TL;DR:

- VAT registration in the UK becomes mandatory once a business’s taxable turnover exceeds £90,000 in a rolling 12-month period. Businesses must register within 30 days of exceeding this threshold, using online applications via HMRC’s Government Gateway and MTD-compatible software. Early registration is advised to avoid penalties and complications related to effective registration dates and ongoing compliance.

VAT registration is the formal process by which a UK business notifies HMRC that it is liable to charge, collect, and remit Value Added Tax. The vat registration process UK becomes mandatory once your taxable turnover exceeds £90,000 in any rolling 12-month period. Miss the deadline and HMRC will penalise you from the date you should have registered, not the date you actually did. This guide covers every stage: eligibility triggers, required documents, the online application via HMRC’s Government Gateway, Making Tax Digital compliance, and the mistakes that cost businesses money.

The mandatory VAT threshold is £90,000 in taxable turnover during any rolling 12-month period, as of 2026. That figure is not your profit or your total income. It is the value of VAT-taxable goods and services you supply, before any deductions.

Two distinct triggers require registration. The first is the historical test: your taxable turnover has already exceeded £90,000 over the past 12 months. The second is the forward-looking test: you expect turnover to exceed £90,000 in the next 30 days alone. The second trigger demands immediate registration, not a 30-day wait.

Once you cross the historical threshold, you must register within 30 days of the end of the month in which you exceeded it. For example, if your rolling turnover passes £90,000 on 18 march, you have until 30 april to notify HMRC, and your effective registration date becomes 1 may.

Voluntary registration is also available to businesses below the threshold. Voluntary registration lets you reclaim VAT on purchases and can signal credibility to larger clients who are themselves VAT-registered. The trade-off is the additional compliance burden of filing quarterly returns.

Key eligibility scenarios at a glance:

Preparation prevents delays. Gather every document before you open the Government Gateway, because an incomplete application can stall your registration by weeks.

Required documents include your Unique Taxpayer Reference (UTR), National Insurance number, and Companies House registration number if your business is incorporated. Sole traders and partners must also provide personal identification such as a valid passport or driving licence. You will need your business bank account details and a contact address for correspondence.

Your Government Gateway account is the gateway to the entire application. If you do not already have one, create it at GOV.UK before you start. You will need a valid email address and a mobile number for two-step verification. HMRC ties your VAT registration to this account permanently, so use a business email rather than a personal one.

Documents checklist:

Pro Tip: Set up your Government Gateway account at least 48 hours before you intend to submit. Verification emails and SMS codes can take time, and a delayed account setup is the most common reason applications stall on day one.

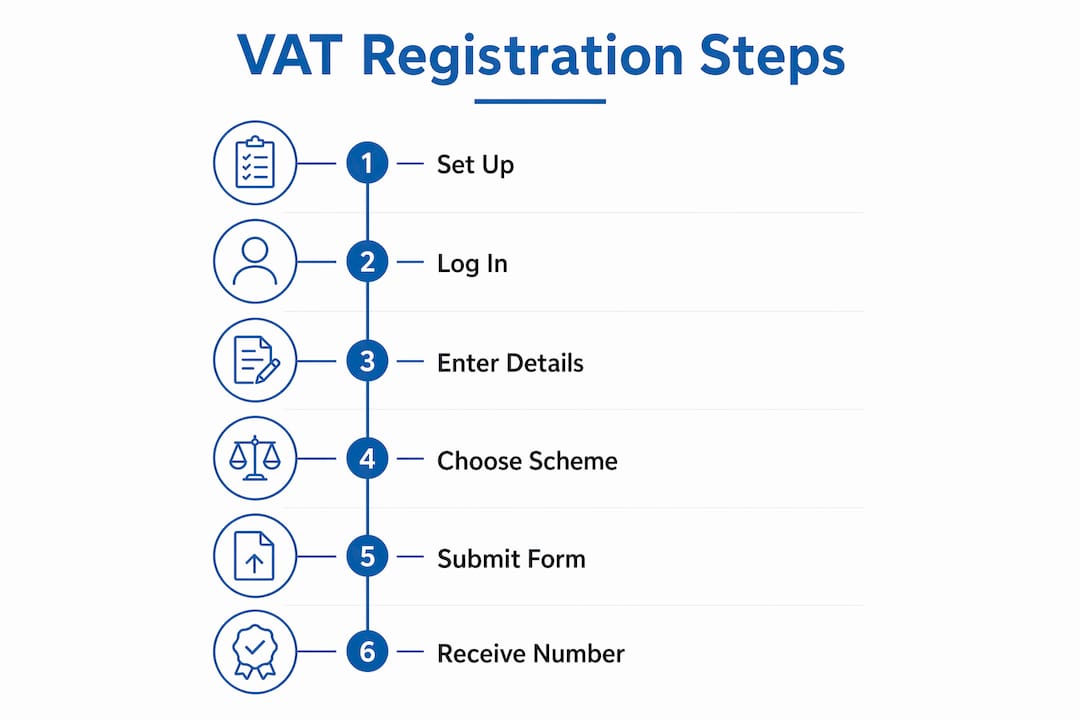

The VAT registration application is completed entirely online through GOV.UK. HMRC no longer accepts paper VAT1 forms as the primary route for most businesses.

Step 1: Log into your Government Gateway account Go to GOV.UK and sign in with your Government Gateway user ID and password. If you are creating a new account, select “Create sign in details” and follow the verification steps.

Step 2: Navigate to the VAT registration section Once logged in, select “Get access to a tax, duty or scheme” from your business tax account dashboard. Choose “VAT” from the list of taxes.

Step 3: Enter your business details You will be asked for your legal business name, trading name (if different), business address, nature of trade, and the date your turnover exceeded the threshold. Enter these accurately. HMRC cross-references your UTR and Companies House data automatically.

Step 4: Choose your VAT accounting scheme HMRC offers several schemes. The Standard VAT Accounting scheme suits most businesses. The Flat Rate Scheme simplifies calculations for businesses with turnover below £150,000. The Cash Accounting Scheme lets you account for VAT based on payments received rather than invoices issued, which helps cash flow. Choose the scheme that fits your business model before submitting.

Step 5: Submit the online VAT1 form Review every field before you submit. Errors in your effective date of registration or business classification can create problems with your first return. Once submitted, HMRC sends a confirmation reference number.

Step 6: Await your VAT number and certificate Your VAT certificate arrives by post within approximately 10–30 days. It confirms your VAT registration number, your effective date of registration, and your first return deadline. Retain this certificate permanently as part of your business records.

| Stage | Action | Typical Timeframe |

|---|---|---|

| Government Gateway setup | Create or log into account | Same day |

| Application submission | Complete online VAT1 form | 30–60 minutes |

| HMRC processing | Application reviewed | 3–5 working days |

| VAT number issued | Number available online | 3–10 working days |

| Certificate by post | Formal confirmation received | 10–30 days |

Pro Tip: Your VAT number is often available in your Government Gateway account before the paper certificate arrives. You can begin trading with it immediately once it appears online, without waiting for the post.

Missing the 30-day registration deadline is the single most costly error. Late registration incurs a penalty starting at a 3% surcharge on the VAT you owe from the date you should have registered. That surcharge increases if the delay remains unresolved. HMRC calculates the penalty on the full amount of VAT due from your effective registration date, not from when you eventually applied.

The effective date of registration trips up many business owners. This date is usually the first day of the second month after you exceeded the threshold. It determines when you must start charging VAT on your invoices and when your first return period begins. Charging VAT before this date or failing to charge it after this date both create compliance problems.

Inaccurate form submissions are another frequent issue. A wrong business classification or an incorrect threshold date can delay processing and require HMRC correspondence to correct. Double-check every field against your actual financial records before you submit.

Many business owners also underestimate the ongoing compliance requirements. After registration, you must keep digital VAT records and submit returns through Making Tax Digital-compatible software. HMRC no longer accepts manual submissions. Software such as Xero, QuickBooks, or Sage all meet the MTD requirement and connect directly to HMRC’s systems.

Pro Tip: Track your rolling 12-month taxable turnover every month, not just at your financial year end. A simple spreadsheet updated monthly catches threshold breaches before they become a compliance problem. Better still, use MTD-compatible accounting software that flags the threshold automatically.

Voluntary registration confusion is also common. Some business owners register voluntarily, then discover the quarterly filing obligation is more burdensome than expected. Before you register voluntarily, calculate whether the VAT you reclaim on purchases genuinely outweighs the administrative cost. For a tax compliance workflow that accounts for this, plan your VAT position before you commit.

The VAT registration process in the UK is mandatory at £90,000 taxable turnover, must be completed online via HMRC’s Government Gateway, and requires MTD-compatible software for all ongoing returns.

| Point | Details |

|---|---|

| Mandatory threshold | Register once taxable turnover exceeds £90,000 in any rolling 12-month period. |

| Registration deadline | Submit your application within 30 days of the month end in which you exceeded the threshold. |

| Documents required | Have your UTR, National Insurance number, Companies House number, and bank details ready before you start. |

| Effective date matters | Your effective registration date determines when you must charge VAT and when your first return is due. |

| MTD compliance | All VAT returns must be submitted through Making Tax Digital-compatible software after registration. |

Most business owners treat the £90,000 threshold as a finish line. They watch their turnover approach it and plan to register at the last possible moment. That approach is the wrong way to think about it.

The 30-day window sounds generous until you factor in document gathering, Government Gateway setup, and the time HMRC takes to process the application. I have seen businesses submit on day 28 and still receive their VAT number after the deadline because their Government Gateway account had a verification issue. HMRC does not accept “the system was slow” as a reasonable excuse for late registration.

The more important point is the effective date. Businesses often assume registration takes effect from the day they apply. It does not. Your effective date is typically the first day of the second month after you exceeded the threshold. That means you may owe VAT on invoices you have already issued, before you even knew you were registered. Reclaiming that VAT from clients retrospectively is awkward and sometimes impossible.

My advice is to start monitoring your rolling 12-month turnover from the moment it passes £70,000. That gives you a genuine buffer. Use Xero or QuickBooks to set a threshold alert. When you hit £85,000, begin gathering your documents and setting up your Government Gateway account. By the time you cross £90,000, you are ready to submit within days, not scrambling to meet a deadline.

The online process itself is genuinely straightforward once you have everything prepared. The VAT1 form takes under an hour to complete. The complexity is not in the form. It is in the preparation, the scheme selection, and understanding what your effective date means for your existing invoices.

— Rahamut

VAT registration is one step. Staying compliant across every quarterly return, every scheme change, and every MTD update is the ongoing work that catches businesses out.

Priceandaccountants handles the full VAT registration application for UK businesses, from document preparation through to scheme selection and submission. The team also manages bookkeeping and VAT records to keep you MTD-compliant from day one. For start-ups and growing businesses, understanding your accounting period and how it aligns with your VAT return deadlines is critical to avoiding penalties. Whether you are registering for the first time or reviewing your current VAT position, Priceandaccountants provides the practical support to get it right. Get in touch to discuss your VAT compliance needs.

The VAT registration threshold is £90,000 in taxable turnover during any rolling 12-month period. Businesses must register within 30 days of the end of the month in which they exceeded this figure.

HMRC typically issues a VAT number within 3–10 working days of a completed application. The formal VAT certificate arrives by post within 10–30 days, though your number is usually visible in your Government Gateway account sooner.

Yes. Voluntary registration is permitted for any business below £90,000 in taxable turnover. It allows you to reclaim VAT on business purchases but requires quarterly return submissions through MTD-compatible software.

Late registration triggers a penalty starting at a 3% surcharge on the VAT owed from your effective registration date. The surcharge increases the longer the delay remains unresolved, and HMRC calculates it on the full amount due from when you should have registered.

Yes. All VAT-registered businesses must keep digital records and submit returns through MTD-compatible software. HMRC no longer accepts manual VAT submissions. Xero, QuickBooks, and Sage all meet the MTD requirement.