TL;DR:

- A UK subsidiary is a separate legal entity controlled by a foreign parent, offering limited liability and local credibility. It enables registration for UK taxes, compliance, and contractual independence, essential for long-term market operations. While more costly and regulated, a subsidiary is ideal for businesses seeking substantive UK presence, hiring locally, and accessing tax reliefs.

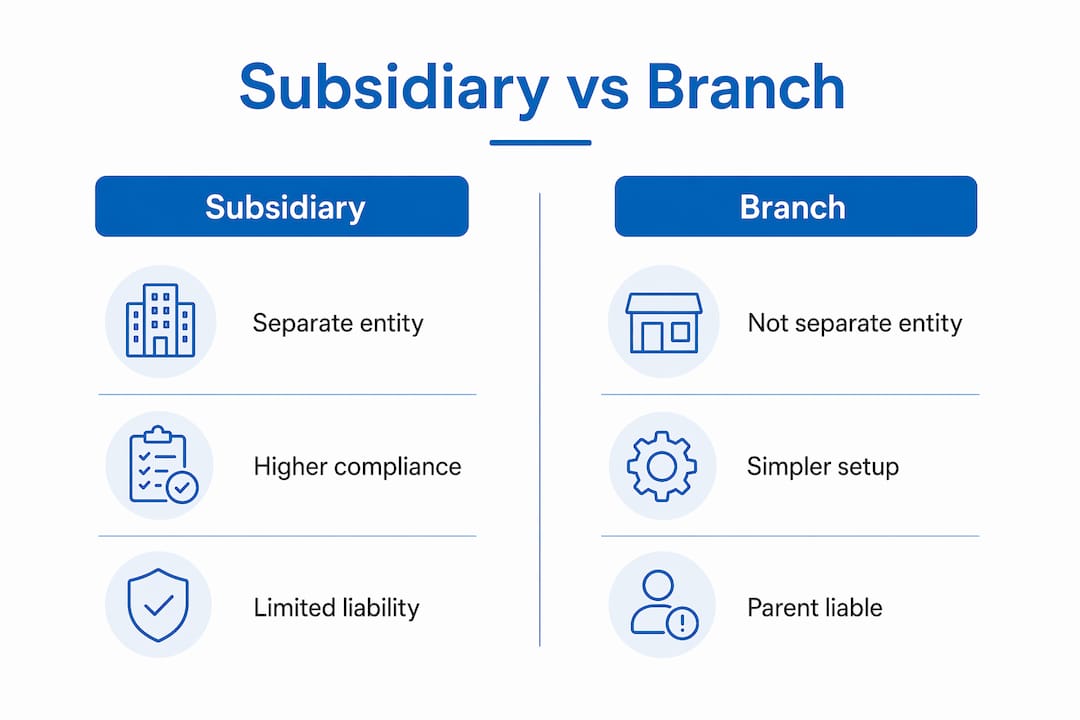

A UK subsidiary is a separate legal entity, incorporated and registered in the UK, that is owned and controlled by a foreign parent company. Unlike a branch, which is simply an extension of the parent, a subsidiary carries its own legal identity, its own liabilities, and its own relationship with Companies House and HMRC. For international founders and business owners asking why set up a UK subsidiary, the short answer is this: it gives you the legal separation, local credibility, and commercial flexibility to operate in the UK as a genuine market participant rather than a visitor.

A UK subsidiary offers limited liability protection that a branch simply cannot match. Subsidiaries have distinct legal personality, which means the parent company’s assets are ring-fenced from any debts or legal claims incurred by the UK operation. If the UK entity runs into difficulty, the financial exposure stays local. That single structural fact changes the risk calculus for most founders.

Beyond liability, the commercial advantages are concrete:

Pro Tip: Open your UK business bank account as early as possible in the setup process. Many banks require the subsidiary to be fully incorporated and have a registered UK address before they will proceed, so delays here can hold up your entire launch timeline.

Subsidiaries do carry higher setup and ongoing compliance costs than branches. That trade-off is worth it for businesses planning a substantive UK presence, but it deserves honest consideration before you commit.

Businesses typically choose between a branch, a subsidiary, or a joint venture when expanding into the UK, and the differences between these structures are material, not cosmetic.

| Feature | Subsidiary | Branch | Joint venture |

|---|---|---|---|

| Legal identity | Separate UK legal entity | Extension of parent company | Separate entity, shared ownership |

| Parent liability | Limited to investment in subsidiary | Unlimited, accrues to parent | Depends on structure |

| Tax filing | UK corporation tax return (CT600) | UK tax on UK profits only | Depends on structure |

| Compliance burden | Higher (annual accounts, directors, governance) | Lower initial setup | Variable |

| Commercial perception | Strong local credibility | Perceived as foreign operation | Depends on partners |

| Hiring UK employees | Straightforward under UK law | Complex, parent entity involved | Depends on structure |

The branch is the lighter-touch option. It is faster to establish and carries fewer ongoing filing obligations, but it exposes the parent to unlimited liability for UK operations. A joint venture introduces a local partner, which can accelerate market entry but creates shared governance and potential for disputes without proper governance documents like shareholders’ agreements. The subsidiary sits in the middle: more administrative work upfront, but a cleaner, more protected structure for long-term UK operations.

Choosing the right UK business structure depends heavily on risk tolerance, governance preferences, and intended market activities rather than a universal best option. There is no single correct answer, but for most founders planning to hire, lease premises, or build a customer base in the UK, the subsidiary is the structure that holds up over time.

UK subsidiary compliance is not optional, and the obligations begin the moment you incorporate. Getting these right from day one prevents penalties and protects the subsidiary’s good standing with both Companies House and HMRC.

Pro Tip: File your annual accounts and CT600 on the same timeline even though the deadlines differ slightly. Keeping both on a single annual compliance calendar reduces the risk of missing either deadline and makes it easier to brief your accountant in one go.

Recent transparency reforms in the UK have also increased the information subsidiaries must disclose in their accounts, particularly around related-party transactions with the parent. This is worth factoring into your governance planning from the start.

The incorporation process defines the subsidiary’s legal structure and governance, so precision at each step matters. The process is faster than most founders expect, often completable within 24 to 48 hours for a straightforward incorporation, but the preparation work takes longer.

For founders who want a deeper walkthrough of the company formation process, the legal and practical steps are well-documented. The key is sequencing them correctly so that banking, tax registration, and operational readiness all align.

A UK subsidiary suits businesses with a clear, long-term commitment to the UK market. A subsidiary generally suits businesses planning local hiring, signing leases, and taking on ongoing UK contracts, and that description covers most founders who are serious about building a UK customer base rather than simply testing the water.

The subsidiary structure makes particular sense when you need to hire UK employees directly, when you are entering contracts with UK customers who expect a locally registered counterparty, or when you are seeking office or commercial premises that require a UK legal entity as the tenant. It also makes sense when the parent company wants a clear legal and financial separation from UK operations, particularly in regulated sectors like fintech, where regulators expect a locally incorporated entity.

A branch may suffice if you are running a short-term project, seconding staff temporarily, or exploring the market before committing to a full presence. The branch carries lower compliance costs and is quicker to wind down. But it is not a substitute for a subsidiary once your UK operations reach any meaningful scale. The liability exposure alone makes it unsuitable for businesses with significant UK revenue or assets.

For UK business compliance essentials and tax planning, the subsidiary also opens doors that a branch does not. UK-specific tax reliefs, including R&D tax credits and the Seed Enterprise Investment Scheme (SEIS), are available only to UK-incorporated companies. If your business is in technology or innovation, those reliefs can represent material capital.

A UK subsidiary is the right structure for foreign businesses that want limited liability, local credibility, and access to UK-specific tax reliefs as they build a permanent market presence.

| Point | Details |

|---|---|

| Limited liability protection | A subsidiary ring-fences the parent from UK debts and legal claims, unlike a branch. |

| Local credibility | UK incorporation improves standing with banks, landlords, and suppliers from day one. |

| Compliance obligations | Annual accounts, CT600, VAT, and PAYE registrations are all mandatory once trading begins. |

| Setup process | Incorporation via Companies House is fast, but tax registrations and banking require additional lead time. |

| Best-fit scenarios | Subsidiaries suit businesses hiring locally, signing UK contracts, or accessing UK tax reliefs like R&D credits. |

The most common mistake I see is founders treating incorporation as the finish line. They file with Companies House, receive their certificate, and assume they are ready to trade. They are not. The corporation tax registration, the bank account, the VAT decision, and the payroll setup are all separate processes, and each one has its own timeline. Getting them out of sequence creates gaps that are expensive to fix later.

The second thing I have observed is that founders consistently underestimate the ongoing compliance burden. Filing annual accounts and a CT600 every year, maintaining statutory registers, and keeping directors’ details current with Companies House are not one-off tasks. They require a system, not just good intentions. The founders who manage this well treat compliance as an operational function, not an afterthought.

My honest view is that most international founders should not attempt this without professional support, at least for the first year. The cost of getting the structure wrong, whether that is a poorly drafted articles of association, a missed HMRC registration, or an incorrect share structure, almost always exceeds the cost of getting expert help upfront. The UK’s tax and company law framework rewards founders who take it seriously from the start.

— Rahamut

Priceandaccountants works with international founders and business owners to make UK subsidiary formation and ongoing compliance straightforward. From incorporation and Companies House filings to HMRC registration, VAT, and payroll setup, the team handles the full compliance cycle so you can focus on building your business. With over 40 years of expertise and a track record of supporting clients now valued at over £50m, Priceandaccountants acts as your financial growth partner from day one. If you are ready to establish your UK presence with confidence, explore the accounting and compliance services available or get in touch for a tailored conversation about your specific structure and goals.

A UK subsidiary is a company incorporated and registered in the UK that is owned or controlled by a foreign parent company. It is a separate legal entity with its own liabilities, directors, and filing obligations.

Incorporation with Companies House can be completed in 24 to 48 hours for a standard private limited company. Additional time is required for bank account opening and HMRC registrations, which can take several weeks.

UK subsidiaries must file annual accounts with Companies House within nine months of their financial year-end and submit a CT600 corporation tax return to HMRC annually. VAT and PAYE registrations apply once the relevant thresholds or activities are triggered.

A subsidiary offers limited liability and stronger local credibility, making it better suited for businesses planning to hire, lease premises, or build a long-term UK presence. A branch carries lower compliance costs but exposes the parent to unlimited liability for UK operations.

Yes. R&D tax credits are available to UK-incorporated companies that meet HMRC’s qualifying criteria. This is one of the significant UK subsidiary advantages for technology and innovation businesses that a branch structure cannot access.