, management accounts are flexible, timely, and used monthly or quarterly to prevent financial drift and support strategic actions.

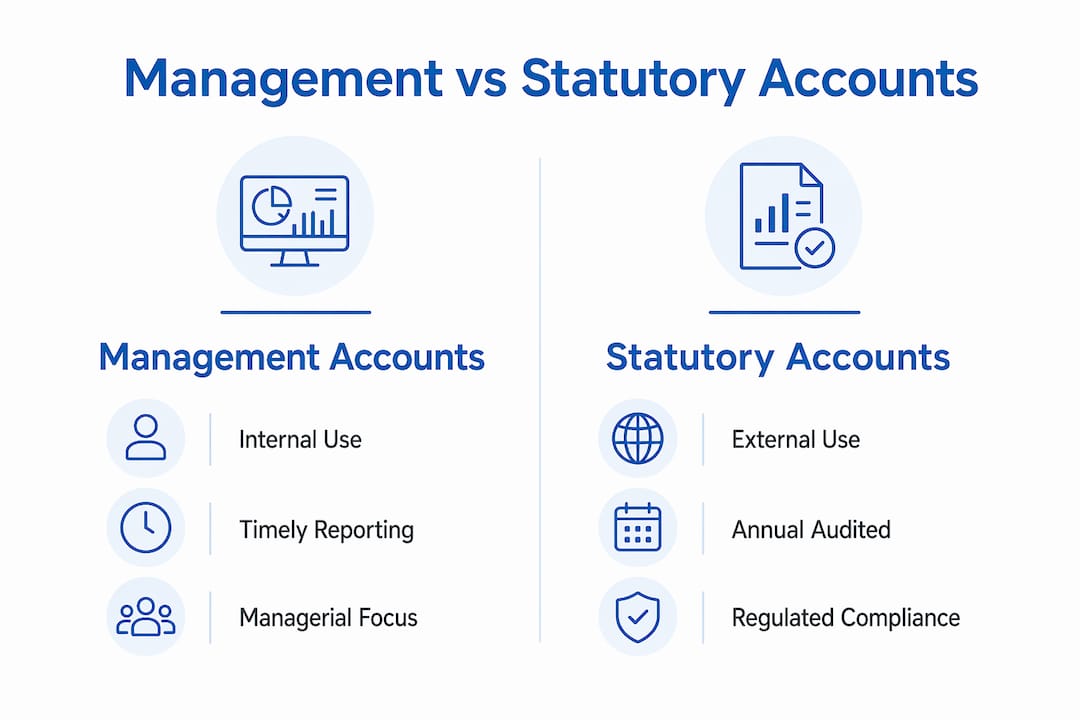

Management accounts are internal financial reports that give business owners a current, accurate picture of how their company is performing. Unlike statutory accounts, which look backwards and satisfy legal obligations, management accounts are built for decision-making right now. With 23,938 registered company insolvencies recorded in England and Wales in 2025, the cost of ignoring timely financial data is not abstract. Management accounts sit between daily bookkeeping and annual compliance, turning raw numbers into the kind of insight that helps you act before problems become crises.

Management accounts are flexible, customised internal reports tailored specifically to help business owners and managers make decisions. They are not regulated by the Companies Act or FRS 102. That means you choose the format, the frequency, and the level of detail that suits your business.

The core components of management accounts typically include:

Core management account components include P&L statements, balance sheets, cash flow statements, variance analysis, and customised KPIs. Each component answers a different question, and together they give you a complete view of business health.

Pro Tip: Choose no more than five to seven KPIs for your management accounts. Too many metrics dilute focus. Pick the ones that directly reflect your biggest risks and opportunities.

The clearest way to understand the difference is through an analogy. Financial statements are like a car’s MOT, proving compliance after the fact, while management accounts are the dashboard gauges giving you real-time readings as you drive. Both matter, but they serve entirely different purposes.

Here is how the two compare directly:

| Feature | Management accounts | Statutory accounts |

|---|---|---|

| Audience | Internal: owners, managers, investors | External: HMRC, Companies House, lenders |

| Frequency | Monthly or quarterly | Annually |

| Regulation | None: fully flexible | Companies Act, FRS 102 |

| Focus | Decision-making and performance | Legal compliance and historical record |

| Precision | Estimates and accruals acceptable | Audited accuracy required |

| Classification | By department, project, or product | By statutory headings |

Management accounts classify data by managerial needs, such as department, project, or product line, rather than the statutory headings mandated by the Companies Act. That flexibility is precisely what makes them useful. You can drill into the profitability of a single product line or a specific client, something a statutory set of accounts would never show you.

Management accounts rely on accruals and estimates for timely reporting, whereas statutory accounts require audited precision. Speed matters more than perfection here. A management pack produced within two weeks of month-end is far more valuable than a perfectly reconciled report that arrives six weeks later.

Pro Tip: Do not wait until your management accounts are perfectly reconciled before sharing them with your leadership team. A 95% accurate report delivered promptly beats a perfect one that arrives too late to act on.

For a deeper look at how annual accounts fit alongside management reporting, the distinction becomes clearer when you see both in practice.

Management accounts protect UK business owners from financial drift. Drift happens when gradual margin erosion or rising costs go unnoticed until they become critical problems. Without monthly or quarterly reporting, you are steering by memory rather than by data.

The practical benefits for small and medium businesses are significant:

The 2025 insolvency figure of 23,938 companies in England and Wales is not a statistic about bad luck. It reflects what happens when business owners lose sight of their financial position until it is too late to correct course.

Producing management accounts that actually drive decisions requires more than assembling numbers. The process needs structure, consistency, and the right level of detail for your business.

Pro Tip: Build your management accounts review into a fixed monthly meeting with your accountant or finance lead. Treat it like a board meeting, even if it is just the two of you. The discipline of a regular review is what turns data into decisions.

Management accounting is a profession focused on partnering in management decision-making and performance management systems. That framing matters. It positions the function not as a back-office task but as a core part of running a business well.

Management accounts are the most practical financial tool available to UK SME owners, providing timely, decision-ready insight that statutory accounts simply cannot deliver.

| Point | Details |

|---|---|

| Core definition | Management accounts are internal reports built for decision-making, not legal compliance. |

| Key components | P&L, balance sheet, cash flow, variance analysis, and tailored KPIs form the standard pack. |

| Statutory difference | Management accounts use estimates for speed; statutory accounts require audited precision under FRS 102. |

| SME importance | Regular reporting prevents financial drift and supports tax planning, pricing, and investor confidence. |

| Practical use | Monthly reviews with variance analysis turn management accounts from a report into a business tool. |

Most business owners I speak with treat management accounts as something their accountant produces and emails over. They glance at the P&L, check whether profit is up or down, and move on. That is a missed opportunity of the first order.

The real value of management accounts is not in the numbers themselves. It is in the conversation the numbers force you to have. When your gross margin drops two percentage points in a single month, that is not just a figure on a page. It is a question that demands an answer: did your costs rise, did your pricing slip, or did your sales mix shift towards lower-margin products? Each answer points to a different action.

Experienced practitioners emphasise that management accounts move the conversation from reporting old news to planning future actions. That shift only happens if you sit down with your accountant and interrogate the variances together. A PDF sent by email does not do that.

The other mistake I see regularly is waiting until the business is in trouble before taking management accounts seriously. By that point, the data confirms what you already feared rather than giving you time to act. The businesses that use management accounts well treat them as a monthly health check, not an emergency diagnostic.

My honest advice: if your management accounts are not changing at least one decision per month, they are not being used properly. Ask your accountant to walk you through the variances. Push for explanations, not just numbers. That is when management accounting becomes genuinely useful.

— Rahamut

Producing management accounts consistently takes time, structure, and financial expertise that most SME owners simply do not have spare. Priceandaccountants works with growing UK businesses to produce timely, accurate management packs that go beyond compliance and into genuine business insight.

From bookkeeping and accounting services to acting as your outsourced Finance Director, Priceandaccountants builds the reporting infrastructure your business needs to make confident decisions every month. Whether you need monthly P&L reports, cash flow tracking, or KPI dashboards tailored to your industry, the team brings over 40 years of expertise to your numbers. Understanding your accounting period and how it shapes your reporting cycle is one of the first things the team will clarify with you. Get in touch to find out how Priceandaccountants can turn your financial data into a tool for growth.

Management accounts are regular internal financial reports that show how a business is performing. They include a P&L, balance sheet, cash flow statement, and KPIs, produced monthly or quarterly to support decisions.

Statutory accounts are annual, regulated by the Companies Act and FRS 102, and filed with Companies House. Management accounts are internal, flexible, and produced as often as the business needs them.

Management accounts are not a legal requirement for UK companies. Statutory accounts are the legal obligation, but management accounts are widely recommended as best practice for any business that wants to stay in control of its finances.

Most growing businesses produce management accounts monthly. Quarterly reporting suits smaller or more stable operations. Consistency matters more than frequency: irregular reporting breaks the trend data needed for variance analysis.

A standard management pack includes a profit and loss statement, balance sheet, cash flow statement, variance analysis against budget, and a set of KPIs tailored to the business and its goals.