Navigating UK startup tax compliance can feel overwhelming, especially when founders discover that missing a single registration deadline or misunderstanding relief eligibility can derail funding rounds or trigger unexpected penalties. Many tech startups overlook crucial tax obligations, from timely corporation tax registration to properly documenting R&D claims, putting both investor confidence and compliance at risk. This guide clarifies what startup tax compliance means in 2026, outlines your key obligations, and reveals optimisation strategies that support funding readiness and sustainable growth.

| Point | Details |

|---|---|

| Registration deadlines | Companies must register for corporation tax within 3 months of starting activity to avoid penalties |

| R&D documentation | Stronger evidence and narrative are essential under tighter HMRC scrutiny introduced in 2023 |

| EIS relief changes | Annual investment limits doubled in 2026 whilst VCT relief dropped to 20%, reshaping funding strategies |

| Tax payment timing | Corporation tax must be paid within 9 months and 1 day after your accounting period ends |

| Efficient remuneration | Combining modest salary with dividends typically optimises tax position for founder directors |

Startup tax compliance means fulfilling all UK tax registration, filing, and payment duties accurately and on time. It’s not just about paying what you owe, it’s about meeting every regulatory requirement from the moment your company begins activity. Companies must register for corporation tax with HMRC within 3 months of starting business activity, whether that’s trading, buying assets, or receiving income.

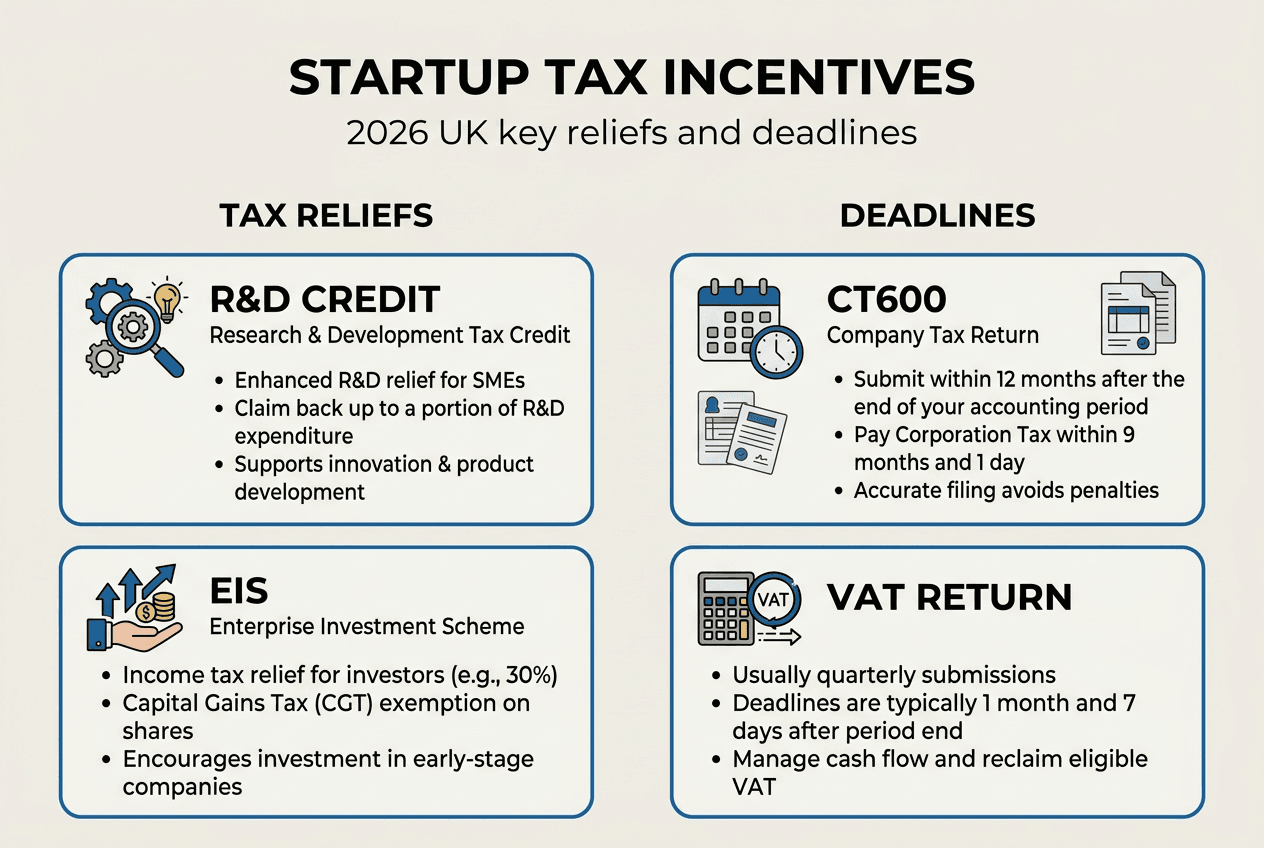

Your key tax events include several critical deadlines. You must file your CT600 return within 12 months of your accounting period ending. Corporation tax liability starts from the date a company begins any activity, including buying or selling assets, receiving income, or trading, even if you haven’t generated profit yet. Payment must reach HMRC within 9 months and 1 day after your accounting period closes.

The Corporation Tax rate in 2026 applies 25% on profits over £250,000 and 19% if profits are £50,000 or less. Companies with profits between these thresholds face marginal relief calculations. Understanding these rates helps you forecast tax liabilities and plan cash flow effectively.

Missing these deadlines carries serious consequences. Late registration triggers automatic penalties. Late filing incurs escalating fines. Late payment adds interest charges that compound quickly. For startups preparing for funding rounds, demonstrating clean compliance history reassures investors that your financial house is in order. Keeping meticulous records and setting calendar reminders for each deadline protects both your compliance status and your reputation with potential backers.

UK startups can access powerful tax incentives that reduce costs and attract investment, but recent regulatory changes demand careful attention. R&D tax relief remains critical for innovation-driven companies, yet HMRC views R&D tax relief as material public spending, leading to tighter policing of claims. From April 2023 onwards, HMRC implemented reforms improving compliance and reducing abuse like limits on overseas subcontracted R&D costs and Additional Information Form requirement.

These reforms mean your R&D tax credits claims need robust documentation. You must demonstrate genuine innovation, maintain detailed project records, and clearly separate qualifying activities from routine development. The Additional Information Form requires granular breakdowns of costs and activities, raising the bar for claim quality. Weak claims now face rejection or lengthy enquiries that delay cash flow benefits.

Enterprise Investment Scheme (EIS) and Venture Capital Trust (VCT) schemes offer different investor incentives with distinct recent changes. VCT income tax relief will fall to 20 percent, reducing capital availability to startups as prior similar cuts caused 65% fundraising fall. Meanwhile, annual and lifetime EIS-eligible capital limits increased significantly from 2025 to 2026 for standard and knowledge intensive companies.

| Feature | EIS | VCT |

|---|---|---|

| Income tax relief | 30% on investments up to £1m (£2m for knowledge intensive) | 20% (reduced from 30% in 2026) |

| Annual investment limit | Doubled in 2026: £250k standard, £500k knowledge intensive | £200k per investor |

| Capital gains exemption | Yes, after 3 year holding | Yes, on VCT share disposals |

| Recent impact | Increased limits boost fundraising potential | Lower relief may reduce investor appetite |

To maximise EIS relief and protect investor benefits, follow these steps:

Pro tip: Maintain accurate documentation and timing for relief eligibility to protect investor benefits over the three year holding period, as retroactive invalidation can destroy investor returns and your fundraising reputation.

Tax reliefs significantly ease investment attraction by improving investor returns, but they demand diligent compliance. Founders who understand the nuances and maintain proper records unlock funding advantages whilst those who treat reliefs casually risk costly failures. For detailed guidance on maintaining compliance, review our R&D reporting guidance and UK tax deadlines for startups 2026.

Daily tax management and smart remuneration strategies directly impact your startup’s cash flow and founder take-home pay. Understanding when obligations trigger and how to structure payments saves money and administrative headaches.

VAT registration is mandatory if turnover exceeds £90,000, with a standard rate of 20%. Once registered, you charge VAT on sales, reclaim VAT on business purchases, and submit returns quarterly or monthly depending on your scheme. Voluntary registration before hitting the threshold can benefit businesses with significant reclaimable input VAT, though it adds administrative burden.

Corporation tax payment follows strict timelines. You must pay within 9 months and 1 day after your accounting period ends, regardless of when you file your CT600. Filing the return itself must happen within 12 months. This split timeline catches many founders off guard, as they assume filing and payment happen together. Missing payment deadlines triggers interest charges immediately, whilst late filing brings fixed penalties that escalate with delay.

Founder remuneration requires balancing multiple taxes. Directors and shareholders pay Income Tax, National Insurance, and Dividend Tax on money taken out, with dividend tax rates varying by band. Current UK dividend rates stand at 8.75% for basic rate taxpayers, 33.75% for higher rate, and 39.35% for additional rate.

Tax-efficient remuneration strategies include:

| Tax type | Rate/threshold | Payment deadline | Applies to |

|---|---|---|---|

| Corporation tax | 19% (profits under £50k), 25% (over £250k) | 9 months + 1 day after period end | Company profits |

| VAT | 20% standard rate | Quarterly or monthly | Sales over £90k turnover |

| Income Tax on salary | 20%/40%/45% on bands above £12,570 | Via PAYE monthly | Director salary |

| National Insurance | 13.25% employee, 15.05% employer | Via PAYE monthly | Director salary |

| Dividend tax | 8.75%/33.75%/39.35% on bands | Self-assessment by 31 Jan | Dividends to shareholders |

Pro tip: Use accounting software that connects directly to HMRC to automate returns and avoid mistakes, with platforms like FreeAgent or Xero reducing filing errors and late penalties significantly.

Efficient tax management isn’t about aggressive avoidance, it’s about understanding the rules and structuring affairs sensibly. Founders who grasp these mechanics keep more of what they earn whilst maintaining full compliance. For comprehensive workflow guidance, explore our startup tax planning workflow and accounts basics for startups.

Startups frequently stumble on tax compliance details that seem minor until they derail funding or trigger penalties. Understanding these pitfalls and implementing best practices protects both your compliance status and investor confidence.

Common EIS mistakes carry severe consequences. Mistakes around company age, qualifying activity, share issues, or investor connections can invalidate EIS income tax relief and capital gains relief, sometimes years after investment. A founder who issues preference shares with excessive rights, accepts investment from a former consultant who worked for the company, or pivots into excluded activities can destroy investor tax benefits retroactively. When this happens, investors face unexpected tax bills and your reputation as a fundraising partner evaporates.

Corporation tax filing errors also create problems. Even if a company makes no profit, it usually still needs to file a CT600 to avoid penalties. Many founders assume dormant status or zero profit means no filing obligation, but HMRC requires annual returns regardless. The penalties for non-filing start at £100 and escalate with delay, adding unnecessary costs.

R&D claims demand exceptional rigour under current scrutiny. The strongest R&D claims are like a mini audit, with evidence first, then narrative, then numbers. Weak claims that lack technical detail, fail to demonstrate uncertainty resolution, or include non-qualifying costs face rejection. HMRC now requests extensive supporting documentation, project logs, and technical explanations. Claims submitted without this foundation waste time and risk enquiries that freeze relief payments for months.

Best practices for maintaining compliance and investor trust:

Pro tip: Early specialist tax advice can help avoid costly retroactive claim invalidations and fund loss, as fixing problems before they crystallise costs far less than unwinding completed transactions.

Funding readiness requires more than compelling pitch decks and growth metrics. Investors conduct tax due diligence, examining your compliance history, relief eligibility, and structural soundness. Clean records signal professional management. Messy compliance suggests operational weaknesses that might plague other business areas. By treating tax compliance as a core competence rather than an administrative burden, you build the foundation for successful fundraising and sustainable growth. Our tax planning guide for startups provides detailed frameworks for establishing these systems.

Managing startup tax compliance whilst building your business stretches founder bandwidth thin. Price & Accountants specialise in lifting this burden for UK tech startups, providing tailored tax advisory and planning services designed specifically for high-growth companies navigating funding rounds.

Our bookkeeping services integrate seamlessly with HMRC systems, automating filings and eliminating the errors that trigger penalties. We handle R&D claims with the rigorous documentation HMRC now demands, manage EIS advance assurance applications, and ensure corporation tax and VAT obligations meet every deadline. Having supported over 20 startups from inception to valuations exceeding £50m, we understand the compliance challenges founders face at each growth stage. Discover how we work with startups to optimise tax positions whilst maintaining investor-ready compliance standards.

Companies must register for corporation tax within 3 months of starting business activities such as trading, buying assets, or receiving income. Missing this deadline triggers automatic penalties even if no tax is owed. Registration starts your compliance timeline for filing and payment obligations.

VCT income tax relief falls to 20% in 2026, potentially reducing investor appetite as historical cuts caused fundraising to drop 65%. Conversely, EIS annual and lifetime investment limits have doubled, making it easier to raise capital from individual investors. Understanding these changes helps founders choose optimal funding structures and set realistic investor expectations.

HMRC requires all limited companies to file CT600 annual returns regardless of profit levels. Failure to file triggers penalties starting at £100 and escalating with delay, even when no tax is owed. Timely filing maintains your compliance status, avoids unnecessary fines, and demonstrates operational discipline to potential investors conducting due diligence.

You need comprehensive project records demonstrating technical uncertainty, innovation attempts, and qualifying costs. This includes project plans, technical reports, meeting notes, cost breakdowns separating qualifying from non-qualifying expenditure, and narrative explanations of challenges overcome. HMRC’s Additional Information Form requires granular detail, so treating documentation as audit-ready from project start strengthens claims significantly.

Most founder directors benefit from taking a modest salary around £12,570 to maintain state pension credits without triggering Income Tax or National Insurance, then extracting remaining income as dividends. Dividends face lower tax rates than salary, though you must ensure the company has distributable profits and follows proper dividend declaration procedures. Your optimal mix depends on total income, other employment, and personal tax position.