TL;DR:

- Deferred tax records future tax obligations or benefits due to temporary differences between financial accounts and tax laws. It arises from timing mismatches and includes deferred tax assets and liabilities, which are measured using enacted tax rates at the time of reversal.

Deferred tax is the accounting recognition of future tax obligations or benefits that arise from temporary differences between financial accounting rules under GAAP or IFRS and the tax regulations applied by HMRC. These differences do not create permanent gaps. They reverse over time, meaning a business will eventually pay more or less tax than its current accounts suggest. Understanding deferred tax is not optional for finance professionals. It sits at the heart of accurate financial reporting, tax planning, and stakeholder communication.

Deferred tax arises from timing mismatches between what accountants recognise as profit and what tax authorities assess as taxable income. The two figures rarely match in any given period. Accounting standards require income and expenses to be recognised when they are earned or incurred. Tax law often follows different rules, particularly around depreciation, provisions, and revenue timing.

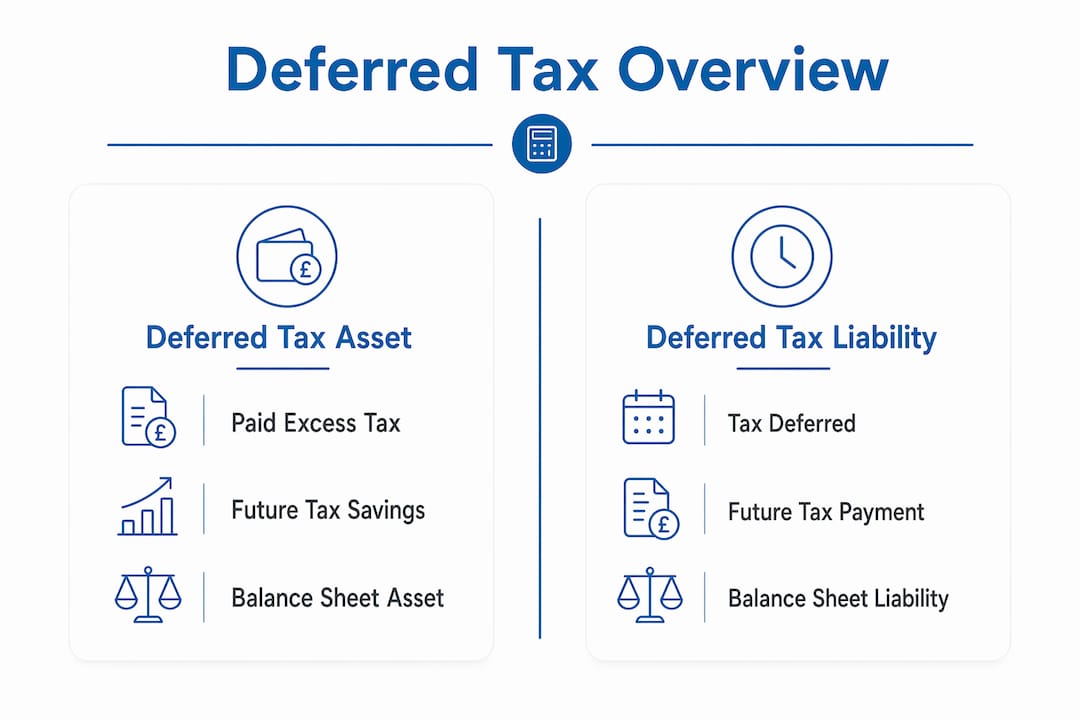

The result is a gap. When your accounting profit exceeds your taxable profit, you pay less tax now but will pay more later. That future obligation is a deferred tax liability (DTL). When your taxable profit exceeds your accounting profit, you pay more tax now and will recover that excess later. That future benefit is a deferred tax asset (DTA).

Both DTAs and DTLs appear on the balance sheet as non-current items. They are not cash movements today. They represent the tax consequences of decisions already made, recognised in advance so that financial statements give an accurate picture of a company’s true tax position.

The most common cause of deferred tax is depreciation. Tax law in the UK often permits accelerated capital allowances, letting businesses deduct the cost of an asset faster than accounting standards allow. A company might write off a piece of machinery over three years for tax purposes but over five years in its accounts. That gap creates a taxable temporary difference and a corresponding DTL.

Other frequent triggers include:

The critical distinction is between temporary and permanent differences. Temporary differences reverse. Permanent differences, such as government fines or tax-exempt interest income, do not reverse and therefore create no deferred tax balance. Confusing the two is one of the most common errors in tax provision work.

Pro Tip: When reviewing your tax provision, list every difference between your accounting profit and taxable profit and classify each one explicitly as temporary or permanent. Any item you cannot classify confidently warrants specialist review.

The calculation is straightforward in principle. Deferred tax equals the temporary difference multiplied by the enacted tax rate expected to apply when the difference reverses. In the UK, that means using the corporation tax rate confirmed by legislation at the balance sheet date, not the rate currently in effect if a change has been announced but not yet enacted.

For example: a company has an asset with a carrying value of £100,000 in its accounts and a tax base of £60,000. The temporary difference is £40,000. At a corporation tax rate of 25%, the DTL is £10,000.

The presentation in financial statements follows a clear structure:

| Item | Deferred tax asset (DTA) | Deferred tax liability (DTL) |

|---|---|---|

| Arises when | Tax paid exceeds accounting tax expense | Accounting tax expense exceeds tax paid |

| Balance sheet position | Non-current asset | Non-current liability |

| Future implication | Future tax saving | Future tax payment |

| Common cause | Warranty provisions, pension liabilities | Accelerated depreciation, revenue timing |

| Measurement basis | Enacted tax rate at reversal date | Enacted tax rate at reversal date |

Deferred tax also flows through the income statement. The movement in DTAs and DTLs between periods forms part of the total income tax charge, alongside current tax. This means your reported profit after tax reflects not just what you owe HMRC this year, but the tax consequences of all timing differences accumulated to date.

Pro Tip: Always use the enacted rate, not the proposed rate. If a budget announcement changes the corporation tax rate but the legislation has not passed, you cannot use the new rate in your deferred tax calculation.

Deferred tax provides insight into earnings quality and future cash obligations that current tax figures alone cannot reveal. A business reporting strong profits but carrying large DTLs is signalling that significant tax payments lie ahead. Investors and lenders read deferred tax balances as a forward indicator of cash pressure.

For business owners, the practical implications are significant:

Deferred tax is also a non-cash item. It reconciles net income to actual cash tax paid and should not be confused with a tax payment due immediately. That distinction matters when you are explaining your accounts to a board, an investor, or a lender.

Deferred tax accounting produces more errors than almost any other area of financial reporting. The consequences range from restated accounts to regulatory scrutiny. The most frequent mistakes follow a predictable pattern.

Misclassifying permanent differences as temporary. This error creates deferred tax balances that should not exist and overstates or understates the tax charge. Every difference must be tested for reversibility before a deferred tax balance is recognised.

Failing to remeasure after tax law changes. Remeasurement must occur in the reporting period when new legislation is enacted, regardless of when it takes effect. Businesses that delay remeasurement until the new rate applies are misstating their accounts.

Recognising DTAs without assessing recoverability. A DTA is only an asset if the business will generate enough taxable profit to use it. Recognising a DTA on losses carried forward without a credible profit forecast is an overstatement.

Using a single tax rate across multiple jurisdictions. A UK group with subsidiaries in Ireland, Germany, and the US faces three different tax rates and three different sets of rules. Applying the UK rate to all entities produces materially wrong figures.

Ignoring the impact on deferred tax journal entries. Each period, the movement in deferred tax must be journalled correctly: debit or credit the balance sheet balance, with the corresponding entry to the income statement tax charge or, in some cases, directly to equity.

Pro Tip: Build a deferred tax schedule that tracks each temporary difference individually, including its origination date, expected reversal period, and the tax rate applied. This makes remeasurement after a rate change a mechanical exercise rather than a crisis.

Deferred tax is a non-cash balance sheet item that reflects future tax obligations or savings from timing differences, measured using enacted tax rates and requiring active management to remain accurate.

| Point | Details |

|---|---|

| Core definition | Deferred tax arises from timing differences between accounting profit and taxable income under GAAP or IFRS. |

| Calculation method | Multiply the temporary difference by the enacted tax rate expected at the reversal date. |

| DTA vs DTL | DTAs signal future tax savings; DTLs signal future tax payments, both classified as non-current. |

| Recoverability test | DTAs must only be recognised when future taxable profit is probable; apply a valuation allowance otherwise. |

| Remeasurement obligation | Remeasure all deferred tax balances immediately when new tax legislation is enacted. |

Rahamut here. After years of working with tech start-ups and growing SMEs at Priceandaccountants, the pattern I see most often is this: deferred tax gets treated as a compliance checkbox rather than a planning tool. That is a missed opportunity.

The businesses that manage deferred tax well use it to anticipate cash. When a client is considering a large capital investment, the accelerated tax relief creates a DTL today but reduces the cash tax bill in the near term. Modelling that correctly changes the investment decision. It is not abstract accounting. It is real money at a specific point in time.

The other thing I have noticed is that tax law changes catch businesses off guard. When the UK corporation tax rate moved to 25%, every deferred tax balance in every set of accounts needed remeasuring. Businesses that had not maintained clean deferred tax schedules spent weeks reconstructing figures they should have had at their fingertips. Staying current with jurisdiction-specific tax law is not optional. It is the difference between a clean audit and an uncomfortable one.

My honest advice: treat your deferred tax schedule as a live document, not an annual exercise. Review it every time your business makes a significant asset purchase, changes its revenue model, or operates in a new country. The accounting policies you adopt at the start of a period shape your deferred tax position for years.

— Rahamut

Deferred tax is one of the areas where specialist advice pays for itself quickly.

At Priceandaccountants, we work with tech start-ups, growing SMEs, and international founders who need their deferred tax positions calculated correctly and managed proactively. Our tax advisory services cover the full scope of deferred tax work: identifying temporary differences, applying the correct enacted rates, assessing DTA recoverability, and remeasuring balances after legislative changes. We also help clients understand what their deferred taxation balances mean for cash flow, valuation, and investor reporting. If your accounts include deferred tax balances you are not fully confident in, speak to our team.

Deferred tax is the future tax impact of timing differences between accounting profit and taxable income. It appears on the balance sheet as either an asset (future tax saving) or a liability (future tax payment).

A deferred tax asset arises when you pay more tax now than your accounts require, giving you a future saving. A deferred tax liability arises when you pay less tax now and will owe more later.

Deferred tax appears on the balance sheet as a non-current asset or liability and flows through the income statement as part of the total tax charge. It is a non-cash item that reconciles accounting profit to actual tax paid.

No. Permanent differences, such as non-deductible fines or tax-exempt income, do not reverse and therefore create no deferred tax balance. Only temporary differences that will reverse in future periods give rise to DTAs or DTLs.

Deferred tax balances must be remeasured in the reporting period when new tax legislation is enacted, regardless of when the new rate takes effect. Delaying remeasurement until the rate applies produces misstated accounts.