TL;DR:

- UK small businesses must register with HMRC at least four weeks before their first payroll run.

- Using payroll software or outsourcing reduces errors, penalties, and compliance risks.

- Tech startups should consider IR35 exemptions and sector-specific contractor regulations.

84% of UK SMEs make payroll errors and 40% have faced fines as a direct result. For founders running lean tech or fintech teams, payroll mistakes are not just an administrative headache — they are a genuine financial risk. HMRC penalties, unhappy staff, and compliance failures can derail growth at the worst possible moment. This guide walks you through every stage of running payroll correctly in the UK, from registering with HMRC to handling IR35 for contractors. Whether you have two employees or fifty, the steps here will help you build a process that is accurate, timely, and built to scale.

| Point | Details |

|---|---|

| Register early with HMRC | Apply as an employer at least four weeks before payday to avoid setup delays. |

| Use payroll software for accuracy | Automated software cuts errors and fines by reducing manual input mistakes. |

| Meet all HMRC deadlines | Submit all payroll reports and payments on time to keep compliant and avoid penalties. |

| Know your allowances | Employers can claim up to £5,000 Employment Allowance and should check eligibility each year. |

| Stay prepared for sector rules | Tech and fintech teams must watch for IR35 and contractor-specific challenges in payroll. |

Before you pay a single employee, you need the right foundations in place. Skipping this stage is where most small teams come unstuck.

The first step is to register as an employer with HMRC. You must do this before your first payday, ideally four weeks in advance, to allow time for HMRC to issue your PAYE reference number. Without it, you cannot submit payroll data or pay over tax and National Insurance. Processing typically takes five to ten working days, so do not leave it until the week before salaries are due.

Beyond registration, you have several legal obligations to meet from day one:

Here is a quick overview of the core tools you will need:

| Requirement | What you need | Where to get it |

|---|---|---|

| PAYE reference | Employer registration | HMRC via gov.uk |

| Tax codes | P45 or starter checklist | Employee or HMRC |

| Payroll software | RTI-compliant program | HMRC-approved list |

| Pension provider | Workplace pension scheme | Authorised provider |

| Employee records | Contracts, NI numbers | HR onboarding process |

Good bookkeeping for UK startups supports your payroll process too, since accurate financial records make reconciliation far simpler at year-end.

Pro Tip: Set a calendar reminder four to six weeks before your first hire’s start date to begin the HMRC registration process. Late registration is one of the most common and entirely avoidable causes of payroll delays.

With your registration and tools in place, here is how a typical payroll run works for a small UK business.

Missing the FPS deadline triggers penalties. Check the PAYE for employers guidance for the current penalty schedule.

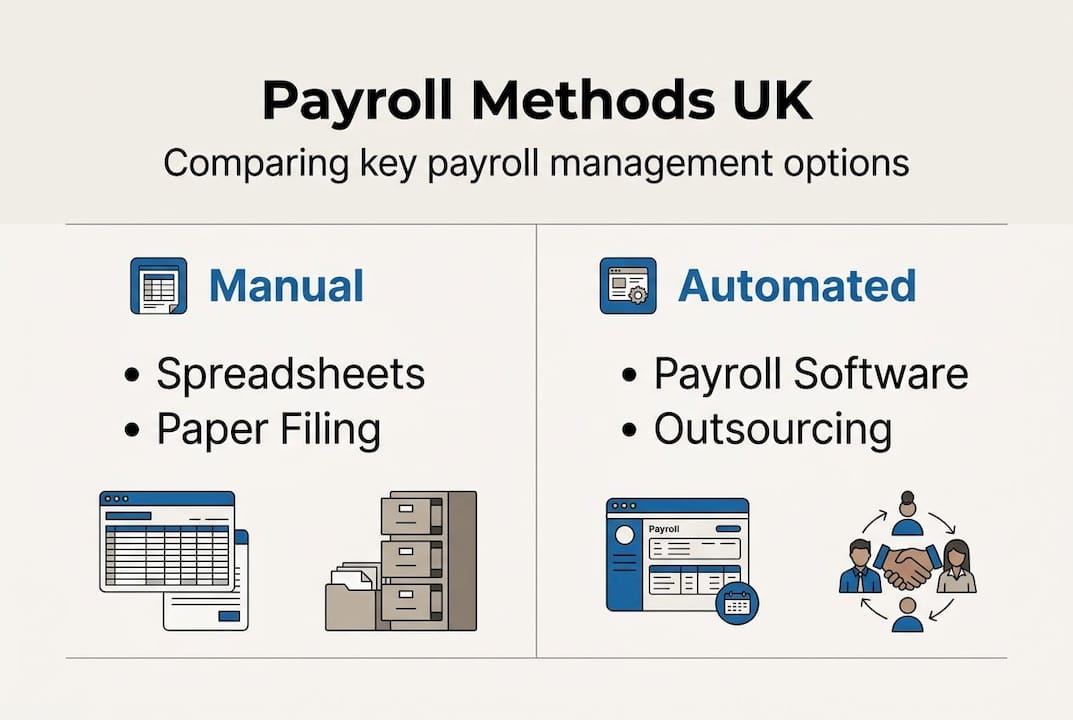

| Method | Accuracy | Time cost | HMRC compliance | Best for |

|---|---|---|---|---|

| Manual spreadsheets | Low | High | Risk of errors | Pre-registration only |

| Payroll software | High | Low | Automated RTI | Teams of 2 to 50 |

| Outsourcing | Very high | Minimal | Fully managed | Complex or growing teams |

Many founders find that outsourcing payroll for UK tech startups removes the compliance burden entirely, freeing up time for product and growth.

Pro Tip: Integrate your payroll software with your cloud accounting platform. When payroll journals post automatically to your accounts, you eliminate a manual step and reduce the risk of reconciliation errors at month-end.

Processing payroll is only part of compliance. Getting the deductions right every single pay period is where many small businesses quietly accumulate problems.

Income tax is calculated using each employee’s tax code. The most common code in 2026 is 1257L, which reflects the £12,570 personal allowance. Employee NIC applies above the primary threshold, while employer NIC is charged at 13.8% on earnings above the secondary threshold. These rates are set by HMRC and updated annually, so always verify them at the start of each tax year.

If your employer NIC bill is below £100,000 per year, you may be eligible to claim Employment Allowance, which reduces your employer NIC liability by up to £5,000. It is a genuine saving and worth claiming from the outset.

“Issue P60s to all employees by 31 May each year. Submit P11D forms for benefits in kind by 6 July. Keep all payroll records for at least three years.” — Payroll compliance checklist

Your annual payroll compliance checklist should include:

For a deeper look at the numbers behind these obligations, the official guide to PAYE and NIC is the definitive reference. Pairing this with strong bookkeeping essentials for tech startups keeps your financial picture clean year-round.

Even with a solid process, preventable errors creep in. The data is stark: 84% of UK SMEs make payroll errors, with 48% getting wage calculations wrong and 40% receiving fines. Manual methods are a significant contributor, with between 31% and 44% of small businesses still relying on spreadsheets.

The most common triggers for errors include:

Switching to HMRC-approved payroll software removes most of these risks automatically. You can compare UK payroll software to find the right fit for your team size and budget. The time saving alone is significant: software typically cuts payroll processing time by more than half compared to manual methods.

When deciding between software and outsourcing, consider this: software works well when someone in your team has the time and confidence to manage it. Outsourcing makes more sense when compliance complexity is high or your team is scaling quickly. Reviewing bookkeeping best practices alongside your payroll setup will also help you spot inconsistencies early.

Pro Tip: Set up calendar alerts for the 15th of each month as a prompt to finalise payroll before the 22nd HMRC payment deadline. A two-step reminder system, one to prepare and one to pay, virtually eliminates late payment penalties.

Unique sector rules and contractor situations add another layer of complexity. Tech and fintech firms should review these special considerations carefully.

IR35 is the tax legislation designed to prevent disguised employment, where contractors work like employees but pay less tax by operating through a personal service company. The good news for most small tech businesses is that small companies are exempt from the off-payroll working rules that require clients to determine a contractor’s IR35 status. You qualify as a small company if you meet at least two of the following: annual turnover below £10.2m, balance sheet below £5.1m, or fewer than 50 employees.

However, being exempt does not mean IR35 is irrelevant. If a contractor is found to be inside IR35, the deemed payment rules apply: the contractor’s company must deduct a 5% expenses allowance, calculate a deemed employment payment, and account for PAYE and employer NIC on that amount.

Common payroll complexity triggers in tech and fintech include:

For broader tax compliance tips for UK tech businesses, including R&D reliefs and share schemes, a sector-specialist adviser makes a real difference. The employer payroll guide from ByteStart also covers the basics well for those new to running a team.

After years of helping UK tech and fintech startups get payroll right, one pattern stands out clearly: the founders who struggle most are not the ones who know the least. They are the ones who think payroll is simpler than it is and build a process that works fine until it suddenly does not.

Old spreadsheet templates, copied from a previous job or downloaded from the internet, are a particular trap. They do not update for rate changes, they do not flag missing data, and they give a false sense of control. When HMRC issues a penalty, the spreadsheet offers no protection.

Cloud payroll tools genuinely change this. The time saving is real, but the bigger win is confidence. When your FPS submits automatically and your accounts reconcile without manual journals, you spend less mental energy on compliance and more on building your product.

For founders watching every pound, the instinct to do payroll yourself is understandable. But the cost of a single HMRC penalty or a disgruntled employee who was underpaid often exceeds a year’s worth of software or adviser fees. Good bookkeeping tips for tech and fintech businesses will reinforce this point: automation is not a luxury for small teams. It is the foundation of a scalable business.

If payroll still feels daunting or you want expert eyes on your numbers, know that help is at hand.

At Price & Accountants, we work with UK tech and fintech businesses every day, handling payroll, compliance, and everything in between. Our bookkeeping services keep your records clean and audit-ready, while our accounting services give you a full picture of your financial position at all times. If your business is also spending on innovation, our R&D tax credits guide shows how you could reclaim significant capital. We do not just file returns — we act as your financial growth partner, so you can focus on scaling your team with confidence.

Register as an employer with HMRC at least four weeks before your first payday, as HMRC processing typically takes five to ten working days and you need your PAYE reference before you can run payroll.

Missing the FPS deadline can result in a penalty of £100 to £400 per month, so always submit on or before payday and pay PAYE and NIC by the 22nd of the following month.

Payroll software is typically the most efficient choice for teams of 2 to 50, automating RTI submissions and auto-enrolment, but outsourcing adds real value when compliance complexity grows or internal capacity is limited.

Most small UK tech and fintech companies are exempt from IR35 client determination obligations, but you should still assess each contractor’s working arrangements carefully to avoid unexpected liability.