TL;DR:

- Specialist accountants are crucial for maximizing UK R&D, SEIS, and EIS claims and compliance.

- Proper structuring and early planning significantly improve funding prospects and reduce costly errors.

- Outsourced financial management provides vital KPI and forecasting support as startups scale.

Thousands of pounds in tax relief slip through the fingers of UK tech and fintech founders every single year. The R&D claims dropped 26% year-on-year in 2023-24, with the tech sector alone falling nearly 14%, pointing to a systemic problem: brilliant founders building genuinely innovative companies are leaving serious money on the table. SEIS and EIS schemes offer life-changing investor incentives, and R&D tax credits can recycle real capital back into your runway. But the rules are intricate, HMRC scrutiny is intensifying, and the gap between a successful claim and a costly mistake often comes down to one thing: the right accountant by your side.

| Point | Details |

|---|---|

| Specialist advice is critical | Tech founders unlock more relief and avoid costly mistakes using specialist accountant help. |

| SEIS/EIS maximise investment | Advance assurance and expert structuring make SEIS/EIS work for ambitious, high-growth startups. |

| R&D claims need evidence | Mandatory tech narratives, evidence and accountant oversight boost your chances under HMRC scrutiny. |

| Outsourced finance drives scale | Financial experts provide the data, discipline and investor readiness that fuel sustainable growth. |

| Proactivity beats correction | Early, professional help avoids delays and painful, expensive fixes demanded later by HMRC or investors. |

Regular bookkeeping is fine for a café. It is not fine for a Series A fintech navigating R&D claims, investor compliance, and a dual SEIS/EIS round simultaneously. The regulatory terrain for high-growth startups is genuinely complex, and that complexity compounds fast.

HMRC’s requirements for R&D and SEIS/EIS are not static. They change annually, and the definitions of qualifying activities, eligible costs, and investor conditions shift with each Finance Act. Generalist accountants who service a broad client base rarely invest the time to track these changes in forensic detail. That creates real exposure for founders.

Common mistakes we see include:

Each of these errors can cost your startup thousands, trigger a formal enquiry, or put off an incoming VC who spots a compliance red flag during due diligence. The stakes are not abstract.

“Specialist firms provide scalable teams and KPI dashboards preferred over generalists, precisely because HMRC scrutiny demands a higher level of sector-specific expertise.”

Specialist teams act as both compliance guardians and opportunity finders. They know which costs qualify, which activities meet the ‘technological uncertainty’ test, and which share structures preserve SEIS eligibility. Solid startup tax planning from the outset is far cheaper than correcting errors later, and optimising your tax workflow early in your growth journey compounds the benefit year after year.

Pro Tip: Appoint a specialist accountant before you issue your first investor share, not after. Retroactive restructuring is possible but expensive and sometimes impossible.

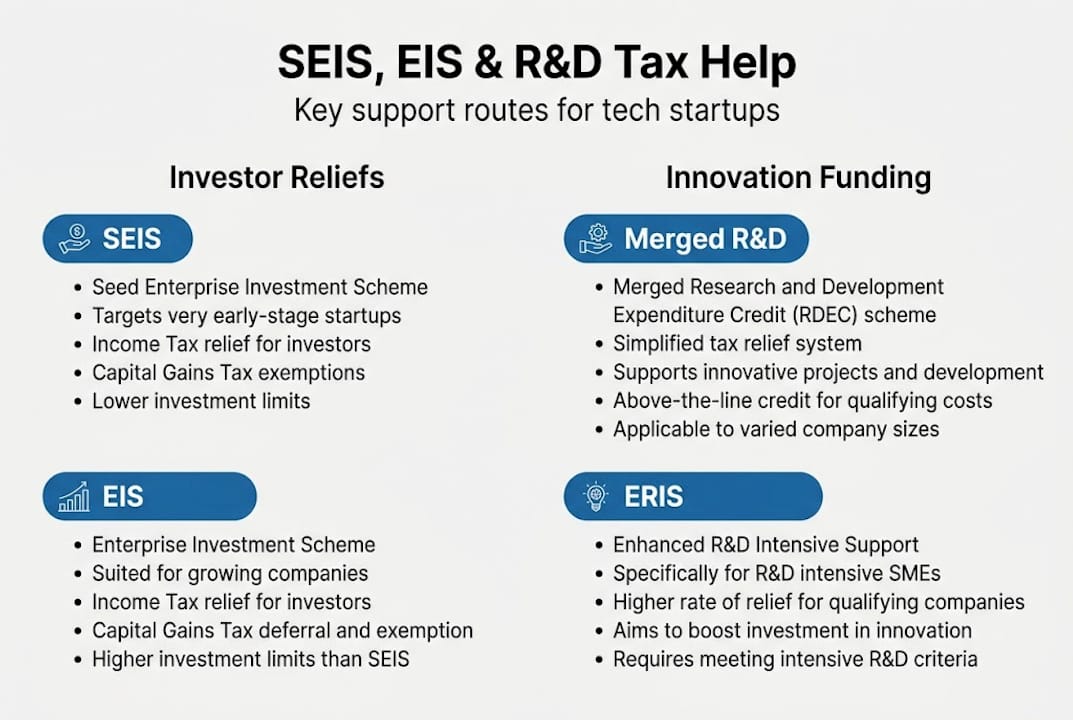

SEIS and EIS are two of the most powerful investor incentives in Europe. Understanding their differences is critical before you approach a single angel or syndicate.

| Feature | SEIS | EIS |

|---|---|---|

| Income Tax relief | 50% | 30% |

| Maximum investment per year | £200,000 | £1m (£2m for knowledge-intensive) |

| Company age limit | Under 3 years | Within 7 years of first commercial sale |

| Gross assets limit | Under £350,000 | Under £15m |

| Number of employees | Fewer than 25 | Fewer than 250 |

| CGT exemption on exit | Yes (after 3 years) | Yes (after 3 years) |

SEIS provides 50% income tax relief on investments up to £200,000, targeting very early-stage companies. EIS offers 30% relief up to £1m, or £2m for knowledge-intensive companies, covering businesses within seven years of their first commercial sale. Both schemes carry strict qualifying conditions that catch out founders who try to navigate them alone.

The typical compliance workflow runs like this:

Following the advance assurance steps correctly is non-negotiable. Many investors will not commit capital without it, and submitting inaccurate information at this stage can invalidate the entire round later.

The silent disqualification risk is particularly serious. A founder who draws a salary as an employee (rather than as a non-executive director) before shares are issued can disqualify the company from SEIS without realising it. Joint ownership of intellectual property or subsidiaries can also break eligibility. Understanding SEIS/EIS tax consultancy options early, and reviewing SEIS/EIS success strategies from experienced practitioners, gives you a material advantage before you ever talk to investors.

The R&D landscape changed substantially in April 2024. From that date, a merged R&D scheme replaced the previous SME and RDEC tracks for most companies.

| Feature | Merged scheme (from Apr 2024) | Enhanced R&D Intensive Support (ERIS) |

|---|---|---|

| Who qualifies | Most UK companies | R&D-intensive SMEs (40%+ qualifying spend) |

| Payable credit rate | 20% | 27% |

| Mandatory pre-notification | Yes (CNF) | Yes (CNF) |

| Subcontractor rules | Stricter | Stricter |

| Overseas costs | Limited | Limited |

From April 2024, the merged R&D scheme introduced a standard 20% credit rate and a 27% ERIS rate for R&D-intensive SMEs, alongside mandatory pre-notification requirements. That pre-notification, known as the Claim Notification Form (CNF), must be submitted to HMRC within six months of the end of the accounting period in question. Miss it, and your claim is void.

For fintech and AI businesses, qualifying activities are broader than many founders expect. Building a novel fraud detection model that resolves genuine technical uncertainty qualifies. Developing proprietary API infrastructure that addresses a specific engineering problem qualifies. Simply integrating existing APIs or adapting standard software frameworks generally does not. The distinction is subtle but critical.

What actually strengthens a claim:

Despite £7.6bn in total R&D relief claimed in 2023-24, SME claims and tech sector outcomes fell sharply, reflecting both tighter HMRC scrutiny and weaker claims preparation. A specialist accountant understands R&D tax relief inside out, and knows how to position your activities for maximum credit while withstanding enquiry. If you are ready to file, a detailed guide on claiming R&D credits as a UK tech startup is a practical starting point.

Pro Tip: Start gathering R&D evidence on the first day of your accounting year, not three weeks before you file. Retrospective reconstruction raises HMRC red flags and weakens your claim.

Once you have secured seed funding and your team grows beyond ten people, the financial complexity of your business changes shape entirely. You now have payroll, multi-currency transactions, investor reporting obligations, board-level KPIs, and a burn rate that needs active management. Hiring a full-time Finance Director at this stage is expensive, often premature, and rarely necessary.

Outsourced financial management solves this elegantly. A specialist outsourced finance team brings:

Specialist outsourced teams provide KPI dashboards, investor-ready forecasts, and scaleup-appropriate support that generalist firms simply cannot match. The difference shows up most sharply when a VC requests three years of clean management accounts during a Series A process and you can produce them in 24 hours rather than three weeks.

The most common pitfalls we see in scaleups that have outgrown their bookkeeper but not yet hired a proper finance function include cash flow blind spots (not knowing your true runway at any given moment), no investor-grade reporting, and a complete absence of scenario modelling for fundraising. These are not minor gaps. They can delay a round by months.

The guide to SEIS/EIS accountants for tech founders goes deeper on how to vet and select a specialist firm that can grow with you from pre-seed through to Series A and beyond.

Pro Tip: Ask any prospective outsourced finance partner to show you a sample investor dashboard before you sign. If it looks like a standard Excel spreadsheet, keep looking.

Here is the uncomfortable truth we see repeatedly: founders who build genuinely world-class products often apply the same frugal mindset to financial advice that they use for office furniture. That instinct makes sense in the early days. It becomes costly from the moment you take your first investor pound.

The myth that specialist accountant help is expensive overhead collapses the moment you see the numbers. A well-executed R&D claim on £500,000 of qualifying spend can return £100,000 or more. A clean SEIS structure protects your investors’ capital and your fundraising credibility. These are not marginal returns. The ROI on good advice is measurable and often immediate.

Speed matters enormously too. Advance Assurance takes time, HMRC processes claims at its own pace, and a delayed or rejected submission can push your funding round back by a quarter. The founders who treat financial compliance as a strategic asset, not an administrative burden, raise faster and retain more equity. Reviewing your approach to maximising R&D credits is often the single highest-return hour a founder can spend.

If any of the above has resonated, the next step is straightforward. At Price & Accountants, we work exclusively with tech and fintech founders who need more than a generalist firm can offer.

We manage R&D tax credits end to end, from CNF submission through to defending claims under HMRC enquiry. We handle SEIS and EIS advance assurance, share structuring, and compliance filings so your investors receive their certificates without delay. Our outsourced finance service delivers the KPI dashboards, forecasting, and strategic input your board expects, without the cost of a full-time FD. Explore our full range of accounting services or speak to a specialist today to see exactly how we can support your next stage of growth.

Founders are eligible for SEIS if the company is under three years old, has gross assets below £350,000, and founder-directors are not paid employees. EIS applies to companies within seven years of their first commercial sale with assets below £15m.

You need a technical narrative, a detailed cost breakdown, contemporaneous evidence such as experiment logs or version control records, and a mandatory pre-notification submitted to HMRC before the claim is filed.

Specialist teams provide forecasting and KPI reporting that make investor conversations far smoother, giving VCs and angels the clean, auditable data they need to commit capital quickly.

Yes, but share issue timing and grant stacking rules require careful planning. Advance assurance and structuring must account for HMRC rules on combining the two schemes to avoid double-counting or silent disqualification.