TL;DR:

- Treating HMRC compliance as an ongoing process rather than a yearly task helps businesses avoid penalties and build trust.

- Maintaining accurate records, submitting timely returns, and engaging registered advisers are essential steps for staying compliant.

Getting HMRC compliance wrong is not just a paperwork problem. It can mean financial penalties, reputational damage, and in serious cases, criminal investigation. Yet many UK business owners treat compliance as a once-a-year scramble rather than an ongoing process. Knowing how to ensure HMRC compliance gives you control over your tax position, reduces the risk of an unwanted compliance check, and keeps your business on a sound legal footing. This guide walks you through what compliance actually involves, how to prepare for it, and how to handle HMRC professionally when they come knocking.

| Point | Details |

|---|---|

| Compliance is year-round | HMRC obligations span VAT, PAYE, corporation tax, and more, requiring consistent attention throughout the year. |

| Records are your foundation | Accurate, up-to-date financial records are the single most reliable defence during any HMRC compliance check. |

| Cooperation reduces penalties | HMRC reduces penalties when taxpayers cooperate fully and respond promptly to requests. |

| Voluntary disclosure is powerful | Proactively disclosing errors to HMRC can significantly reduce penalty amounts and protect your reputation. |

| Expert support matters | Using a registered tax adviser protects your legal position and prevents costly escalations. |

At its core, HMRC compliance means meeting all the legal obligations you have as a business to report, calculate, and pay the correct amount of tax. It covers a broader range of responsibilities than most business owners realise.

The key obligations include:

Understanding HMRC regulations means recognising that compliance checks verify tax accuracy and completeness across all of these areas, not just one. HMRC may open a check when it spots a mismatch between your returns, receives information from a third party, or identifies an unusual pattern in your filings.

What makes compliance checks particularly significant is their potential scope. Checks can escalate from straightforward enquiries into multi-year audits covering potential fraud, depending on what HMRC finds at each stage. A minor inconsistency that goes unexplained can quickly become a much larger investigation.

Pro Tip: Do not wait for HMRC to contact you before reviewing your filings. A quarterly internal review of your VAT returns, payroll records, and management accounts can catch discrepancies before they become triggers for investigation.

Most compliance failures do not happen because business owners are dishonest. They happen because preparation is poor. Meeting HMRC standards starts long before any return is due.

Here are the essential preparations every business should make:

Maintain meticulous records. Accurate record-keeping is the foundation of every compliance obligation. This means retaining bank statements, invoices, receipts, payroll records, and contracts for at least six years.

Use cloud accounting software. Platforms such as Xero create a real-time, auditable trail of your financial activity. They reduce manual errors and make it far easier to produce accurate returns quickly.

Appoint a registered tax adviser. From 18 May 2026, tax advisers must be registered to interact with HMRC on behalf of clients. Appointing an authorised agent gives you a professional representative and protects your legal position.

Stay on top of deadlines. Create a tax calendar covering every filing and payment deadline relevant to your business. Missing a deadline is one of the most common and entirely avoidable triggers for penalties.

Monitor legislative changes. Tax law in the UK changes regularly. Budget announcements, HMRC consultations, and updated guidance can all affect your obligations.

The table below shows the key compliance areas, along with their typical filing deadlines and record retention requirements:

| Tax area | Key deadline | Records to retain |

|---|---|---|

| Corporation tax | 12 months after accounting period end | Company accounts, invoices, contracts |

| VAT | One month and seven days after quarter end | VAT returns, purchase and sales invoices |

| PAYE | Monthly or quarterly to HMRC | Payroll records, P60s, P11Ds |

| Self Assessment | 31 January (online) | Income records, expenses, bank statements |

| CIS | 19th of each month | Subcontractor verification records |

Knowing your deadlines and the records you need to support them transforms compliance from a reactive scramble into a managed process.

Preparation gets you ready. Execution is where compliance is actually demonstrated. Here is how to carry out the core compliance processes correctly.

File returns accurately and on time. Check every return against your underlying records before submitting. A common error is claiming VAT on ineligible expenses or under-reporting income due to bank reconciliation gaps.

Respond to HMRC correspondence without delay. When HMRC contacts you, do not ignore it. Even a routine letter asking for clarification can escalate if left unanswered. Acknowledge receipt and respond within the timeframe given.

Manage payment obligations. If you cannot pay a tax bill in full, contact HMRC before the deadline. Time to Pay arrangements allow businesses to spread payments, and HMRC is generally receptive to these requests when approached proactively. Specialist advisers help negotiate these arrangements and protect your legal position.

Consider voluntary disclosure. If you identify an error in a previously submitted return, disclosing it voluntarily is nearly always the right move. Voluntary disclosures enable cooperative resolution and can substantially reduce the penalties HMRC would otherwise impose. Acting first, before HMRC discovers the error independently, gives you far greater control over the outcome.

Negotiate information requests carefully. During a compliance check, HMRC may ask for documents or access to information. You have the right to discuss the scope and timing of these requests. Providing everything HMRC asks for in one organised submission is almost always more effective than a fragmented response over several weeks.

Pro Tip: If HMRC opens a compliance check, do not start providing documents before you understand exactly what is being requested. Seek professional advice first so that your response is targeted, complete, and does not inadvertently open up new areas of enquiry.

Even well-run businesses make compliance mistakes. The difference between a minor correction and a serious penalty often comes down to the type of mistake and how it is handled afterwards.

The most frequent errors that business owners make include:

Ignoring information notices. Failing to comply with an HMRC information notice can result in penalties and trigger a more intensive investigation. If you receive one, treat it as a legal obligation, not a request.

Incomplete or misleading disclosures. Partial disclosures that omit relevant information can be treated by HMRC as deliberate concealment. A disclosure must be thorough to gain the full benefit of reduced penalties.

Using unregistered tax advisers. As noted above, from May 2026, unregistered advisers interacting with HMRC on your behalf can expose your business to sanctions and penalties of up to £10,000. Always verify your adviser’s registration status.

Treating careless errors as harmless. HMRC distinguishes between careless, deliberate, and concealed inaccuracies when calculating penalties. Careless errors still attract penalties, typically between 0% and 30% of the unpaid tax, so a culture of careful, reviewed reporting matters.

Failing to take specialist advice early. Many business owners delay seeking professional help until a situation has already escalated. Early specialist advice on complex checks protects your legal position and often prevents unnecessary escalation entirely.

Understanding the best practices for HMRC compliance means recognising that transparency and cooperation are not just ethical stances. They are genuinely the most cost-effective strategy when things go wrong.

One-off compliance efforts are not enough. The businesses that consistently avoid penalties are the ones that treat compliance as a continuous process rather than an annual event. You can learn more about how tax compliance fuels growth by making it a structural part of your business strategy.

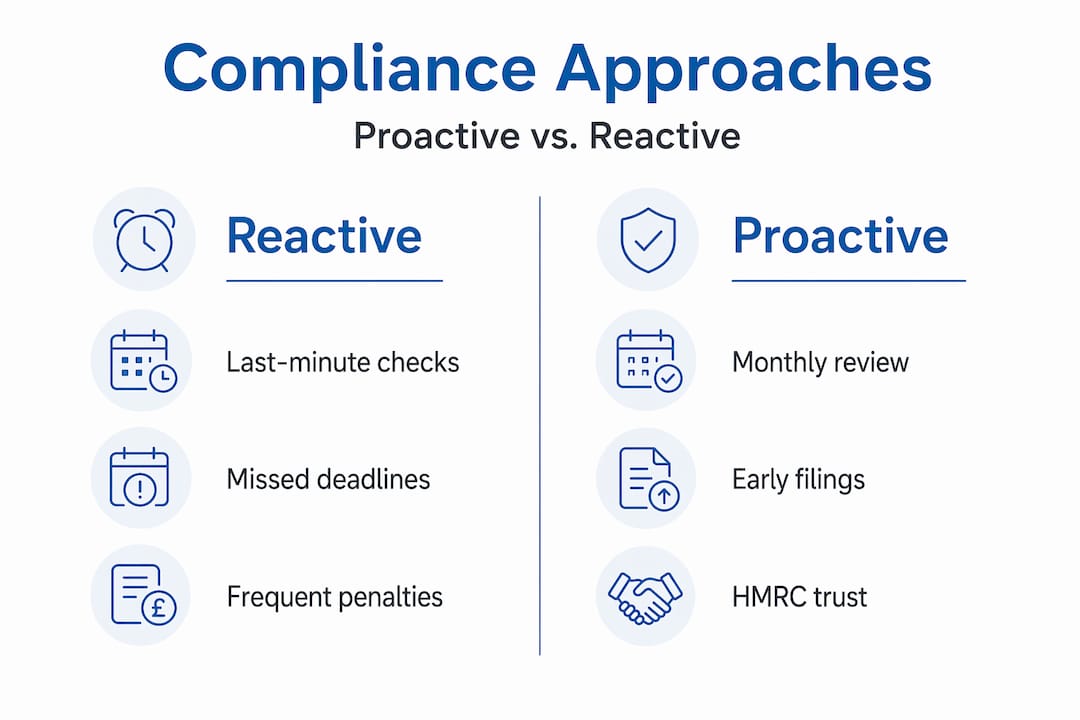

![]()

The table below illustrates the difference between a reactive and a proactive compliance approach:

| Reactive approach | Proactive approach |

|---|---|

| Review records only before filing deadlines | Monthly reconciliation of accounts and VAT records |

| Wait for HMRC to raise concerns | Conduct quarterly internal compliance reviews |

| Respond to legislative changes after they take effect | Subscribe to HMRC updates and act on changes before deadlines |

| Address errors only when identified by HMRC | Identify and voluntarily disclose errors as soon as they arise |

| Seek advice only during a compliance check | Retain a registered adviser for ongoing support and planning |

The proactive column is not just about avoiding penalties. It builds a positive relationship with HMRC, which matters more than many business owners realise. A business with a consistent history of accurate, timely filings is simply less likely to be selected for detailed scrutiny.

For growing businesses, SME compliance tips show how meeting your obligations and maximising available reliefs such as R&D tax credits and the Annual Investment Allowance can go hand in hand.

I have worked with a wide range of UK businesses on their tax compliance, and one pattern I see repeatedly is this: business owners who treat HMRC as an adversary consistently come off worse than those who treat compliance as a management discipline.

The most counter-intuitive lesson I have learned is that voluntary disclosure is a strategic tool, not a confession of failure. When a business proactively identifies an error and brings it to HMRC before being asked, it fundamentally changes the dynamic of the entire relationship. I have seen businesses avoid serious financial and reputational damage simply by acting decisively and transparently before HMRC came looking.

The other misconception I encounter constantly is that HMRC compliance is purely about not making mistakes. It is not. It is about demonstrating, through good records, timely filings, and professional representation, that you are a reliable and trustworthy participant in the tax system. That reputation has real, tangible value for your business. It affects your ability to attract investment, secure lending, and operate without disruption. Compliance is not a cost of doing business. It is an asset.

— Rahamut

Running a business leaves little time to monitor every HMRC deadline, legislative change, and compliance obligation across corporation tax, VAT, PAYE, and beyond. That is exactly where Priceandaccountants comes in.

At Priceandaccountants, we provide expert accounting services that keep your records accurate, your returns filed on time, and your business fully prepared for any HMRC interaction. Our team of registered advisers works with UK businesses across all sectors, from early-stage tech start-ups to established SMEs, providing the strategic tax advisory support you need to stay compliant and tax-efficient. Whether you are facing a compliance check, want to review your current position, or simply need reliable ongoing support, we are here to help. Get in touch with us today to discuss your compliance needs with a specialist.

HMRC compliance means meeting all legal obligations to report, calculate, and pay the correct taxes as a UK business. It covers corporation tax, VAT, PAYE, Self Assessment, and other tax-related duties.

HMRC compliance checks are often triggered by mismatches in returns, third-party information, or unusual filing patterns. They can range from a simple enquiry to a detailed multi-year audit.

HMRC reduces penalties when taxpayers cooperate fully and respond to requests promptly. Voluntary disclosure of errors before HMRC identifies them independently also reduces penalty amounts significantly.

No. From 18 May 2026, tax advisers must be registered to interact with HMRC on behalf of clients. Using an unregistered adviser exposes your business to penalties of up to £10,000.

A monthly reconciliation of your accounts and VAT records is advisable, combined with a quarterly review of all filings and obligations. This reduces errors and ensures you can respond to HMRC requests without disruption.