TL;DR:

- Setting up a global business involves choosing the right jurisdiction, legal structure, and banking options before forming an entity.

- Operational readiness and thorough document preparation are crucial, as delays in banking and licenses can hinder activation.

Global business setup is the process of legally establishing and operating a company across international borders by navigating jurisdictional, operational, and compliance requirements. Getting it right means choosing the correct entity structure, satisfying local regulatory bodies, and activating banking before you trade. This global business setup guide covers every critical decision point: jurisdiction selection, incorporation steps, tax obligations, and the operational realities that trip up even experienced founders. Frameworks such as OECD BEPS now shape which structures are viable, and banking readiness determines whether your entity can actually function from day one.

Clarity on your business objectives is the first prerequisite for any international business setup. Are you entering a new market to sell, to hire talent, or to hold intellectual property? Each goal points to a different jurisdiction and entity type, so defining this before you file a single document saves months of costly restructuring.

Operational readiness matters as much as legal readiness. Your product must have demonstrated demand before you commit to a foreign entity. A common and practical approach is to test markets first using independent contractors or an Employer of Record (EOR) service. An EOR employs staff on your behalf in a target country, letting you validate the market without triggering a tax nexus or VAT registration obligation.

Document preparation is where most founders lose time. A cross-border business setup typically requires notarised identity documents, apostille certifications, Ultimate Beneficial Owner (UBO) disclosures, and certified translations. Document mismatches in UBO filings alone can add multiple weeks to your formation timeline. Prepare a complete document pack before you approach any registry.

Key prerequisites to address before filing:

Pro Tip: Engage a local notary or formation agent in your target jurisdiction at least four weeks before your intended filing date. Certification chains take longer than most founders expect.

Jurisdiction selection is the single most consequential decision in any foreign company establishment. Tax rate is only one factor. Payment processor compatibility, banking availability, and substance requirements all determine whether your entity can operate in practice.

The OECD BEPS framework and EU anti-tax-avoidance directives require genuine economic activity in the jurisdiction you choose. A letterbox company in a zero-tax territory is no longer a viable structure for most businesses. You need real substance: a local director, a registered office with activity, and demonstrable economic presence.

Payment processor support is a practical filter that founders routinely overlook. Stripe, for example, supports businesses registered in the UK, Ireland, Singapore, and the UAE, but excludes many low-tax offshore centres such as the Cayman Islands, BVI, and Seychelles. If your revenue model depends on Stripe or similar processors, your jurisdiction shortlist shrinks immediately.

| Jurisdiction | Entity type | Formation speed | Stripe support | Substance requirement |

|---|---|---|---|---|

| United Kingdom | Ltd | 24 hours | Yes | Moderate |

| Singapore | Pte Ltd | 1–3 days | Yes | Moderate |

| UAE (Free Zone) | Free Zone LLC | 5–7 days | Yes | Low to moderate |

| Ireland | Ltd | 3–5 days | Yes | Moderate |

| Cayman Islands | IBC | 3–5 days | No | Low |

Banking availability is the other critical filter. Many banks in the UAE and Singapore require in-person KYC visits, which adds time and travel cost to your plan. Confirm that a bank you can realistically open with operates in your chosen jurisdiction before you incorporate.

Pro Tip: Check payment processor and bank onboarding feasibility before you incorporate. Restructuring after the fact costs far more than getting the jurisdiction right the first time.

Incorporation and activation are two separate milestones. Founders frequently celebrate incorporation and then discover that banking, licences, and operational approvals take far longer. Plan for both from the outset.

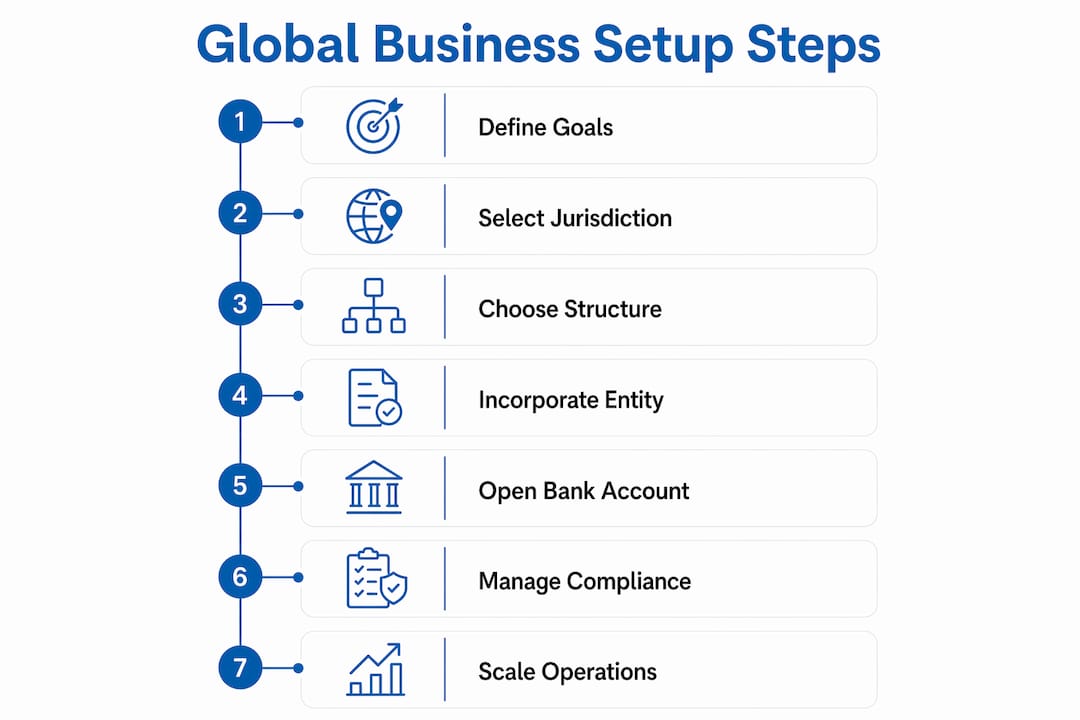

The sequential steps for overseas business registration are:

The gap between incorporation and full activation is where most delays accumulate. Incorporation speed can be swift, but banking and licences sit on the critical path and must be planned early.

Pro Tip: Submit your bank application on the same day you receive your certificate of incorporation. Every day you wait extends the period your entity exists but cannot trade.

Tax obligations in a cross-border business setup are triggered by activity, not just registration. A tax nexus arises when your business has sufficient presence in a country, whether through employees, a fixed place of business, or revenue thresholds. Crossing that threshold creates a local filing obligation even if you have not formally registered there.

VAT registration follows similar logic. The UK VAT threshold, for instance, applies to taxable turnover generated in the UK regardless of where your company is incorporated. The Priceandaccountants VAT guide covers the specific triggers and registration process in detail for UK-facing businesses.

Sound accounting policies are the backbone of multi-jurisdictional compliance. You need consistent policies for revenue recognition, foreign currency translation, and deferred taxation across every entity in your group. Inconsistent policies create audit risk and complicate consolidation at year end.

Ongoing compliance priorities for international founders:

Pro Tip: Appoint a local tax adviser in each jurisdiction from the start. A single adviser trying to cover multiple countries rarely has the depth needed for each one.

Operational scaling requires matching your business model to local realities, not just market size. Roughly 96% of international import and export participants are small businesses. That statistic shows that global reach is achievable at any scale, but it also means the competition for local market share is intense and operationally demanding.

The most common and costly mistake is expanding internationally before the domestic business is stable. Operational weaknesses at home are amplified by international complexity. A cash flow problem that is manageable in one market becomes a crisis when multiplied across three.

“Evaluate market entry through the lens of operational reality rather than chasing headline tax rates or market hype.”

Practical strategies for sustainable international growth:

Overexpansion is a genuine risk. Entering too many markets simultaneously dilutes management focus and stretches capital. Two markets executed well outperform five markets executed poorly.

Successful global business setup depends on matching your entity structure, jurisdiction, and banking arrangements to your operational model before you incorporate.

| Point | Details |

|---|---|

| Jurisdiction choice is operational | Select jurisdictions based on banking access and payment processor support, not tax rate alone. |

| Banking is the critical path | Start your bank application on incorporation day; KYC delays are the most common cause of activation failure. |

| Document preparation takes longer than expected | Apostilles, UBO disclosures, and certified translations must be ready before filing, not after. |

| Tax nexus triggers early obligations | Activity in a country creates filing obligations regardless of where your entity is registered. |

| Domestic stability comes first | Expanding internationally before your home business is stable amplifies existing weaknesses. |

Most founders treat banking as an administrative step they will sort out after incorporation. That is the single most expensive mistake I see in international formation work. The entity exists on paper, the clock is ticking on registered office fees and compliance deadlines, but the business cannot move a penny until a bank account is open.

I have seen UAE Free Zone entities sit dormant for three months because the founder chose a jurisdiction with limited banking options and no appetite for their industry sector. The incorporation took five days. The bank account took fourteen weeks. That gap cost real money and real momentum.

My honest view is that most founders spend too long optimising for tax and not long enough asking whether their chosen jurisdiction is operationally compatible with their business. A UK Ltd with a 25% corporation tax rate and a working bank account on day two beats a zero-tax offshore structure that cannot accept Stripe payments or open a bank account without a six-month wait.

The UK company setup guide from Priceandaccountants lays out the specific steps for UK formation clearly. For most early-stage international founders, the UK remains the most practical starting point precisely because the formation is fast, banking is accessible, and the regulatory environment is well understood.

Get the banking sorted first. Everything else follows from there.

— Rahamut

Setting up across borders creates accounting and tax obligations that compound quickly without the right support in place.

Priceandaccountants works with international founders and growing businesses to manage the full compliance picture, from UK entity formation and VAT registration through to year-end accounts and multi-currency bookkeeping. The team’s accounting and tax services are built specifically for businesses operating across jurisdictions, not adapted from a domestic-only model. Whether you need ongoing bookkeeping, tax advisory for cross-border structures, or support with your first UK entity, Priceandaccountants provides the depth that generalist firms cannot match. Get in touch to discuss your specific situation.

A UK Ltd can be incorporated in 24 hours fully online, making it the fastest option for remote founders. Most other major jurisdictions take between 1 and 7 days.

Many jurisdictions require at least one locally resident director, particularly in Singapore and certain UAE Free Zones. Requirements vary by country and entity type, so confirm this before selecting your jurisdiction.

A tax nexus is triggered by having employees, a fixed place of business, or revenue above a local threshold in a country. It creates a filing obligation regardless of where your company is incorporated.

Bank account opening typically takes weeks and sometimes months, depending on the jurisdiction and the bank’s KYC requirements. Some banks require in-person visits, which extends the timeline further.

Yes. Using an Employer of Record lets you hire and test a market without triggering a tax nexus or VAT obligation. It is the most cost-effective way to validate demand before committing to full entity formation.