Many UK tech startups assume R&D tax credits only apply to laboratory research or groundbreaking inventions, missing out on substantial financial support for everyday innovation work. In reality, these government incentives reward a much broader range of projects, from software development to process improvements. If you’re building technology solutions or advancing your field through systematic investigation, you likely qualify for significant tax relief. Understanding what R&D tax credits truly cover and how to claim them effectively can unlock vital funding to accelerate your growth in 2026.

| Point | Details |

|---|---|

| Government innovation support | R&D tax credits reduce corporation tax bills or provide cash refunds for qualifying science and technology projects |

| Scheme transition matters | The merged R&D scheme applies to accounting periods from 1 April 2024, replacing previous SME and RDEC schemes |

| Eligibility is specific | Many business types including hospitality, retail, and personal services rarely qualify for R&D tax relief |

| Advance assurance available | First-time claimants can confirm project eligibility before filing through HMRC’s advance assurance programme |

| Specialist support recommended | Working with experienced tax advisers significantly improves claim success rates and maximises relief amounts |

R&D tax credits represent government incentives for innovation that reward UK companies investing in scientific and technological advancement. These credits directly reduce your corporation tax liability or provide cash payments when your company has no tax to pay. For tech startups burning through capital whilst developing products, this financial support can mean the difference between runway extension and premature closure.

The scheme specifically targets companies working to resolve scientific or technological uncertainties through systematic investigation. You’re not required to succeed in your innovation attempts. The government recognises that genuine R&D involves risk and potential failure. What matters is demonstrating that your project sought to advance knowledge or capability in your field beyond what competent professionals could readily deduce.

Qualifying activities span a remarkably wide range within technology sectors:

The relief operates through two mechanisms depending on your tax position. Profitable companies receive enhanced deductions against corporation tax, reducing their tax bills substantially. Loss-making companies, common among early-stage startups, can claim cash credits paid directly by HMRC. This cash option proves particularly valuable when you need immediate funding rather than future tax savings.

“R&D tax relief helps companies that work on innovative projects in science and technology by allowing them to deduct more than 100% of their qualifying costs from their yearly profit, as well as a cash alternative.”

Understanding these fundamentals helps you recognise opportunities within your own operations. Many founders overlook maximising R&D tax credits because they underestimate how broadly the scheme applies to technology development work.

Eligibility hinges on three critical factors: your project’s innovative nature, your business structure, and your accounting period dates. The government maintains strict criteria to ensure relief targets genuine innovation rather than routine development. Your project must seek to achieve an advance in science or technology by overcoming uncertainties that competent professionals in your field cannot readily resolve.

Certain business sectors rarely qualify for claims regardless of their activities. Restaurants, pubs, wholesalers, retailers, personal trainers, childcare providers, and care homes typically fall outside the scheme’s scope. These exclusions reflect the scheme’s focus on science and technology advancement rather than service delivery improvements or operational efficiencies.

Your accounting period determines which relief scheme applies to your claim. This distinction carries significant financial implications:

| Scheme aspect | SME scheme (pre-April 2024) | Merged scheme (post-April 2024) |

|---|---|---|

| Applicable periods | Accounting periods beginning before 1 April 2024 | Accounting periods beginning on or after 1 April 2024 |

| Company size focus | Small and medium enterprises | All company sizes |

| Relief rates | Higher enhancement rates for SMEs | Standardised rates across company sizes |

| Claim complexity | Separate SME and RDEC schemes | Single unified framework |

The accounting period governs scheme selection, not the calendar year or when you file your claim. A company with an accounting period starting 1 March 2024 uses the SME scheme, whilst one starting 1 May 2024 uses the merged scheme. Straddling periods require apportionment between schemes, adding complexity to calculations.

Company size classification depends on staff headcount, turnover, and balance sheet totals. You qualify as an SME if you have fewer than 500 employees and either annual turnover below €100 million or a balance sheet below €86 million. These thresholds apply at group level, so parent company structures affect your classification.

Pro Tip: Verify your accounting period start date before beginning any R&D claim preparation. Using the wrong scheme framework invalidates your entire claim and triggers HMRC queries that delay payment for months.

Subsidised expenditure rules add another layer. Costs funded by grants, subsidies, or notified state aid may face restricted relief rates. The merged scheme introduced an intensive support category for heavily subsidised R&D, offering lower but still valuable relief rates. Understanding these nuances prevents nasty surprises when calculating expected benefits.

The 2026 R&D credit landscape continues evolving as HMRC refines compliance requirements and fraud prevention measures. Staying current with rule changes protects your claims from rejection whilst maximising legitimate relief.

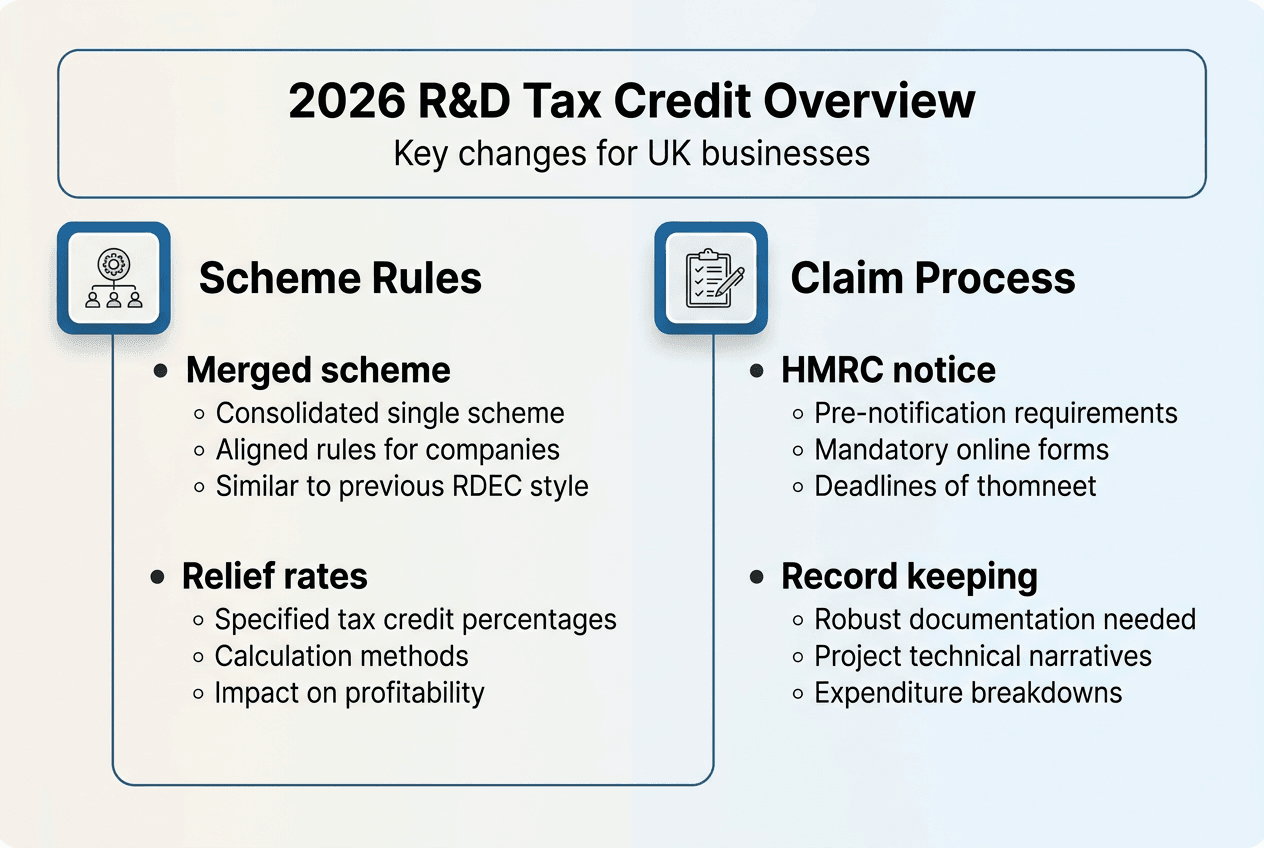

The merged scheme fundamentally changed how UK companies claim R&D tax relief for accounting periods beginning on or after 1 April 2024. This consolidation combined the previous SME scheme and Research and Development Expenditure Credit into a single framework, simplifying administration whilst adjusting relief rates. For tech startups, understanding these changes proves essential to accurate claim preparation.

The transition created a clear dividing line. Companies with accounting periods starting before 1 April 2024 continue using the SME scheme rules for those periods. Those starting on or after that date must apply the merged scheme framework. This date-driven approach means two similar companies might use different schemes based purely on their accounting period start dates.

Key merged scheme features include:

Determining your applicable scheme requires checking your accounting period carefully. Companies with year-end dates in early 2024 likely fall under SME rules, whilst those with later year-ends use the merged scheme. Straddling periods demand apportionment, calculating relief separately for pre and post-transition portions.

| Consideration | SME scheme approach | Merged scheme approach |

|---|---|---|

| Relief calculation | Enhanced deduction against profits | Tax credit based on qualifying expenditure |

| Loss-making companies | Payable credit at higher rate | Payable credit at standard rate |

| Overseas costs | More flexibility | Stricter UK focus requirements |

| Subcontractor rules | Connected party restrictions | Broader restrictions on all subcontractors |

| Notification | Not required | Mandatory for new claimants |

The merged scheme’s notification requirement catches many first-time claimants off guard. You must inform HMRC of your intention to claim within six months of your accounting period end, before submitting your actual claim. Missing this deadline can invalidate your entire claim regardless of project merit.

Pro Tip: Mark your calendar six months before your accounting period end to submit the mandatory R&D notification to HMRC. This simple administrative step protects potentially six-figure claims from automatic rejection.

Relief rate changes under the merged scheme affect cash flow projections significantly. Loss-making SMEs previously enjoyed higher payable credit rates, providing substantial cash injections. The merged scheme’s standardised rates reduce this benefit, though relief remains valuable. Adjusting your financial forecasts to reflect actual merged scheme rates prevents budget shortfalls.

The scheme also tightened rules around deferred taxation implications and how relief interacts with other tax positions. Companies carrying forward losses or utilising group relief must consider how R&D claims affect their broader tax strategy. These interactions grow complex quickly, particularly for companies with multiple entities or international structures.

HMRC increased compliance scrutiny alongside the merged scheme introduction. Enhanced information requirements mean you’ll provide more detailed technical and financial evidence supporting your claims. This shift towards transparency aims to reduce fraudulent claims whilst ensuring legitimate innovators receive their entitled relief.

Successful R&D claims begin long before you file paperwork with HMRC. The advance assurance scheme offers first-time claimants invaluable certainty by allowing you to confirm project eligibility before investing significant time in claim preparation. This programme particularly benefits startups unsure whether their activities meet R&D criteria.

Advance assurance provides written confirmation that HMRC accepts your projects as qualifying R&D for up to three accounting periods. You submit a detailed project description explaining the scientific or technological uncertainties you’re addressing and how you’re attempting to resolve them. HMRC reviews your submission and issues a decision, giving you confidence to proceed with full claims or adjust your approach if projects don’t qualify.

Documentation forms the foundation of every successful claim. Start capturing evidence contemporaneously as your R&D work progresses:

The claiming process follows a structured sequence:

Working with specialists who understand both technology and tax legislation significantly improves outcomes. R&D tax advisers help identify qualifying activities you might overlook, maximise eligible expenditure calculations, and present claims in ways that satisfy HMRC requirements. Their expertise proves particularly valuable for avoiding common rejection triggers.

Pro Tip: Treat your R&D claim as a storytelling exercise. HMRC inspectors aren’t technology experts, so clearly explain what uncertainty you faced, why it wasn’t readily solvable, what you tried, and how you systematically worked towards resolution.

Common pitfalls that derail claims include:

The financial impact of successful claims justifies careful preparation. Tech startups commonly receive five to six-figure payments that fund additional development sprints, extend runway, or support hiring. These cash injections arrive when you need them most, during intensive growth phases when capital efficiency determines survival.

Maintaining ongoing R&D records throughout the year, rather than reconstructing activities retrospectively, dramatically improves claim quality. Implement simple systems where developers log technical challenges and solutions as they work. These contemporaneous notes provide compelling evidence that satisfies even the strictest HMRC reviews.

Your R&D tax credit strategy should integrate with broader financial planning. Consider how relief timing affects cash flow, how claims interact with investor funding rounds, and how to communicate R&D capabilities to stakeholders. This holistic approach ensures you extract maximum value from the scheme whilst maintaining compliance and credibility.

Navigating R&D tax credits whilst building your startup demands expertise you likely don’t have in-house. Price & Accountants specialises in helping UK tech startups maximise innovation funding through expert R&D tax credit services tailored to your growth stage. We’ve supported over 20 startups through their R&D claiming journey, many now valued above £50 million.

Our team handles the entire claim process, from identifying qualifying activities to preparing technical reports that satisfy HMRC requirements. We integrate R&D claims with your broader accounting services, ensuring accurate cost tracking and optimal relief calculations. Understanding how accounting periods affect scheme selection, we guide you through merged scheme complexities whilst maintaining compliance. Connect with our specialists to transform your innovation work into substantial cash benefits that fuel your next growth phase.

An R&D tax credit is a government incentive providing tax relief or cash payments to companies engaging in qualifying research and development activities. The scheme rewards businesses that work to resolve scientific or technological uncertainties through systematic investigation. It’s designed to encourage innovation and technological advancement within UK businesses by reducing the financial burden of R&D investment.

Projects that aim to resolve scientific or technological uncertainties through systematic investigation qualify for R&D tax credits. Your work must seek to advance overall knowledge or capability in your field beyond what competent professionals could readily deduce using existing techniques. Routine development, customisation work, or applying known methods to new situations typically don’t qualify unless they involve overcoming genuine technical challenges.

Most UK companies involved in innovative science or technology projects may qualify, but certain sectors rarely meet eligibility criteria. Businesses in hospitality, retail, personal services, childcare, and care homes typically don’t qualify regardless of their activities. Eligibility depends on meeting specific government criteria related to the innovative nature of your work and whether it genuinely advances scientific or technological knowledge in your field.

Identify qualifying projects and costs early in your accounting period, maintaining detailed contemporaneous records of technical challenges and solutions. Consider using the advance assurance scheme if you’re a first-time claimant to confirm project eligibility before investing significant resources. Submit the mandatory notification to HMRC within six months of your period end, prepare comprehensive technical and financial documentation, and file your claim accurately with your Corporation Tax return. Consulting specialist tax advisers significantly improves claim success rates and ensures you maximise legitimate relief whilst maintaining compliance.