TL;DR:

- Financial forecasting helps small businesses project future financial performance and avoid cash crises. It involves estimating revenue, expenses, and cash flow based on operational drivers, with regular updates and detailed assumption tracking. Accurate, driver-based models support better decision-making and financial health for growing companies.

Financial forecasting is defined as the process of projecting a business’s future financial performance using operational drivers, historical data, and validated assumptions to guide decisions on growth, hiring, and capital. For founders and managers of small to medium enterprises, a well-built forecast is not a luxury. It is the difference between reacting to a cash crisis and preventing one. Unlike a static budget, which sets targets, a financial forecast tells you what is actually likely to happen based on how your business operates today.

Financial forecasting is the practice of estimating future revenues, expenses, and cash flows using measurable inputs tied to how your business actually runs. The industry standard term is “financial forecasting,” and it sits alongside budgeting as a distinct discipline. Most companies lack a formal forecasting capability separate from their budgeting process. That gap limits their ability to respond to change.

A budget sets a target. A forecast predicts an outcome. Budgets are typically fixed for a financial year and reviewed annually. Forecasts are living models, updated as new data arrives. For a scaling SME, the forecast is the more useful tool because your business in month nine rarely resembles the business you planned in month one.

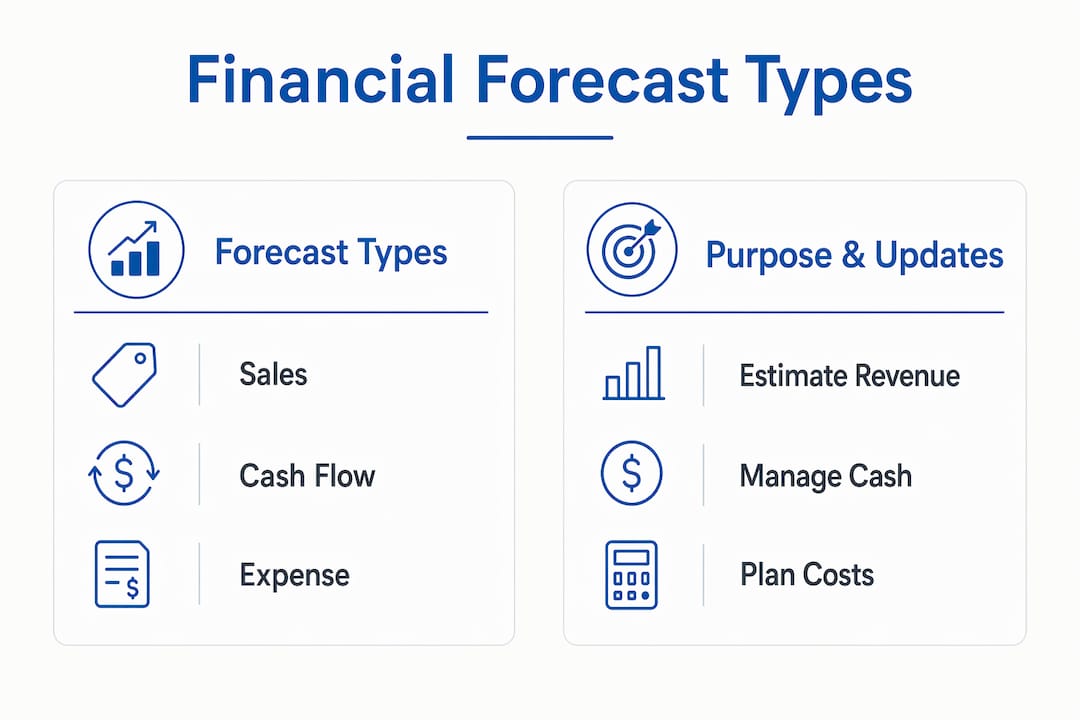

The financial forecasting definition also covers three distinct outputs: a revenue or sales forecast, a cash flow forecast, and a pro forma expense model. Each serves a different purpose, and confusing them is one of the most common planning errors founders make.

The three core forecast types address different questions your business faces at different moments.

| Forecast type | Primary purpose | Recommended update frequency |

|---|---|---|

| Sales forecast | Estimates revenue by product, channel, or customer segment | Monthly |

| Cash flow forecast | Predicts the timing of cash receipts and payments | Weekly (13-week rolling) |

| Pro forma expense forecast | Models fixed and variable costs against projected revenue | Quarterly |

A sales forecast estimates the revenue your business will generate. It influences every other number in your model, from headcount to marketing spend. A cash flow forecast predicts when money arrives and leaves, which is a different question entirely from how much profit you make. A pro forma expense forecast maps your cost base against projected growth, separating fixed costs such as rent from variable costs such as fulfilment.

The importance of financial forecasting becomes clearest when you look at the cash flow forecast. A business can show a healthy profit and loss account while running out of cash because invoices are unpaid or stock is sitting in a warehouse. The cash flow forecast catches that problem before it becomes a crisis.

Driver-based forecasting ties every financial projection to a measurable operational activity. Instead of extrapolating last year’s revenue by a fixed percentage, you build from inputs: number of leads, conversion rate, average deal value, and customer churn. Switching to driver-based methods improves forecast accuracy by an average of 14% compared with simple extrapolation. That improvement comes from grounding projections in reality rather than assumption.

Building a driver-based model follows a clear sequence:

Key assumptions to document include customer acquisition cost (CAC), average revenue per user, gross margin by product line, payment terms, and headcount growth tied to revenue milestones.

Pro Tip: Review your assumption register at least once per quarter. Assumptions that made sense at pre-seed stage often become inaccurate by Series A. Outdated assumptions are the most common source of forecast drift.

The most damaging mistake in financial forecasting is treating profit and cash flow as the same thing. A business can be profitable on an accrual basis but still run out of cash because funds are tied up in receivables, inventory, or tax liabilities. Understanding your net profit figure is useful, but it does not tell you whether you can make payroll next Friday.

A forecast that shows strong profit but ignores the timing of cash movements is not a forecast. It is a wish list. The cash flow statement is where business survival is decided, not the income statement.

The second major pitfall is underestimating the cost of growth. Founders often project revenue doubling without accounting for the additional support staff, infrastructure, and overhead that growth requires. Every growth inflection must have a driver explaining cost and revenue changes; otherwise the forecast lacks credibility with investors and with your own management team.

The seven most common forecasting mistakes are:

Avoiding these errors is not complicated. It requires discipline, a clear process, and a willingness to challenge your own projections. For founders evaluating growth costs in adjacent business models, reviewing franchise finance structures offers a useful parallel on how operational costs scale with revenue.

Best practice is a rolling 12-month forecast updated at least quarterly, supplemented by a 13-week rolling cash flow forecast updated weekly. The quarterly update keeps your strategic picture current. The weekly cash flow update keeps you solvent. These two cadences together cover both the long view and the immediate operational reality.

The rolling format matters as much as the frequency. A static annual forecast becomes stale by february. A rolling model always looks 12 months ahead, which means your planning horizon never shrinks. Forecasts must be living documents connected to real decisions, not filed away after the board meeting.

Connect your forecast directly to decisions. Before hiring a new sales manager, check what your forecast says about revenue in the next two quarters. Before raising a funding round, use your model to show investors the assumptions behind your growth projections. Before committing to a new office lease, run your downside scenario to confirm you can cover the fixed cost. Understanding financial risk at each decision point is where forecasting delivers its clearest value.

Pro Tip: Set a fixed monthly date for your forecast review, treat it as a board-level agenda item, and assign one person as the model owner. Forecasts that have no owner get updated by nobody.

The right tool depends on your stage and complexity, not on what looks most impressive. A well-structured spreadsheet model in Excel or Google Sheets handles most SME forecasting needs up to Series A. The key is building it with driver-based logic from the start, not retrofitting drivers onto a revenue extrapolation later.

Dedicated forecasting platforms offer scenario analysis, real-time data connections, and collaborative updating. They are worth considering when your model has more than three revenue streams or when multiple team members need to update assumptions simultaneously. The features that matter most are:

Advisory support complements any tool. A finance director or external adviser brings the judgement to challenge assumptions that a spreadsheet cannot question. Priceandaccountants acts as an outsourced finance director for growing SMEs, providing the model governance and assumption review that most founders do not have time to do alone. Understanding your cash flows at a granular level is the foundation any tool must build on.

Effective financial forecasting requires driver-based models, linked financial statements, and a regular update cadence to remain a useful management tool rather than a static document.

| Point | Details |

|---|---|

| Forecasting differs from budgeting | A budget sets targets; a forecast predicts outcomes based on operational drivers and current data. |

| Driver-based models outperform extrapolation | Tying projections to measurable inputs improves forecast accuracy by an average of 14%. |

| Profit does not equal cash flow | A business can show profit on paper while running out of cash due to unpaid receivables or tax liabilities. |

| Update cadence determines usefulness | Use a rolling 12-month forecast updated quarterly and a 13-week cash flow updated weekly. |

| An assumption register is non-negotiable | Document every key assumption with its source, owner, and last validation date to maintain model integrity. |

I have worked with founders at every stage from pre-seed to Series A, and the pattern is consistent. The forecast gets built once, usually for a funding round, and then it sits in a folder. Six months later, the business looks nothing like the model, and nobody can explain why because nobody tracked the assumptions.

The uncomfortable truth is that a forecast’s value is not in the numbers. It is in the discipline of building it correctly and updating it regularly. Founders who treat their forecast as a management tool, not a fundraising document, make better decisions. They spot cash shortfalls three months out instead of three weeks out. They know which revenue driver is underperforming before it becomes a board-level problem.

The other thing I see consistently is the hockey stick projection. Revenue is flat for six months, then it doubles in month seven with no operational explanation. Every growth inflection needs a driver. If you cannot name the hire, the campaign, or the product change that causes the step-up, the number is not a forecast. It is optimism.

My advice is to spend less time on the model’s visual presentation and more time on the assumption register. A simple, well-governed model with honest assumptions beats a polished deck built on wishful thinking every time.

— Rahamut

Building a credible financial forecast takes more than a spreadsheet. It takes the right process, the right assumptions, and someone to challenge the numbers before an investor does.

Priceandaccountants works with tech founders and SME managers across London and beyond, acting as an outsourced finance director to build, govern, and update financial models that hold up under scrutiny. From bookkeeping services that feed clean data into your model, to strategic advisory and tax planning that connects your forecast to your funding and tax position, the team covers the full picture. Understanding your accounting period and how it structures your reporting is a practical starting point. Get in touch with Priceandaccountants to build a forecast that actually drives your decisions.

A financial forecast is a projection of your business’s future revenues, expenses, and cash flows based on current data and operational assumptions. It tells you what is likely to happen, not what you want to happen.

A budget sets financial targets for a fixed period, usually a year. A financial forecast predicts actual outcomes based on operational drivers and is updated regularly as conditions change.

The three key components are a sales forecast, a cash flow forecast, and a pro forma expense model. Linking all three to a balance sheet ensures the model remains internally consistent.

SMEs should update their rolling 12-month forecast at least quarterly and their 13-week cash flow forecast weekly to maintain accuracy and support timely decisions.

Financial forecasting for startups identifies cash shortfalls before they occur, supports investor conversations with credible assumptions, and connects hiring and spending decisions to projected revenue growth.