TL;DR:

- Founder tax efficiency involves legally reducing your tax burden by strategically structuring income, investments, and business activities to maximize wealth retention. It emphasizes proactive planning over reactive decisions, ensuring eligibility for reliefs like BADR, SEIS, and EIS to optimize growth and exit outcomes. Early, straightforward decisions regarding share classes, remuneration, and relief applications are crucial for long-term financial success.

Founder tax efficiency is the legal minimisation of your tax burden through deliberate structuring of income, investments, and business activities to maximise retained wealth. In practice, this means combining tools like SEIS, EIS, Business Asset Disposal Relief (BADR), and pension contributions to reduce what you owe HMRC without reducing what your business earns. For UK tech founders and SME owners, getting this right is the difference between reinvesting capital into growth and handing it over unnecessarily. This guide covers the primary methods, structural choices, exit planning, and the broader financial picture you need to understand in 2026.

Founder tax efficiency is the recognised practice of legally reducing your tax with the same economic outcome, not evading it. The distinction matters because HMRC draws a clear line between avoidance schemes and legitimate planning. Smart planning improves cash flow, builds resilience, and grows net worth without any risk of HMRC action.

For UK tech founders specifically, the stakes are high. Your business may be pre-revenue for years, your personal income is tied to how you extract value from the company, and your eventual exit could be your single largest financial event. Each of these stages carries distinct tax implications, and failing to plan for them in sequence costs real money.

The standard industry term for this discipline is tax planning, but “founder tax efficiency” captures something more specific: the alignment of every financial decision with both your business growth goals and your personal wealth objectives. True tax efficiency operates fully within legal boundaries while ensuring no pound of profit is taxed more than once or at a higher rate than necessary.

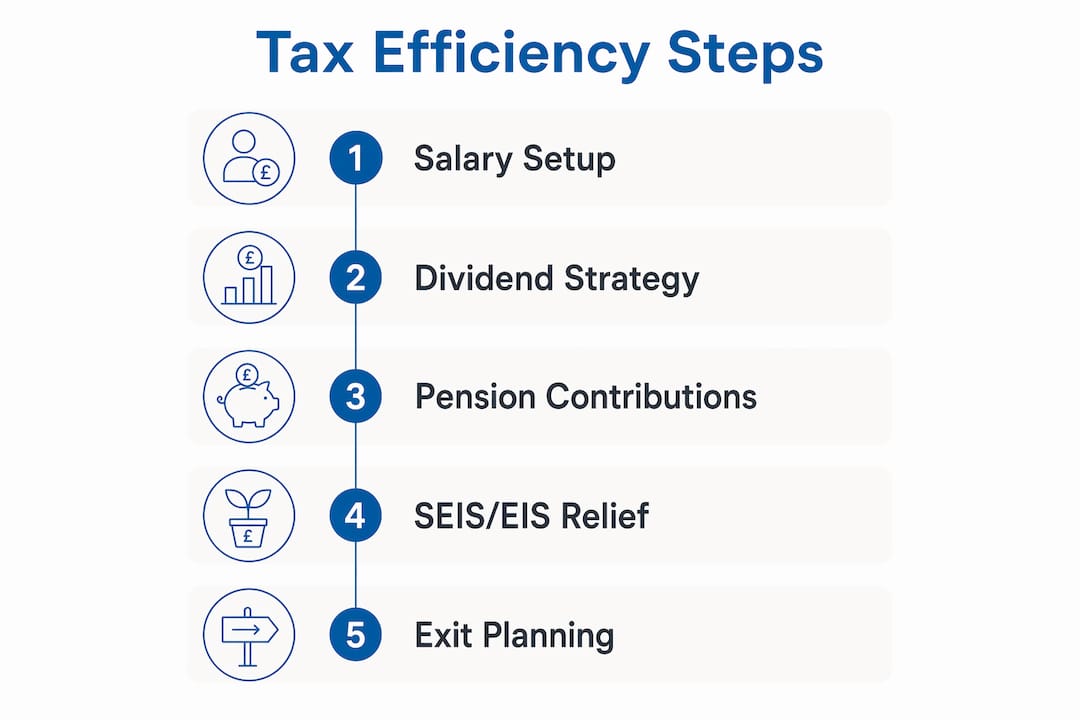

Founder-directors in the UK typically take a low salary set at the personal allowance of £12,570, then extract further income as dividends. This combination saves 25–30 percentage points in tax compared to taking everything as salary. The reason is straightforward: dividends are paid from post-corporation-tax profits and taxed at lower rates than employment income, with no National Insurance Contributions (NICs) on either side.

This is the starting point for most founder tax strategies, but it is not the whole picture. The optimal split between salary and dividends depends on your other income sources, your company’s profitability, and whether you have co-founders or investors with different share classes.

Employer pension contributions of up to £60,000 per year attract corporation tax relief and carry no personal tax charge in the year of contribution. That means contributions reduce your company’s taxable profit at 19–25%, grow free of income tax and capital gains tax inside the pension wrapper, and cost you nothing personally upfront.

Many founders overlook pensions entirely in the early years, treating them as a retirement afterthought. They are actually one of the most tax-efficient extraction routes available, particularly once your dividend allowance is exhausted.

SEIS offers investors 50% income tax relief on investments up to £200,000 per year, alongside CGT deferral and exemption benefits. EIS provides 30% income tax relief on larger investments. These schemes do not just benefit your investors. They make your startup significantly more attractive to early-stage capital by reducing the financial risk for anyone writing a cheque.

Pro Tip: Advance Assurance from HMRC before you raise confirms your company qualifies for SEIS or EIS. Investors will almost always ask for this before committing, so apply early and factor the timeline into your fundraising plan.

BADR reduces the CGT rate on qualifying gains to 14% on the first £1 million of lifetime gains. Using multiple share classes allows founders to allocate dividends and growth differently across shareholders, which can be useful for tax planning when family members or co-founders are involved. Benefits like company medical insurance or electric company cars also provide value at a lower tax cost than equivalent salary.

Limited companies offer the most tax-efficient structure for UK founders compared to sole traders or partnerships. The reasons are structural: corporation tax on profits, lower dividend tax rates, and eligibility for reliefs like BADR and R&D tax credits simply do not apply to unincorporated businesses.

The table below compares the key tax features across the three main structures:

| Feature | Limited Company | Partnership | Sole Trader |

|---|---|---|---|

| Corporation tax on profits | Yes (19–25%) | No | No |

| Dividend extraction option | Yes | No | No |

| Eligible for BADR | Yes (shares) | Limited | No |

| SEIS/EIS compatible | Yes | No | No |

| NICs on profit extraction | Avoidable via dividends | Yes (Class 4) | Yes (Class 4) |

| R&D tax credit access | Yes | No | No |

Partnerships and sole trader structures do have lower administrative costs, but those savings are quickly outweighed by the tax disadvantages once your profits exceed modest levels. For any founder planning to raise external investment, a limited company is not optional. SEIS and EIS both require it.

Scalability is the other factor. A limited company can issue new share classes, grant EMI options to employees, and accommodate institutional investors. A sole trader structure cannot do any of these things without a full restructure, which itself carries tax costs.

Exit planning is where founder tax efficiency pays its largest dividends, and where the most expensive mistakes happen. BADR is the centrepiece of most founder exit strategies, but qualifying for it is not automatic.

To claim BADR, you must meet all of the following criteria at the point of disposal:

The timing of share issuances, dilution events, and restructuring can all affect whether you meet these thresholds. Founders who receive new share classes during a funding round sometimes inadvertently lose their qualifying status without realising it.

From April 2026, the BADR CGT rate rises to 18%, up from 14%. The lifetime allowance remains at £1 million. That increase is not catastrophic, but it does mean the value of early planning is higher than ever. A founder who secures a £1 million qualifying gain before the rate change saves £40,000 compared to one who exits after it.

Pro Tip: If you are approaching a funding round that will dilute your shareholding below 5%, speak to a tax adviser before the round closes. Anti-dilution provisions or share reorganisations may preserve your BADR eligibility without disrupting the deal.

Common pitfalls include holding non-qualifying share types such as preference shares or loan notes rather than ordinary shares, and failing to account for the two-year holding period when planning an accelerated exit. Early decisions about share ownership and investment structure consistently yield the largest long-term tax savings when made proactively rather than reactively.

Tax efficiency for founders does not exist in isolation. It sits inside a broader picture of personal financial goals, lifestyle choices, and long-term wealth building. Getting the tax right while ignoring the rest produces suboptimal outcomes.

Here is a practical framework for integrating the two:

“Optimising for headline tax rates alone can cause founders to sacrifice lifestyle and networking vital to success.” — Capital Founders

The most effective founder tax strategies are those built around the founder’s specific context. Your sector, your funding stage, your co-founder arrangements, and your personal income needs all shape which tools apply and in what order. Working with an adviser who understands the UK tech ecosystem, rather than a generalist, makes a measurable difference to the outcomes you achieve. You can explore tax planning for startups to understand why timing and structure decisions made early have compounding effects throughout your company’s life.

Founder tax efficiency is the deliberate, legal structuring of income, investments, and business activities to minimise tax and maximise retained wealth across every stage of a company’s life.

| Point | Details |

|---|---|

| Salary plus dividends | Taking a low salary at £12,570 and extracting further income as dividends saves 25–30 percentage points versus salary only. |

| Pension contributions | Employer contributions up to £60,000 per year attract corporation tax relief with no personal tax charge upfront. |

| SEIS and EIS schemes | SEIS gives investors 50% income tax relief, making your startup more attractive to early-stage capital. |

| Limited company structure | Only limited companies access BADR, SEIS, EIS, and R&D tax credits, making incorporation the default for growth-focused founders. |

| Exit planning timing | BADR’s CGT rate rises to 18% from April 2026, so early share structuring and two-year holding periods are critical to qualify. |

I have worked with founders across pre-seed through to Series A exits, and the pattern I see most often is this: tax planning happens reactively. A founder raises a round, restructures their shares, and only then asks whether they still qualify for BADR. Or they take a full salary for three years because it felt simpler, then realise they have paid tens of thousands more in NICs than necessary.

The uncomfortable truth is that the most valuable tax decisions are made before the money arrives, not after. Choosing the right share class structure before your first investor comes in, setting up your pension contribution policy in year one, and applying for SEIS Advance Assurance before you open your fundraising round: these are the decisions that compound. They are also the ones that feel premature when you are focused on product and growth.

I also see founders conflate tax efficiency with complexity. The salary-plus-dividends approach is not complex. A pension contribution is not complex. What makes them powerful is consistency and timing, not sophistication. The founders who retain the most wealth are not the ones with the most elaborate structures. They are the ones who made straightforward decisions early and stuck to them.

One area I would flag specifically for 2026: the BADR rate change is real, and the window to lock in gains at 14% is closing. If you are considering a partial exit, a secondary sale, or a management buyout of any kind, get advice now rather than after the April deadline has passed.

— Rahamut

Priceandaccountants works exclusively with UK tech founders, SMEs, and international businesses establishing a UK presence. Our strategic tax advisory service covers the full founder journey: from structuring your initial share classes and applying for SEIS Advance Assurance, through to exit planning and BADR qualification reviews.

We have supported over 20 startups through their early-stage processes, several of which are now valued at over £50 million. Our team understands the specific reliefs, thresholds, and timing decisions that matter to founders in the UK tech ecosystem. Whether you need a one-off review of your remuneration structure or ongoing outsourced FD support, we provide the depth of advice that generalist accountants typically cannot. Speak to us before your next funding round or financial year-end to make sure your tax position is working as hard as your business is.

Founder tax efficiency is the legal practice of structuring your salary, dividends, investments, and business activities to pay the minimum tax required by law. It covers remuneration, funding schemes, and exit planning across the full life of your company.

SEIS offers investors 50% income tax relief on investments up to £200,000 per year and is designed for very early-stage companies. EIS offers 30% relief on larger investments and suits companies at a slightly later stage of growth.

Taking a low salary at the personal allowance combined with dividends saves 25–30 percentage points compared to salary only in most cases. The optimal split depends on your total income, company profitability, and whether you have other income sources.

You must hold at least 5% of ordinary share capital and voting rights, have been an employee or officer for at least two years, and meet all conditions continuously for two years ending on the disposal date. The CGT rate under BADR rises to 18% from April 2026.

Year-round proactive planning consistently outperforms reactive year-end decisions. The most impactful choices, including share structure, remuneration method, and pension setup, should be made at company formation or before your first funding round.