TL;DR:

- Many founders mistakenly believe audit readiness is achieved once accounts are prepared, but it requires consistent, process-backed evidence throughout the year.

- Preparation should start from day one, embedding disciplined routines like reconciliations, documentation, and organized evidence to avoid costly last-minute remediation.

Most tech founders assume audit readiness means having finished accounts. It does not. Audit preparation importance goes far deeper: auditors need evidence that your processes are real, consistent, and reliably applied across the year. For UK tech and fintech startups approaching funding rounds or crossing growth thresholds, the gap between “accounts done” and “audit ready” can cost months of remediation, delay investor close, and expose control weaknesses you did not know existed. This guide explains exactly why prepare for audit matters, and what genuine readiness looks like in practice.

| Point | Details |

|---|---|

| Audit readiness is continuous | Start preparing from day one and embed processes monthly rather than scrambling before audits. |

| Evidence quality matters | High-quality, traceable evidence reduces audit questions and speeds up completion. |

| Statutory audits have UK thresholds | Know Companies Act criteria and prepare before crossing triggers or seeking funding. |

| Regulatory audits need control mapping | Fintech firms must map AML/KYC regulations to operational controls and evidence early. |

| Readiness supports fundraising | Well-prepared accounts signal credibility to investors and lenders, facilitating smoother deals. |

The question of why prepare for audit starts with knowing when you are legally required to. Under the Companies Act 2006 thresholds, a UK company triggers a statutory audit requirement when it meets two of three criteria: turnover above £15 million, a balance sheet total exceeding £7.5 million, or more than 50 employees. Many early-stage founders assume these thresholds are distant concerns. They are closer than you think, particularly for fintechs growing at 200 to 300 percent year on year.

But statutory obligation is only part of the picture. Lenders, institutional investors, and even sophisticated angel syndicates routinely demand audit-ready financials well below these thresholds. A Series A lead conducting due diligence does not care whether you are legally obliged to be audited. They care whether your financial controls and documentation can withstand scrutiny. That distinction changes when you should start preparing.

The practical consequence of ignoring this is severe. Companies that cross audit thresholds unprepared typically face three to six months of catch-up work, reconstructing documentation, backfilling reconciliations, and establishing policies that should have existed from day one. Review the year-end accounting tips for tech founders to understand the groundwork required well before your accounts are finalised.

Key items to have in place as early foundations:

Missing any of these when an auditor arrives does not just cause delay. It triggers additional audit procedures, which increases your audit fee and the time your team spends answering queries. The accounting due diligence for UK tech startups guide covers how investor-grade readiness overlaps with audit requirements, which is worth reading alongside this article.

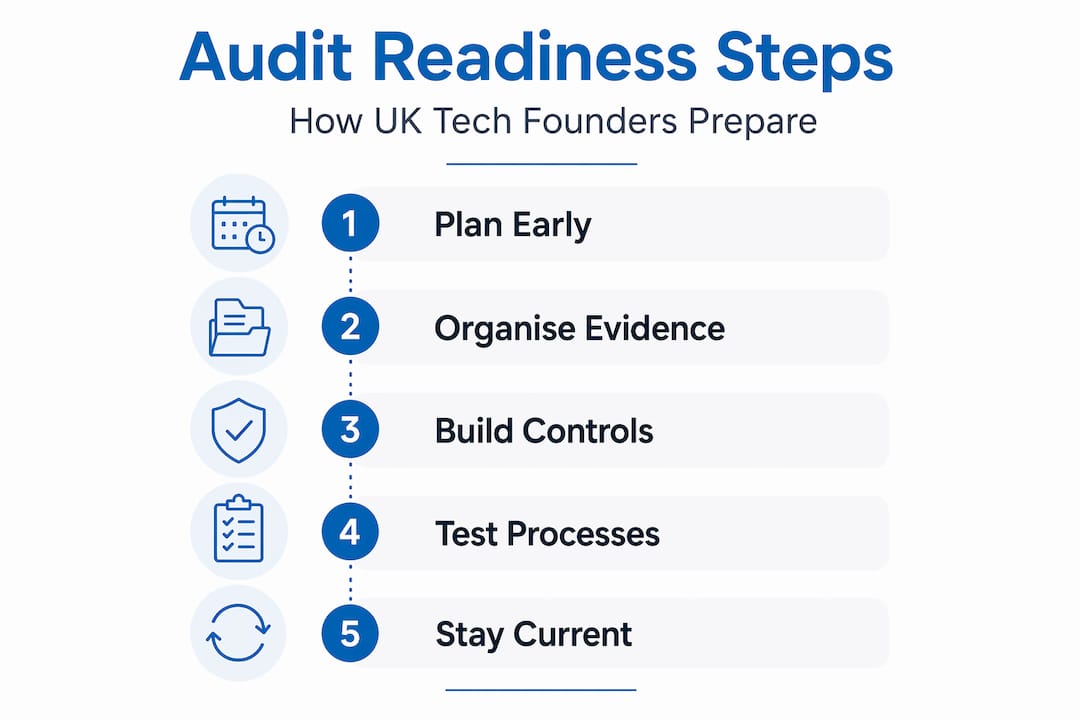

Preparing from day one avoids the three to six months of remediation that companies routinely face when they cross audit thresholds unprepared. That statistic is not alarming for its own sake. It is alarming because those three to six months typically coincide with the period you are trying to close a funding round, onboard a new CFO, or scale the team. The last thing you need is your finance function buried in historical reconstruction.

The shift in mindset required is straightforward: treat audit readiness as an operational discipline, the same way you treat sprint planning or regulatory reporting. Build it into monthly routines so that when an auditor arrives, the evidence is already there.

Here are the key monthly disciplines that separate audit-ready startups from those scrambling at year end:

Pro Tip: Build a rolling Prepared By Client (PBC) file from the start of your financial year. This is a shared folder, usually in Google Drive or SharePoint, organised by audit area, where you deposit evidence continuously as transactions occur. When the auditor sends their request list, most items are already populated. First-time audit engagements take 30 to 50 percent longer when this file does not exist.

For a broader view of how monthly disciplines feed into annual compliance, the guide on corporate accounting for UK tech founders is a practical companion resource.

Gathering evidence is necessary. Gathering good evidence is what actually moves an audit forward. Modern audit quality challenges are frequently tied to insufficient or inappropriate evidence rather than outright errors in the accounts. The distinction matters for founders: your accounts might be technically correct, but if the auditor cannot trace how you arrived at a number through independent, contemporaneous documentation, they are obligated to extend their testing.

“The majority of audit delays stem not from accounting errors but from missing, incomplete, or untraceable evidence that forces auditors to perform additional procedures they had not planned for.” This pattern is consistent across first-time audits at growth-stage companies in every sector.

Evidence quality comes down to four attributes:

Disorganised digital storage is one of the most common practical failures here. A folder named “2025 stuff” containing 400 unsorted PDFs is not audit evidence. Build a folder structure that mirrors your audit areas: revenue, payroll, fixed assets, debtors, creditors, taxation. Every document inside should follow a consistent naming convention. This sounds administrative. In practice, it is one of the most high-impact things a finance team can do to shorten audit duration and reduce stress.

For more context on how evidence quality feeds into tax positions and overall compliance, the small business tax planning guide covers related documentation requirements.

Financial audits test whether your numbers are right. Regulatory audits test whether your controls are right. For fintech founders, this distinction is critical. FCA AML inspections and broader regulatory reviews focus on whether your governance framework is designed correctly and whether it is operating effectively in practice.

Regulatory audit preparation requires mapping your obligations under the Money Laundering Regulations 2017 and FCA SYSC requirements to your internal controls, then producing evidence that those controls actually work. The audit team is not there to understand your product. They are there to verify your control environment.

The key areas a fintech regulatory audit will examine, and the evidence you need for each:

| Regulatory requirement | Internal control | Evidence example |

|---|---|---|

| AML risk assessment | Annual enterprise-wide risk assessment | Signed board-approved risk assessment document |

| CDD/KYC | Onboarding screening procedure | Completed CDD files with risk ratings |

| Transaction monitoring | Automated monitoring with tuned rules | Alert logs and disposition records |

| SAR process | Internal escalation procedure | Internal SAR register with MLRO sign-off |

| Staff training | Annual mandatory AML training | LMS completion records with pass scores |

Pro Tip: Conduct a gap analysis against your regulatory obligations at least 90 days before your expected audit date. Remediation of control gaps, particularly around CDD completeness or monitoring tuning, cannot be done in a fortnight.

For further detail on due diligence obligations specific to your sector, see the accounting due diligence for fintech startups resource, alongside the year-end accounting tips for fintech founders.

The benefits of audit readiness extend well beyond surviving the audit itself. Audit readiness signals governance to investors and lenders during underwriting and onboarding, and prevents the kind of late-stage contradictions that can derail funding rounds at the worst possible moment.

Consider what happens during a Series A diligence process without audit-ready financials. The investor’s accountants request management accounts, reconciliations, and contracts. Your finance team cannot locate three months of bank reconciliations, the revenue recognition policy does not exist in writing, and a significant accrual has no supporting documentation. The investor does not necessarily walk away. But they do adjust their valuation, extend the timeline, or request a full audit at your expense before proceeding. All of that is avoidable.

The practical benefits of genuine audit readiness for fundraising include:

Pro Tip: Align your documentation standards with investor expectations before you start fundraising conversations. Investors increasingly expect management accounts to be produced within ten to fifteen days of month end, with supporting schedules available on request.

For context on what accountants do to support you after investment closes, the article on accountants’ role post investment is directly relevant.

Here is the uncomfortable truth most audit preparation articles skip. The founders who approach audit season with the most stress are rarely those with the most complex businesses. They are the ones who confused activity with readiness. They filed VAT returns on time. They had accounts prepared within nine months. They used Xero. And then an auditor arrived and found that three months of bank reconciliations had never been done, revenue recognition had been applied inconsistently across the year, and the only documentation for a £200,000 accrual was an email chain that nobody could find.

What bookkeeping essentials for tech startups actually produce is the raw material for audit evidence. But raw material is not the same as organised, independent, traceable documentation that an auditor can rely on without follow-up.

The founders who come through audits quickly and calmly share three habits. First, they assign clear ownership: someone specific is responsible for each balance sheet reconciliation, not “finance generally.” Second, they document decisions when they make them. A note in your accounting system explaining why you recognised revenue in a particular way in November is worth infinitely more when written in November than when reconstructed in March. Third, they treat their PBC file as a live document, not a year-end project.

The irony is that embedding these habits takes less time cumulatively than the scramble that happens without them. A monthly reconciliation that takes two hours as you go takes twenty hours to reconstruct after the fact. That is not a rule of thumb. It is a pattern we see consistently across first-time audits at growth-stage companies.

Audit preparation should never fall solely on a founder juggling product, hiring, and fundraising simultaneously. At Price & Accountants, we work with UK tech and fintech startups to embed the financial disciplines that make audits straightforward rather than stressful.

Our expert accounting services cover everything from month-end close routines to year-end accounts, built around the evidence standards auditors actually need. We help you design and document accounting policies that are consistently applied and audit-defensible from day one. Our accurate bookkeeping solutions mean your reconciliations are current, your PBC file grows automatically through the year, and you approach every audit or investor diligence process with confidence. If you are approaching a fundraising round, a statutory audit threshold, or a regulatory inspection, speak to our team before the clock is running against you.

UK companies must have a statutory audit if they meet two of three thresholds under the Companies Act 2006: turnover exceeding £15 million, a balance sheet total above £7.5 million, or more than 50 employees. Investors and lenders may require audit-ready standards below these thresholds.

Preparation should begin from day one of operations, building continuous documentation and control routines throughout the year rather than scrambling at year end, which avoids costly remediation periods of three to six months.

Missing or disorganised evidence is the primary cause of audit delays, not accounting errors. Reconstruction of records after the fact is time-consuming and often raises additional auditor questions about reliability.

Fintechs must map regulations to controls covering governance, customer due diligence, transaction monitoring, suspicious activity reporting, staff training, and record keeping, and should perform a gap analysis at least 90 days before the expected audit date.

Consistent audit readiness signals strong governance and financial reliability to investors and lenders, accelerating due diligence, improving negotiating position, and preventing late-stage funding delays caused by unexpected financial findings.