TL;DR:

- Effective business scaling requires aligning cash flow management, funding strategies, and operational maturity to ensure reliable growth. Regular forecasting, automation, and disciplined financial practices help UK SMEs avoid fragility and make informed funding decisions. Monitoring key metrics like cash runway and free cash flow supports sustainable expansion and long-term resilience.

Scaling a business is one of the most exciting things you can do as a founder. But knowing how to scale business finances effectively is where most UK SMEs quietly come unstuck. Revenue goes up, the team grows, customers multiply — and then the bank account tells a very different story. The mistake is treating revenue growth and financial health as the same thing. They are not. This guide cuts through the noise to give you practical, proven strategies for financial growth that keep your cash cycle, funding decisions, and financial processes working together rather than pulling apart.

| Point | Details |

|---|---|

| Growth is not the same as scaling | True financial scaling means growing reliably without creating fragility in your cash position or operations. |

| Cashflow forecasting is non-negotiable | A rolling 13-week forecast lets you spot funding gaps before they become crises and supports better funding conversations. |

| Align funding to your cash cycle | Match the type and timing of funding to your actual working capital needs, not just your ambition or revenue projections. |

| Automate to control overhead | Automating invoicing, reporting, and payment processing reduces errors and frees up time for strategic decisions. |

| Measure what matters | Track cash runway, operating cash flow ratio, and free cash flow regularly to maintain genuine financial control. |

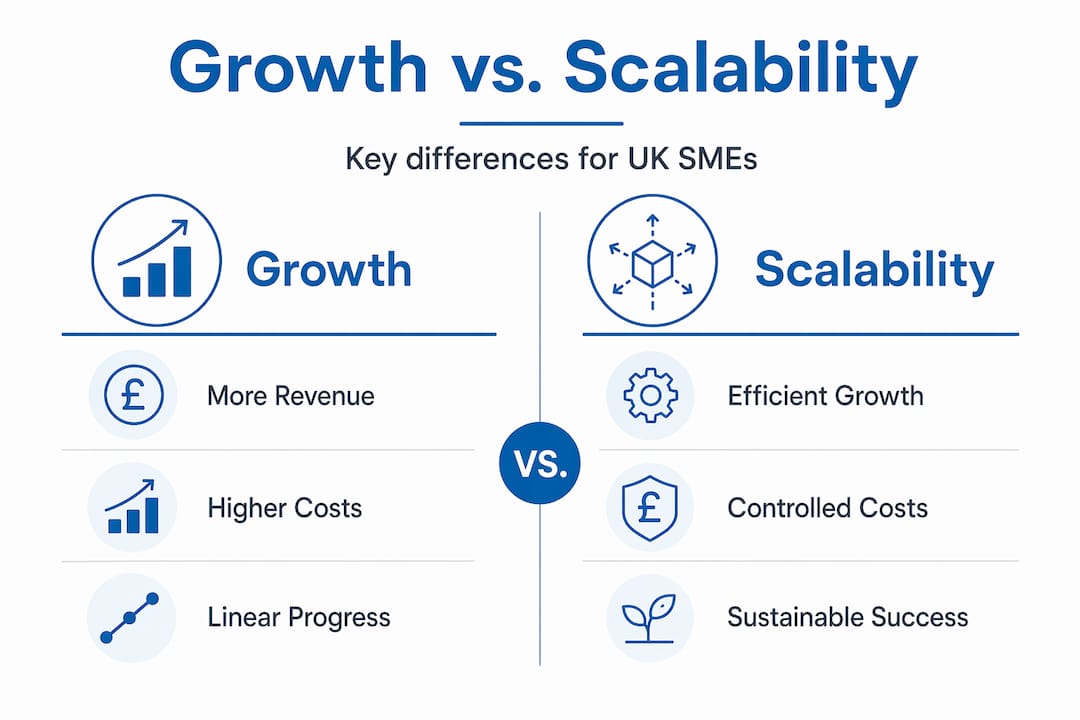

Before you can build a plan, you need to understand what you are actually trying to achieve. Most founders want growth. Fewer founders achieve genuine financial scalability. The difference matters enormously.

Growth means your revenue is increasing. Scalability means your business can grow reliably and efficiently with operational maturity, improving margins, and a cash cycle that supports rather than undermines expansion. A business that doubles its turnover but sees its overdraft triple and its supplier relationships strain is not scaling. It is accelerating towards a structural problem.

The current UK economic environment has made this distinction sharper. With borrowing costs still elevated and customers taking longer to pay, the businesses winning on financial resilience are those prioritising disciplined, controlled growth over speed. Margin resilience matters. Cash cycle alignment matters. The ability to absorb a slow month without a crisis matters.

Several risks emerge when growth outpaces your financial infrastructure:

Pro Tip: Before you pursue your next growth initiative, map your current cash conversion cycle. How long does it take from spending money to receiving money? That single number will tell you more about your scaling readiness than any revenue projection.

Improving business cash flow is not about chasing invoices harder. It is about building genuine visibility into where your money is, where it is going, and when the gaps will appear. That visibility starts with understanding your cash dependencies: your supplier payment terms, your stock cycles if you hold inventory, and your customer payment behaviour.

The most practical forecasting tool for scaling businesses is the rolling 13-week cashflow forecast. This approach helps businesses adjust plans ahead of time to maintain liquidity, rather than reacting to a shortfall after it has already arrived. You update it weekly, rolling it forward, so you always have a clear 90-day picture of your cash position.

Within that forecast, you need at least three scenarios:

| Scenario | Description | Purpose |

|---|---|---|

| Base case | Your most realistic expectation of income and outgoings | Day-to-day decision-making and planning |

| Downside | Revenue falls 20-30%, payment delays increase | Tests resilience and highlights minimum cash needs |

| Rapid growth | Revenue accelerates, requiring more working capital | Identifies funding needs before growth creates a gap |

The downside scenario is the one most founders skip. Do not skip it. Your lender or investor will stress-test your numbers. You should do it first.

Accurate forecasting also directly supports better funding conversations. Strong businesses fail funding conversations not because of weak revenue, but because they cannot clearly articulate their day-to-day cash needs or explain the timing of their funding ask. A well-constructed forecast solves that problem before you walk into any meeting.

Pro Tip: Link your cashflow forecast directly to your sales pipeline and payment terms. If a large customer pays on 60-day terms, that invoice landing on day one should trigger a visible dip in your forecast 60 days out. Seeing it in advance changes how you manage it.

Once your cashflow visibility is in place, the next step is making sure your financial operations do not create drag as you grow. Automated invoicing and reporting provide real-time data, reduce errors, and cut administrative overhead. For a scaling SME, that is not just a convenience. It is a structural advantage.

Here is where to focus your automation efforts:

On overhead: tips for scaling finances always include controlling your cost base, but few people give you a concrete benchmark. Keep your overhead as a percentage of revenue below the level at which a 20% revenue drop would put you in the red. That sounds obvious. Very few founders actually calculate it.

Effective receivables and payables management also includes negotiating payment terms proactively. If your standard customer terms are 30 days and your standard supplier terms are also 30 days, your working capital buffer is zero. Extending supplier terms to 45 or 60 days while tightening customer terms to 21 days creates a meaningful improvement without any additional funding.

One of the best practices for financial scaling is understanding that not all funding is the same, and timing matters as much as amount. Using a long-term loan to solve a short-term cash gap is expensive and inefficient. Using a short-term facility to fund long-term equipment creates monthly pressure that squeezes your operating cash.

| Funding type | Best used for | Key consideration |

|---|---|---|

| Working capital facility | Bridging gaps between payment and receipt | Should match your receivables cycle length |

| Equipment or asset finance | Purchasing capital items that generate income | Term should align with asset’s useful life |

| Bridging finance | Short-term gap before a known cash event | High cost; use only when timing is certain |

| Equity investment | Long-term growth capital and team expansion | Dilutes ownership; best for non-debt growth phases |

Matching your funding ask to your cash cycle rather than your ambition is critical. A business with a 45-day cash conversion cycle asking for a 12-month term loan to solve a 45-day problem is paying for money it does not need for most of that period.

Digital-first funding journeys and proactive cashflow guidance consistently produce better outcomes for SMEs than capital alone. Lenders and investors respond to founders who can clearly explain what they need the money for, when they need it, and how they will repay it. That credibility comes from the forecasting and financial process work you have already done. Good tax planning strategies also play a role here, as understanding your tax position affects both your funding ask and your net cash position.

Getting the systems and funding in place is one part of how to manage business budgets for scale. Keeping them working well as you grow is the other part. That requires regular measurement and honest benchmarking.

The three metrics that matter most for scaling SMEs are:

Maintaining cash reserves covering three to six months of operating expenses provides the buffer that keeps unexpected events from becoming existential threats. Building that reserve should be a deliberate target in your budget, not something that happens when revenue is good.

Diversifying your revenue streams adds a second layer of resilience. A business that gets 70% of its revenue from two customers is financially fragile no matter how strong those relationships feel today. Scenario stress-testing your expansion decisions, particularly before signing significant overhead commitments, will reveal that fragility before it costs you.

A fractional CFO or strategic adviser helps unify fragmented financial data, stabilise cashflow, and translate the numbers into growth decisions. At the stage where your finances are genuinely complex, that kind of support pays for itself.

I have worked with founders at every stage, from pre-revenue to Series A, and the pattern I see most often is this: the businesses that struggle are not the ones that grew too slowly. They are the ones that treated revenue as a proxy for financial health and discovered the difference at the worst possible moment.

What I have learned is that profitability and tax strategy matter far more than top-line volume when you are building something that lasts. A founder who knows their margins, their cash runway, and their tax position is infinitely better placed than one who knows only their monthly revenue figure.

The most underrated shift I see in well-run scaling businesses is the move from reactive to proactive financial management. They stop checking bank balances and start reading forecasts. They stop reacting to tax bills and start planning for them with proper HMRC compliance in place from the outset. Digital tools make that transition faster, but the tools only work when there is financial discipline behind them.

My honest take: the founders who scale well are not the ones with the most ambition. They are the ones who respect the numbers and build the systems to stay ahead of them.

— Rahamut

Scaling your finances is easier when you are not doing it alone. At Priceandaccountants, we work with UK tech founders and SME owners every day to build the financial infrastructure that makes reliable growth possible, from cashflow forecasting and bookkeeping services that keep your records accurate in real time, to strategic tax planning that protects your cash position as you grow.

Our advisory and tax planning service acts as your outsourced finance director, giving you the strategic clarity to make confident funding decisions without the overhead of a full-time hire. Whether you need support building your first cashflow model, preparing for an investor conversation, or making sense of your accounts, we bring the expertise that growing businesses need at the exact moment they need it. Talk to us about where your finances are today and where they need to be.

Scaling your finances means building financial processes, cashflow visibility, and funding structures that support reliable growth without creating fragility. It goes well beyond increasing revenue to include margin resilience and operational maturity.

Begin by mapping your cash conversion cycle and identifying your largest payment timing gaps. Tightening customer payment terms and scheduling supplier payments strategically can improve cashflow within weeks without any additional funding.

The three most critical metrics are cash runway, operating cash flow ratio, and free cash flow. These tell you whether your operations are genuinely self-sustaining rather than dependent on constant external funding.

Match the type and term of funding to the specific cash cycle it is solving. Working capital facilities suit short-term receivables gaps, while asset finance suits capital purchases. Mismatching funding type to need is one of the most common and costly mistakes SMEs make.

When your financial data becomes fragmented across multiple systems, your tax position is affecting growth decisions, or you are preparing for a funding round, bringing in strategic financial expertise becomes a genuine necessity rather than a luxury.