TL;DR:

- Year-end accounting involves finalizing all financial transactions and producing accurate financial statements. Proper preparation and regular reconciliations reduce errors, errors that could lead to penalties or audit corrections. Maintaining clean data and following structured processes ensures compliance with UK reporting deadlines and standards.

Year-end accounting is the process of finalising all financial transactions, reconciling accounts, and producing accurate financial statements at the close of a company’s fiscal year. Known formally as the year-end close, it is the single most important financial reporting event in a business calendar. For UK businesses in 2026, with regulators placing greater scrutiny on governance and operational resilience, getting this process right is not optional. It is the foundation of compliance, investor confidence, and sound financial management.

Year-end accounting finalises the general ledger by completing all transactions, reconciliations, and adjustments needed to produce accurate financial statements. The output includes the balance sheet, income statement, and cash flow statement. These documents are the definitive record of a company’s financial position and performance for the period.

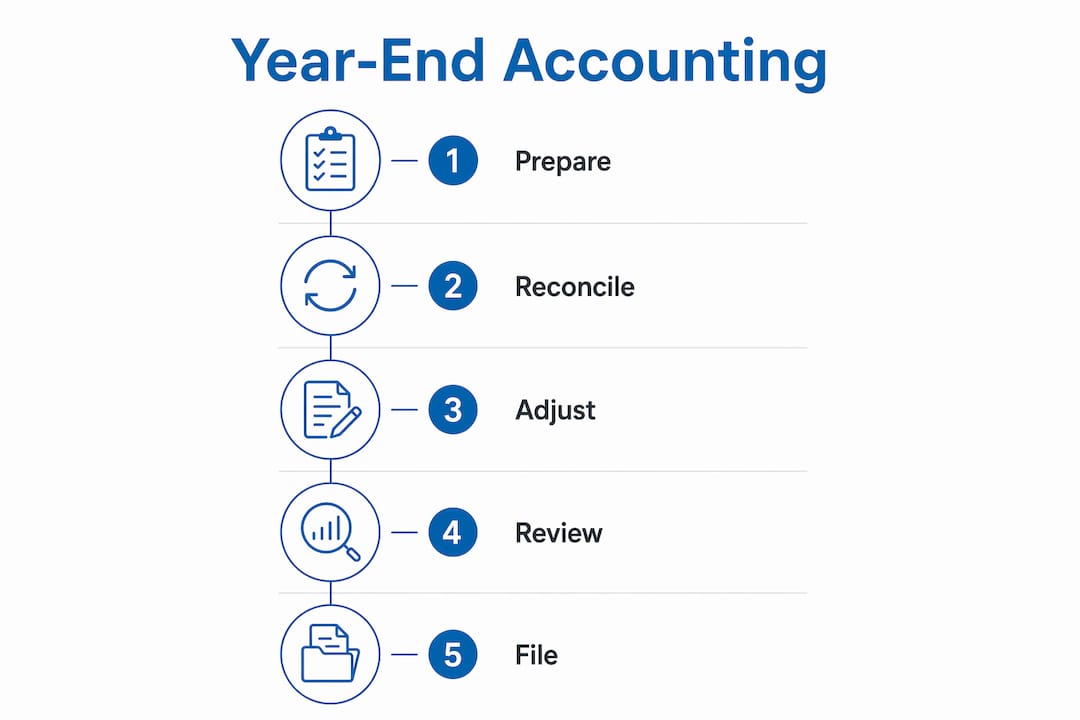

The process follows a structured sequence of activities. Each step builds on the last, and skipping any one of them creates errors that compound at audit time.

Complete all transactions. Post every outstanding invoice, payment, and journal entry before the period closes. Any transaction dated within the fiscal year must appear in that year’s records.

Reconcile subledgers. Match accounts payable, accounts receivable, and payroll subledgers to the general ledger. Discrepancies at this stage signal either data entry errors or missing transactions.

Post year-end adjustments. Record accruals, depreciation charges, prepaid amortisation, and inventory corrections. These entries bring the accounts into line with the matching principle under UK GAAP or IFRS.

Prepare financial statements. Produce the balance sheet, profit and loss account, and cash flow statement. Review them against prior periods to identify anomalies before sign-off.

Management review and approval. Directors or senior finance leads sign off the accounts. This step creates the formal record of oversight that regulators and auditors expect to see.

Archive and lock the period. Close the accounting module in your software to prevent retrospective changes. File all supporting documents in a structured archive.

A phased 90-day preparation window reduces audit adjustment risk and improves filing accuracy. The typical structure runs as follows: data collection at 60 days out, full reconciliation at 45 days, and a final review 15 days before the filing deadline. Starting early is the single most effective change most businesses can make to their year-end process.

Pro Tip: Involve department heads from operations, sales, and HR at least 60 days before year-end. Cross-department coordination prevents the accrual guessing that happens when finance teams chase pending invoices or expense submissions at the last minute.

Year-end adjustments are mandatory accounting entries that correct the books to reflect economic reality at the period close. They are not optional tidying-up exercises. Failing to post adjustments risks auditor-imposed corrections, delayed filing, and reputational damage with lenders or investors.

Common year-end adjustments include:

The distinction between routine monthly entries and year-end adjustments matters. Monthly entries maintain the ledger during the year. Year-end adjustments finalise it. They carry a higher level of scrutiny because they directly affect the figures presented in statutory accounts.

“Year-end adjustments are necessary compliance entries that ensure adherence to accounting frameworks and prevent auditor-imposed corrections.” — AccountingTools

Pro Tip: Review your accounting policies before posting year-end adjustments. Policies govern how items like depreciation rates and revenue recognition are applied, and inconsistency between years triggers auditor questions.

Year-end compliance in the UK means meeting the reporting and filing obligations set by Companies House, HMRC, and, where applicable, the Financial Conduct Authority. The 2026 regulatory environment places particular weight on governance, operational resilience, and demonstrable risk oversight. Regulators expect firms to use the year-end review to reassess risks, update policies, and show that controls are working.

The key compliance tasks for UK businesses at year-end are:

The table below sets out the most common compliance tasks alongside the pitfalls that cause delays.

| Compliance task | Common pitfall |

|---|---|

| Statutory accounts filing | Missing the nine-month deadline due to late reconciliations |

| Corporation tax return | Incorrect treatment of deferred taxation or capital allowances |

| P11D reporting | Omitting benefits such as private medical insurance or company cars |

| VAT reconciliation | Differences between VAT returns and the nominal ledger left unresolved |

| Payroll year-end | Failing to account for salary sacrifice or pension adjustments |

Delaying the tax compliance review risks costly penalties and audit adjustments. Starting 60–90 days ahead allows time to confirm payroll tax treatment, review P11D data, and run a simulated tax return before the actual filing deadline. This approach catches errors when there is still time to correct them without penalty.

The most effective way to reduce year-end pressure is to treat every month-end as a rehearsal. Monthly balance sheet reconciliations prevent the high-volume adjustment crunch that causes mistakes and triggers auditor queries. Businesses that practise a soft close each month arrive at year-end with a ledger that is already largely clean.

Beyond monthly discipline, four strategies make a measurable difference.

Maintain clean data throughout the year. Duplicate suppliers, misclassified transactions, and unreconciled bank lines all compound at year-end. Reviewing the chart of accounts quarterly prevents these issues from accumulating.

Archive documents systematically. Data hygiene activities such as archiving old files, locking period modules, and formalising document retention create immutable audit trails. These records are your evidence in any future tax or regulatory inquiry.

Use accounting software with period-lock controls. Platforms such as Xero allow you to lock closed periods, preventing retrospective changes that corrupt the audit trail. Automated bank feeds and reconciliation tools also reduce manual error.

Formalise the sign-off process. Every material journal entry and reconciliation should carry a preparer name, a reviewer name, and a date. This documentation demonstrates control effectiveness to auditors and satisfies the governance expectations regulators set out for 2026.

Pro Tip: Build a year-end accounting checklist and assign each task an owner and a deadline at least 90 days before close. A shared tracker in a tool like Xero or a project management platform removes ambiguity about who is responsible for what.

For a detailed walkthrough of the preparation steps, the Priceandaccountants guide on how to prepare year-end accounts covers the full UK process with practical timelines. UK tech and fintech founders will also find the year-end tips for founders guide directly relevant to their specific reporting obligations.

Year-end accounting is a structured, compliance-driven process that requires clean data, phased preparation, cross-department coordination, and formal sign-offs to produce accurate financial statements and meet UK regulatory deadlines.

| Point | Details |

|---|---|

| Start 90 days early | A phased preparation window reduces audit risk and improves filing accuracy. |

| Post all adjustments | Accruals, depreciation, and cutoff corrections are mandatory, not optional. |

| Meet UK filing deadlines | Statutory accounts, corporation tax, and P11Ds each carry separate deadlines and penalties. |

| Practise monthly soft closes | Monthly reconciliations reduce the volume of year-end adjustments and audit triggers. |

| Lock and archive at close | Period locks and document archiving create the audit trail regulators expect in 2026. |

Most businesses treat year-end as a deadline to survive rather than a process to manage. That mindset is the root cause of most filing errors and audit delays I have seen.

The businesses that handle year-end well share one habit: they do not wait for year-end to start thinking about year-end. Their finance teams reconcile every month, flag anomalies in real time, and keep the general ledger clean as a matter of routine. When the close arrives, it is not a crisis. It is a confirmation.

The second thing I have observed is that technology only helps if the underlying data is clean. Xero, QuickBooks, and similar platforms are excellent tools. But they cannot fix a chart of accounts that has been misused for 11 months. The discipline has to come first.

The 2026 regulatory environment adds another dimension. Regulators are no longer satisfied with a set of filed accounts. They want evidence that controls were operating throughout the year. That means documented reconciliations, signed-off journals, and a clear record of who reviewed what and when. Businesses that build these habits into their monthly routines will find year-end compliance far less demanding than those who scramble to reconstruct evidence after the fact.

Year-end is also the best moment in the calendar to assess your financial position honestly. The numbers are as accurate as they will ever be. Use them to make decisions, not just to file returns.

— Rahamut

Year-end accounting carries real consequences: missed deadlines, audit adjustments, and penalties that cost far more than the time saved by cutting corners.

Priceandaccountants works with UK tech businesses, start-ups, and growing SMEs to manage the full year-end process, from bookkeeping and reconciliations through to statutory accounts preparation and corporation tax filing. Our advisory and tax planning service helps businesses review their tax position before the deadline, not after it. We also help founders understand their accounting period obligations and structure their reporting cycles for maximum clarity. If your year-end process feels reactive rather than controlled, we can help you change that.

Year-end accounting is the process of closing a company’s financial books at the end of its fiscal year. It involves reconciling all accounts, posting final adjustments, and producing statutory financial statements.

Most UK private limited companies have a financial year ending on 31 march or 31 december, though the accounting period end date is set when the company is incorporated and can vary. Companies House allows businesses to change their year-end date once per year.

Year-end accounts are the financial statements a company prepares at close. A year-end audit is an independent examination of those accounts by a registered auditor to verify their accuracy. Not all UK companies require a statutory audit, but all must file accounts.

A well-prepared year-end close typically takes four to six weeks from the period end date. Businesses that practise monthly reconciliations and maintain clean records throughout the year complete the process faster and with fewer adjustments.

Companies House imposes automatic penalties for late filing, starting at £150 for accounts up to one month late and rising to £1,500 for accounts more than six months late. HMRC applies separate penalties for late corporation tax returns, with interest charged on overdue tax payments.