TL;DR:

- Most small businesses rely on single-entry bookkeeping, which hides errors and prevents full financial reporting.

- Double entry accounting records each transaction twice, maintaining balance and ensuring accurate financial statements.

- Understanding this system helps business owners make better decisions and meet regulatory and lender requirements.

Most small business owners start out tracking money the same way they manage their personal finances: one column in, one column out. It feels logical. But this single-entry approach conceals a serious flaw. It cannot tell you whether your figures are wrong, what you owe, or what you own. What is double entry accounting, and why does it fix these problems? It is the method that underpins every reliable set of business books, from a one-person consultancy to a FTSE 100 company. Understanding how it works gives you a financial picture you can actually trust.

| Point | Details |

|---|---|

| Every transaction is recorded twice | Each entry has a corresponding debit and credit, keeping your books balanced at all times. |

| The accounting equation must hold | Assets always equal liabilities plus equity, and double entry preserves this in every transaction. |

| Error detection is built in | If total debits do not equal total credits, you know immediately something is wrong. |

| Single entry leaves gaps | Single-entry bookkeeping cannot produce a balance sheet or catch most recording errors. |

| Software helps but structure matters | Accounting software alone will not save you if your chart of accounts is poorly organised from the start. |

Double entry accounting is a system in which every transaction is recorded twice, once as a debit and once as a credit of equal value. The logic behind this is not complexity for its own sake. It reflects a simple truth: every financial event has two sides. When you receive cash from a customer, your cash goes up and your outstanding receivable goes down. Recording both movements gives you a complete picture of what actually happened.

The entire double entry system rests on one equation:

Assets = Liabilities + Equity

This is the accounting equation, and it must always hold true. If your business holds £80,000 in assets and owes £30,000 in liabilities, your equity is £50,000. Every single transaction you record must leave this equation balanced. That constraint is precisely what makes double entry so powerful.

Within this system, transactions flow through a general ledger, which is a master record of all your accounts. Each account can be visualised as a T-account, with debits on the left side and credits on the right. The accounts themselves fall into five main categories:

Pro Tip: When you are setting up your books for the first time, map out all five account categories before you enter a single transaction. Getting this structure right from day one prevents hours of correction later.

This is where most people get confused, and understandably so. In everyday banking, a credit to your account means money coming in. In accounting, debits and credits do not work that way. They simply describe which side of the ledger an entry goes on: debit is left, credit is right. What effect they have depends entirely on the type of account.

Here is how the rules work across the five account types:

A practical double entry accounting example makes this concrete. Say you purchase £1,000 of office supplies with cash. You debit Office Supplies (an asset, going up by £1,000) and credit Cash (an asset, going down by £1,000). The books stay balanced. Or suppose you sell services worth £2,500 and the client pays immediately. You debit Cash (up £2,500) and credit Revenue (up £2,500). As debits must always equal credits, the system flags any mistake automatically.

Pro Tip: Forget how your bank uses the words “debit” and “credit.” In accounting, these are positional terms, not value judgements. Debit is left. Credit is right. The impact on your balance depends on which account type you are working with.

Another useful double entry accounting example: your business takes out a £10,000 bank loan. You debit the Bank account (asset up by £10,000) and credit the Loan Payable account (liability up by £10,000). Both sides move equally, and your equation stays perfectly balanced.

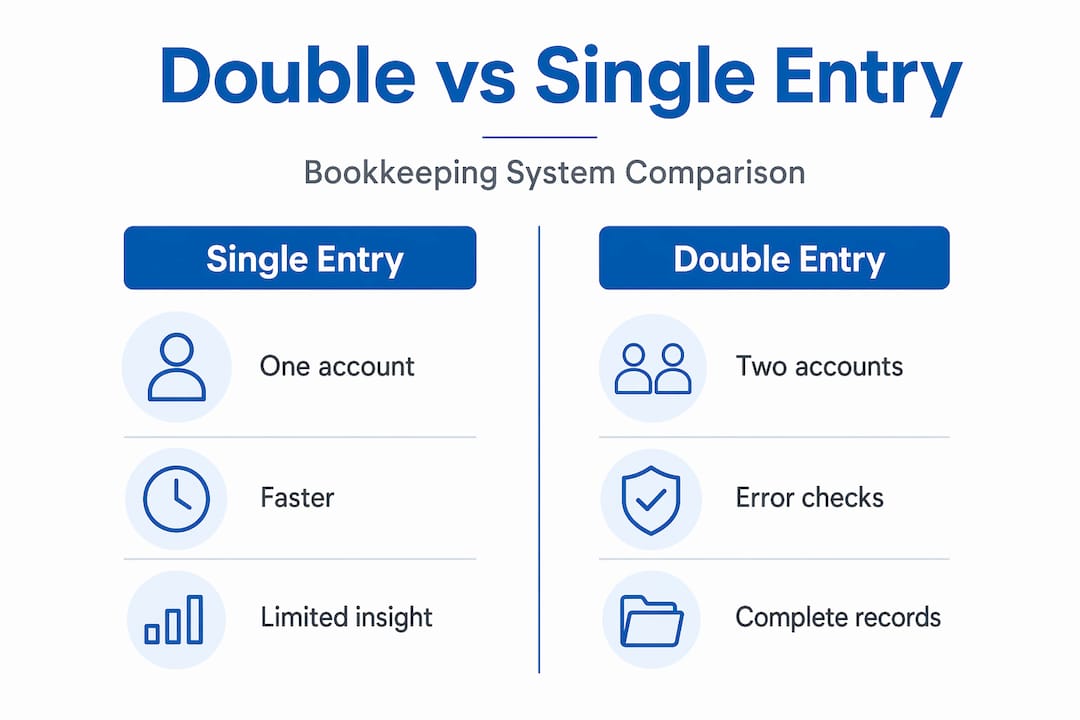

Single-entry bookkeeping records only one side of each transaction, typically just income and expenditure. It is quicker to maintain but carries real limitations. Single-entry lacks the accuracy to catch errors or produce a full set of financial statements. You can tell whether you made money this month, but you cannot produce a balance sheet, reconcile your accounts, or show a lender a credible snapshot of the business.

Here is a direct comparison:

| Feature | Single-entry bookkeeping | Double entry accounting |

|---|---|---|

| Entries per transaction | One | Two (debit and credit) |

| Error detection | Minimal | Built-in via balance check |

| Financial statements | Income only | Full: P&L, balance sheet, cash flow |

| Suitable for lenders and investors | Rarely | Yes |

| Regulatory compliance | Limited | Generally required for limited companies |

The benefits of double entry accounting extend well beyond catching arithmetic mistakes. Comprehensive financial statements are what banks, investors, and HMRC expect when they scrutinise your records. If you are seeking funding, applying for a business loan, or planning to scale, double entry is not optional. It is the foundation everything else is built on.

Starting a double entry system does not require an accounting degree. It does require a deliberate setup. Here are the core steps to do it properly:

For practical guidance on getting your books organised from the start, the bookkeeping best practices guide from Priceandaccountants is worth reading alongside this article.

Pro Tip for software users: Even with Xero or similar tools, review your transaction categories weekly. Software can post entries to the wrong account without triggering any alerts, and small misclassifications accumulate quickly.

Here is something that surprises many business owners: balanced books are not the same as correct books. Transactions can be recorded wrongly yet still appear mathematically balanced. If you debit Marketing Expenses instead of Equipment when buying a laptop, your totals still balance. But your balance sheet is wrong, and so is your tax calculation.

The most common mistakes tend to be:

Misclassification of accounts, where expenses land in the wrong category and distort your profit figures. Duplicate entries, which happen when a transaction is recorded twice without a corresponding reversal. Timing errors, where revenue or costs are recorded in the wrong accounting period. And data entry mistakes, where the wrong amount is entered on both sides.

Regular reconciliation with your bank statements is the best defence against all of these. If your bank shows a payment going out that does not match a ledger entry, something is wrong. Find it immediately. If debits and credits do not match, your ledger contains an error you must resolve before closing your accounts.

Pro Tip: Set a fixed date each month to reconcile your accounts, ideally within five working days of your bank statement arriving. Treating it as a recurring appointment rather than an optional task keeps errors small and manageable.

If you spot persistent discrepancies or your books consistently fail to reconcile, that is a signal to bring in professional help. The common accounting mistakes article from Priceandaccountants covers several scenarios where DIY bookkeeping causes real financial damage.

I have worked with dozens of founders and small business owners over the years, and one pattern repeats itself constantly. They delay adopting a proper double entry system because it looks complicated, and then spend twice as long untangling the mess later. The irony is that the complexity they fear is actually the complexity they create by avoiding it.

What I have found is that business owners who understand the principles of double entry, even at a basic level, make far better financial decisions. They spot when a profit figure looks suspicious. They question why cash is tight despite a supposedly good trading month. They understand the difference between profit and cash flow in a way that people relying on a simple income spreadsheet simply cannot.

The system is not perfect. Human error and misclassification remain vulnerabilities no matter how carefully you set things up. But the discipline of recording every transaction twice forces a rigour that single-entry never demands. In my experience, that rigour alone separates the businesses that scale from the ones that muddle through.

You do not need to become an accountant. You need to understand what your numbers are telling you. Double entry gives you that language.

— Rahamut

Setting up a double entry system correctly from the start makes everything that follows, from VAT returns to investor due diligence, significantly simpler. But getting the structure right requires experience that most new business owners have not yet had the chance to build.

At Priceandaccountants, we work with tech start-ups, growing SMEs, and international founders to put proper bookkeeping foundations in place from day one. Our bookkeeping services cover everything from chart of accounts setup to monthly reconciliation and trial balance preparation, using Xero and modern cloud tools that give you real-time visibility over your finances. If you need broader support, our accounting services include year-end accounts, VAT management, and strategic financial advice tailored to where your business is right now. Get in touch to find out how we can help you build books you can actually rely on.

Double entry accounting is a bookkeeping method where every financial transaction is recorded in at least two accounts: once as a debit and once as a credit of equal value. This keeps your books balanced and provides a complete record of your business finances.

Every transaction affects two accounts. Debits increase assets and expenses while credits increase liabilities, equity, and revenue, so each transaction always has equal and opposite entries that maintain balance.

Single entry records only one side of each transaction and cannot produce a full set of financial statements. Double entry records both sides, detects errors automatically, and generates the balance sheet and profit and loss statement that lenders and investors require.

A transaction can be posted to the wrong account but still use the correct amounts on both sides, leaving totals balanced while the underlying figures are wrong. Regular bank reconciliation and review of account classifications are needed to catch these errors.

Limited companies in the UK are legally required to maintain full accounting records, which in practice means double entry. Sole traders are not legally obliged, but double entry enables complete financial statements that are almost always necessary for growth, funding, and compliance.